Asset pricing research often focuses on risk, valuation, and macroeconomic forces. But this paper highlights another surprisingly powerful driver of returns: the timing of dividend payments. Across 44 international equity markets, the authors uncover a large and persistent “dividend premium.” Dividend-paying stocks outperform non-payers by a meaningful margin, even after controlling for traditional global and regional risk factors.

Dividend Timing and Global Dividend Premium

- Allaudeen Hameed, Jing Xie and Yuxiang Zhong

- working paper, 2026

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

Dividend-paying stocks outperform globally

Using data from 44 international equity markets between 1993 and 2018, the paper documents a robust dividend premium. Dividend-paying stocks outperform non-payers by approximately 0.58% per month after adjusting for global and regional risk factors. The effect is remarkably widespread. The premium is positive in 95% of markets after factor adjustments, suggesting that dividend-paying status represents a globally priced characteristic rather than a local anomaly.

The dividend premium has two distinct components

The authors show that the dividend premium is not a single phenomenon. It consists of a timing-related component and a persistent component. The timing-related component comes from predictable investor demand around dividend events. Stocks earn unusually strong returns before ex-dividend dates, followed by only partial reversals afterward. The persistent component survives even outside dividend-event windows and appears linked to governance and institutional quality.

Dividend timing creates predictable price pressure

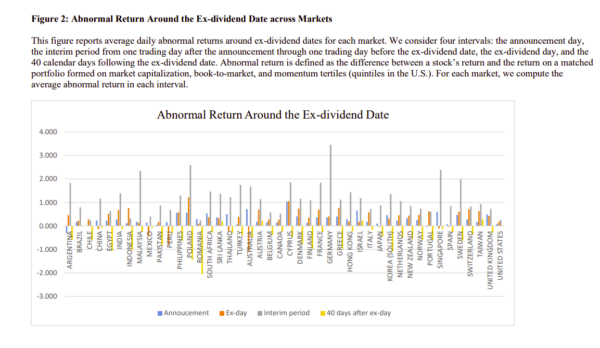

One of the paper’s most important findings is that dividend demand is highly predictable. Dividend-paying stocks earn substantially higher returns during months when they are expected to go ex-dividend. Specifically, dividend payers earn 1.47% in predicted ex-dividend months versus 0.94% in non-ex-dividend months and the payer-minus-nonpayer spread rises to 1.01% during dividend months. Daily data reinforce this conclusion. Prices rise between the dividend announcement and the ex-dividend date, followed by only a partial reversal afterward. This pattern is consistent with temporary buying pressure from dividend-seeking investors.

Dividend clustering amplifies returns

Dividend events are not evenly distributed throughout the year. In many countries, firms cluster dividend payments into specific months due to fiscal year-end conventions and payout practices. For example: nearly 60% of Japanese firms go ex-dividend in March, 34% of Korean firms cluster in December and 39% of Italian firms cluster in May. The paper finds that greater clustering significantly increases the dividend premium. A one-standard-deviation increase in ex-dividend clustering predicts a 0.18% higher dividend premium in the same month the following year.

Global dividend premia move together

Dividend premia are not isolated country-level effects. Markets with aligned dividend calendars experience stronger co-movement in dividend premia. When payout schedules overlap internationally, investor demand shocks become synchronized across countries. The effect is economically large. Above-median calendar overlap roughly doubles a country’s sensitivity to global and regional dividend-premium factors. This creates a new explanation for global dividend-style factors rooted in payout timing rather than macroeconomic risk alone.

Governance matters

The persistent component of the dividend premium is strongest in weaker institutional environments. The premium is larger in markets with: lower liquidity, poorer investor protection, weaker securities regulation and pre-IFRS accounting environments. This suggests investors value dividends more when corporate governance is less reliable. Dividends act as a credible mechanism for returning cash to shareholders.

Taxes do not fully explain the premium

Traditional tax-based explanations struggle to explain the findings. The paper shows that dividend premia remain strong even in countries where dividends and capital gains are taxed similarly, or not taxed at all. Hong Kong is a notable example. This weakens the view that dividend premia are simply compensation for dividend taxation.

Practical Applications for Investment Advisors

Dividend investing is more than yield

Dividend-paying stocks may benefit from predictable investor demand, especially around concentrated payout periods. Advisors should recognize that dividend-related return dynamics extend beyond fundamentals alone.

Timing matters

Dividend calendars create recurring seasonal effects. Understanding when dividend demand concentrates may help explain short-term relative performance within equity markets.

Global diversification can alter dividend exposure

Dividend timing differs significantly across countries. International diversification changes not only sector and valuation exposure, but also the timing structure of dividend demand.

Governance still matters

The persistent dividend premium is stronger where governance quality is weaker. In some markets, dividends function as a signal of shareholder protection and capital discipline.

How to Explain This to Clients

“Dividend-paying stocks tend to outperform globally, but not only because of the dividends themselves. Investors often buy dividend stocks ahead of payout dates, creating predictable demand that pushes prices higher. Because many companies pay dividends at similar times, this effect can become large enough to influence entire markets. At the same time, dividends also matter because they signal financial discipline. In markets where governance is weaker, investors place even greater value on companies that consistently return cash to shareholders.”

The Most Important Chart from the Paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Using data from 44 international equity markets, we document a robust dividend premium of 0.58%

per month after controlling for global and regional risk factors. We decompose this premium into

a timing-related component and a persistent component. The timing-related component arises in

predictable dividend months: dividend payers earn return run-ups around clustered ex-dividend

dates that only partially reverse, leaving a residual that does not wash out. Within markets, the

premium is stronger when ex-dividend dates are more concentrated. Across markets, dividend

premia co-move more strongly when payout calendars overlap, consistent with synchronized

cross-market demand shocks. The persistent component survives outside dividend months and is

larger in weaker institutional environments (weaker investor protection, poorer disclosure and

securities regulation, and lower liquidity). Together, the evidence shows that predictable payout

timing generates both return premia and international return co-movement.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.