Index investing is often seen as passive. Mechanical. Almost indifferent to market conditions. This paper challenges that perception. It shows that the way indexes rebalance can systematically shift exposure between stocks at different points in the cycle, creating something that looks surprisingly like market timing.

Index rebalancing and stock market composition: Do indexes time the market?

- Marco Sammon and John J. Shim

- Journal of Financial Economics, 2026

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

• Index rebalancing is not neutral. It changes market exposure over time

Indexes add and remove stocks based on rules like market capitalization and eligibility. These changes are not random. They systematically increase exposure to stocks that have recently performed well and reduce exposure to those that have underperformed. This creates a dynamic shift in the composition of the market portfolio.

• Indexes implicitly buy high and sell low but not always inefficiently

At first glance, rebalancing looks like forced momentum. Winners enter or gain weight. Losers exit or shrink. However, the paper shows this behavior can align with economic conditions. In some cases, indexes increase exposure to stocks when expected returns are lower and reduce exposure when expected returns are higher, creating a timing effect.

• Market composition evolves with cycles

During expansions, high-performing stocks grow in weight and dominate indexes. During downturns, rebalancing gradually shifts exposure away from these names. This means the “market portfolio” itself is not static. It reflects past performance and embeds cyclical biases.

• Index changes affect returns and risk

Because rebalancing alters which stocks are held and in what proportion, it impacts both expected returns and risk. The paper shows that changes in index composition can explain part of the variation in aggregate market returns over time.

• Passive investing is not purely passive

Even without discretionary decisions, index rules generate systematic trades. These trades can resemble timing strategies. The implication is that passive investors are indirectly exposed to a form of rules-based market timing.

Practical Applications for Investment Advisors

• Understand what “the market” really is

The market index is not a fixed benchmark. It evolves with performance. When you allocate to an index, you are implicitly accepting its rebalancing logic and the timing effects embedded in it.

• Be aware of concentration risk

Index rebalancing can lead to increased concentration in recent winners. This can amplify exposure to sectors or themes at their peak. Monitor concentration and consider complementary strategies to diversify

• Combine passive with intentional tilts

Since indexes already embed momentum-like behavior, layering additional momentum strategies may lead to overlap. Instead, consider balancing with value, quality, or equal-weight approaches.

• Rebalancing frequency matters

Different index methodologies lead to different timing effects. Understanding how often and how aggressively an index rebalances can help in selecting benchmarks aligned with your investment philosophy.

• Use index behavior as a signal

Changes in index composition can provide information about market dynamics. Large shifts in weights or constituents may reflect broader trends in risk appetite or economic conditions.

How to Explain This to Clients

“Even passive investing involves decisions, just not human ones. Indexes follow rules that automatically shift money toward companies that have grown and away from those that have shrunk. Over time, this creates a subtle form of market timing. Understanding this helps us build portfolios that are truly diversified, not just passively allocated.”

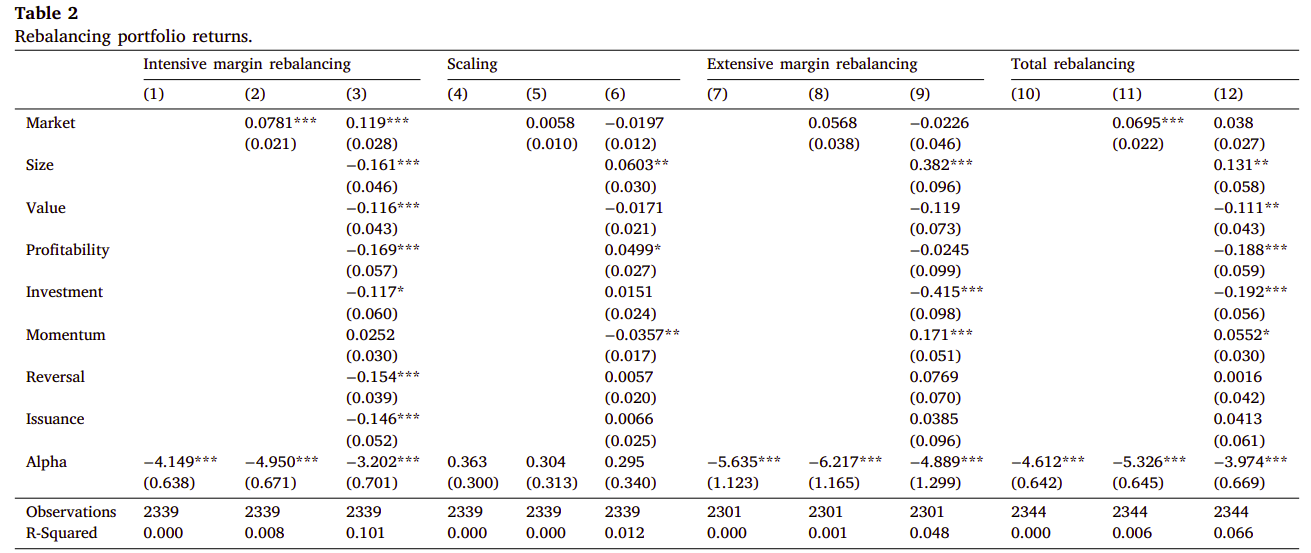

The Most Important Chart from the Paper

Table 2 : This table presents regressions of our rebalancing and scaling portfolios’ returns on asset pricing factors for value-weighted index funds tracking the S&P 500, 400, and 600, the Russell 1000, 2000, and 3000, and the CRSP market-capitalization based indexes. The intensive margin captures rebalancing activity for existing positions. The scaling portfolio is based on how the index fund is predicted to scale existing holdings up and down based on flows. The extensive margin portfolio is long/short stocks added/dropped by the index fund. The total rebalancing portfolio is composed of all intensive and extensive margin rebalancing trades. Portfolios are constructed in quarter 𝑡 to examine returns

in 𝑡+ 1. We use quarterly index fund holdings data from 1996.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Value-weighted indexes must rebalance in response to stock market composition changes, e.g., issuance, buybacks, and IPOs. In doing so, existing index funds implicitly engage in market timing. Index funds’ long-short rebalancing portfolios have an annualized return of 4.61% and load negatively on value and profitability factors. We estimate these trades impose a 46–69 bps annual index-level performance drag. We explore alternative value-weighted indexes that rebalance less and delay responding to compositional changes. Despite still closely tracking the market, these indexes improve market timing and lower trading costs, saving 50 bps annually, an order of magnitude greater than index fund fees.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.