Corporate bonds aren’t just about yield—they’re influenced by the same types of systematic factors we associate with stocks. This paper explores how value, momentum, low-risk, and size factors explain differences in corporate bond returns across firms and over time. Using a massive dataset of global investment-grade and high-yield bonds, the authors show that bonds with higher value and momentum scores outperform, while low-risk bonds offer better risk-adjusted returns. Interestingly, these effects persist even after adjusting for traditional bond risk factors like interest rates and default risk. For advisors, this opens new paths to improve fixed income portfolios using smart beta principles.

The Cross-Section of Corporate Bond Returns

- GUIDO BALTUSSEN, FREDERIK MUSKENS, and PATRICK VERWIJMEREN

- Working paper, June 2025

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

Factor Investing Applies to Bonds too,

Much like equities, corporate bonds exhibit return patterns based on value (cheap vs. expensive), momentum (past winners), low-risk (lower volatility), and size (issuer scale). These factors have persistent and statistically significant effects on bond performance globally.

Value and Momentum are especially strong

Bonds issued at cheaper prices relative to fundamentals (e.g., OAS vs. duration or credit quality) tend to outperform more expensive bonds. Similarly, bonds with strong recent price momentum tend to keep performing well in the near term.

Low-Risk Outperforms on a Risk-Adjusted Basis

Low-volatility bonds, while less exciting, tend to deliver superior Sharpe ratios. This challenges the idea that higher yield (i.e., risk) always translates into better long-term results.

These results are Robust

The findings hold across different markets (U.S., Europe, and global), bond types (investment grade and high yield), and remain valid after controlling for liquidity, credit ratings, and macroeconomic factors.

Practical Applications for Investment Advisors

Use Factors to Build Smarter Bond Portfolios

Move beyond traditional duration and credit risk. Consider tilting fixed income portfolios toward bonds with favorable value and momentum characteristics, or incorporating low-risk bond strategies to improve Sharpe ratios. See also Factor Investing in Sovereign Bond Markets for a broader look at applying smart beta across asset types.

Rethink “High Yield” as a Risk Premia Strategy

Not all high-yield bonds compensate for their risk appropriately. Advisors should be selective—especially since low-risk bonds can sometimes outperform high-yield peers on a risk-adjusted basis.

Apply Equity Thinking to Fixed Income

If you’re already using factor-based ETFs for equities, consider similar approaches in the bond sleeve of client portfolios. Many smart beta ETFs now target these exact bond anomalies.

How to Explain This to Clients

“When you invest in bonds, it’s easy to think your only choices are between safe government bonds and risky high-yield ones. But new research shows that, just like with stocks, some bonds offer better value than others—especially those with good track records (momentum) or that are temporarily underpriced (value). By carefully choosing these types of bonds, we aim to improve your portfolio’s returns without taking on unnecessary risk.”

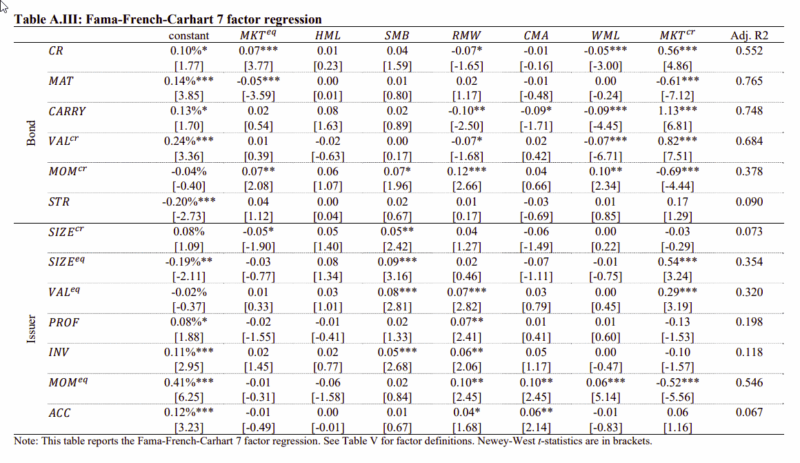

The Most Important Chart from the Paper

The table below, Table A.III, reports factor alphas relative to equity factors. More specifically, the authors regress each corporate bond factor mimicking portfolio on Fama and French (2015) five-factor model that includes the return of the equity market minus the risk-free rate (𝑀𝐾𝑇), small minus big (𝑆𝑀𝐵), high minus low (𝐻𝑀𝐿), robust minus weak (𝑅𝑀𝑊), conservative minus aggressive (𝐶𝑀𝐴), and expand it with

winners minus losers (𝑊𝑀𝐿), and the credit return of the corporate bond market (𝑀𝐾𝑇).

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

We examine the cross-section of U.S. corporate bonds and account for the infrequent trading of corporate bonds, sample selection bias, duration-matching, and high transaction costs. In a net-of-costs setting, four factors turn out to offer unique, robust, and sizable return premia. These factors are a short maturity factor, a bond value factor, an equity momentum factor, and an accruals factor. A five-factor model that combines the market factor with these four factors most robustly prices the cross-section of corporate bonds after accounting for transaction costs.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.