Asset prices are often viewed through a simple lens. Investors form expectations, discount future cash flows, and determine prices accordingly. But in reality, expectations themselves are complex. They vary across institutions, across asset classes, and over time. This paper introduces a new perspective. Institutional expectations are not random or purely behavioral. They are structured, data-driven, and closely tied to economic fundamentals. The result is a powerful insight. Institutional investors largely behave in line with rational asset pricing models. Yet at the same time, they strongly disagree with each other, and this disagreement has important implications for markets.

Institutions’ return expectations across assets and time

- Magnus Dahlquist , Markus Ibert

- The Journal of Financial Economics, 2026

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

Institutional expectations align with rational models

The paper shows that subjective risk premia from institutional investors and professional forecasters move closely with objective, model-based risk premia. These objective measures are countercyclical. They rise in recessions and fall in expansions. The fact that subjective expectations move one-to-one with them supports the idea that time-varying risk premia are central to asset pricing.

Time variation in expected returns is systematic

Across equities, credit, and cash, institutional expectations track well-known predictors such as valuation ratios and term premia. This suggests that expected returns are not arbitrary. They respond to economic conditions in a predictable way.

Disagreement across institutions is large and persistent

Despite strong alignment in the time series, expectations differ significantly across institutions at any given point in time. In many cases, this cross-sectional variation is larger than the variation over time. This highlights that disagreement is a core feature of financial markets.

Valuation assumptions drive most of the disagreement

The main source of disagreement is not growth or inflation. It is valuation. Specifically, institutions differ in their assumptions about how price-earnings ratios evolve over time. Some expect mean reversion. Others assume valuations persist. This single difference explains most of the variation in expected equity returns.

A common framework underlies expectations

Most institutions use a “building-block” approach. Expected returns are decomposed into income, growth, inflation, and valuation changes. While the framework is shared, the inputs differ. This leads to very different outcomes.

Risk expectations are consistent across asset classes

Institutions form coherent views across markets. An investor that is optimistic about equities is typically also optimistic about credit and other risky assets. This reflects a macro-driven process where expectations about growth and inflation feed into multiple asset classes.

Retail and institutional investors behave differently

Unlike retail investors, who often extrapolate recent returns, institutional investors’ expectations are countercyclical. They increase expected returns when markets fall and decrease them when markets rise. This distinction is critical for understanding market dynamics.

Practical Applications for Investment Advisors

Understand who drives market expectations

Small differences in valuation expectations can lead to large differences in expected returns. Advisors should pay close attention to assumptions about long-term valuation levels when building capital market expectations.

Recognize persistent disagreement

There is no single “correct” expected return. Even sophisticated institutions disagree significantly. This reinforces the importance of diversification and robust portfolio construction.

Incorporate macro-driven thinking

Return expectations across asset classes are interconnected. Growth, inflation, and interest rates shape expectations broadly. Portfolio decisions should reflect this integrated perspective.

How to Explain This to Clients

“Professional investors don’t all see the market the same way. Even when they use similar models, small differences in assumptions can lead to very different expectations about future returns.What matters is that these expectations are not random. They tend to rise when markets are stressed and fall when markets are strong. This is how markets adjust to risk.At the same time, disagreement is normal. That’s why diversification is so important. It helps manage the uncertainty that comes from different views about the future.”

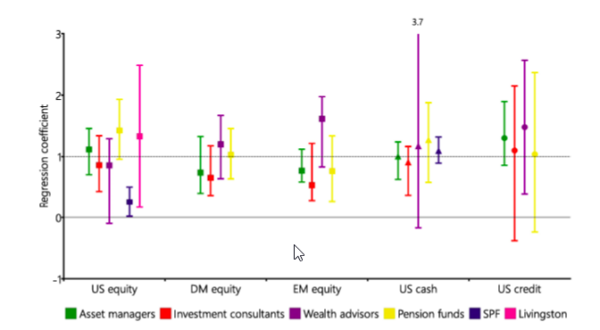

The Most Important Chart from the Paper

In Figure 1 we can see regression coefficients with 95% confidence bands. The figure plots the slope coefficient estimates of Table 3 together with their 95% confidence bands. The upper part of the band for wealth advisors’ cash risk premium is 3.715 and outside the plotted range.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

We study the equity, cash, and corporate bond risk premium expectations of asset managers, investment consultants, wealth advisors, public pension funds, and professional forecasters. Subjective risk premia vary one-to-one with objective risk premia that are available in real time and countercyclical. Despite their significant time-series variation, several subjective equity premia vary more in the cross-section of institutions than in the time series. This heterogeneity persists both over time and across asset classes. We tie the heterogeneity in subjective equity return expectations to heterogeneous expectations about long-term equity valuations: some institutions believe that the price–earnings ratio behaves like a random walk, whereas others believe in varying degrees of mean reversion.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.