“Buy the dip” (BTD) has become one of the most popular investment mantras of recent years, especially since the COVID-19 market recovery in 2020.

The strategy seems intuitive: when markets fall, buy at a discount and wait for the inevitable rebound. However, BTD is not foolproof. By design, it performs well when market declines are brief, but poorly when declines mark the beginning of a prolonged drawdown. A new paper from AQR Capital Management, “Hold the Dip,” examines the empirical evidence and puts this popular strategy to the test.

What the Authors Examined

The research team at AQR conducted a comprehensive analysis of “Buy the Dip” (BTD) strategies applied to the S&P 500 from January 1965 to September 2025. Rather than testing just one version of the strategy, they created 196 different variations by combining:

- Four dip depths: 5%, 10%, 15%, and 20% price declines.

- Seven dip lengths: ranging from one week to one year.

- Seven holding periods: from one month to five years.

For each variation, the strategy bought the S&P 500 after a specified decline and held it for the designated period, remaining in three-month T-bills otherwise. The authors then compared these BTD strategies against simple buy-and-hold investing.

The Key Findings: BTD Disappoints

1. Lower Risk-Adjusted Returns Than Passive Investing

Across all BTD strategies, the average Sharpe ratio (SR) was -0.04 less than equities (about a 16% degradation to holding equities passively), with over 60% of BTD implementations underperforming by this metric. Using more recent data from 1989 onward, the picture was even worse—the SR of these strategies was -0.27 worse than holding equities passively—a 47% degradation in risk-adjusted returns.

2. No Meaningful “Alpha”

Even when accounting for the fact that BTD strategies spend time in cash (and thus have less market exposure), the authors found minimal evidence that BTD adds value. The average alpha across all implementations was just 0.5% per year, and only 16 of the 196 strategies (just 8%) showed statistically significant outperformance. In other words, BTD doesn’t appear to offer reliable market-timing ability.

3. The Momentum Problem

Why does BTD underperform? The authors identified a crucial insight: BTD is essentially “value investing at a momentum horizon.”

Markets tend to exhibit momentum over weeks and months—trends continue in the short term. Meanwhile, value strategies (buying when prices are depressed) tend to work over much longer periods of years. BTD tries to catch reversals at precisely the wrong timeframe, positioning investors against prevailing market trends.

4. Trend-Following Works Better

When the authors compared BTD to trend-following strategies (which buy when prices are rising and sell when falling), trend-following significantly outperformed. The SG Trend Index, representing major trend-following managers, delivered a 4.7% alpha to equities with a near-significant statistical result—far better than BTD’s 0.5% average alpha.

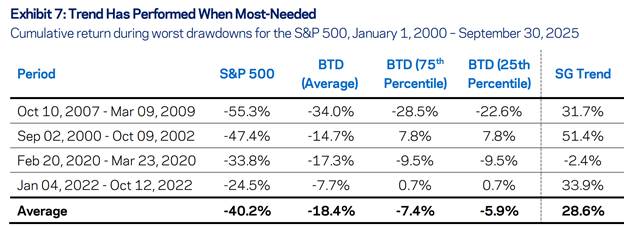

Most importantly, trend-following strategies excelled during major market downturns. During the four worst S&P 500 drawdowns since 2000 (each exceeding 20%), trend-following delivered an average return of +28.6%, while the average BTD strategy lost 18.4%. BTD tends to maintain long positions during extended declines, exposing investors to losses precisely when they can least afford them.

It’s important to note that all the BTD results were before considering any implementation costs.

Investor Takeaways

1. Don’t Confuse Long-Term Optimism with Market Timing

Just because stocks tend to go up over time doesn’t mean buying dips is a superior strategy. The belief that “prices will eventually be higher” was true before, during, and after any dip. BTD only makes sense if it identifies periods with better-than-normal near-term prospects—and the evidence suggests it doesn’t.

2. Beware of Recency Bias

Interest in BTD surged after the quick 2020 COVID recovery and the 2025 “Liberation Day” rebound, but plummeted during the extended 2022 drawdown. Strategies that only look good after short, sharp declines may leave you exposed during the prolonged downturns that pose the greatest threat to long-term goals.

3. If You Want to Time Markets, Align with Momentum

The research suggests that if investors insist on tactical timing, they’re better off following trends rather than fighting them. Trend-following has historically provided diversification benefits and downside protection during extended market stress.

4. Consider “Portable Alpha” Approaches

For investors who want exposure to trend-following but don’t want to sacrifice equity returns, the authors highlight “portable alpha” strategies that combine trend-following with full market exposure. These approaches aim to add alpha without giving up beta.

5. Stick with Strategic Asset Allocation

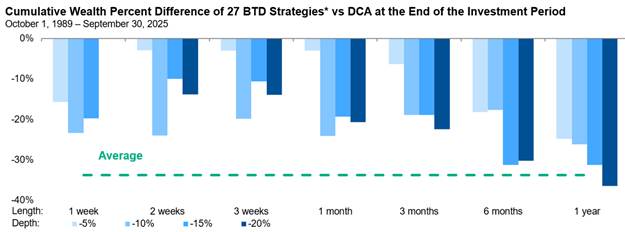

Perhaps the simplest takeaway: for most investors, maintaining a strategic allocation and staying invested is likely to outperform trying to time dips. If you have cash to invest, the evidence suggests investing sooner rather than waiting for a decline is the more reliable approach. As further support for staying the course, AQR’s team addressed the question: “What if I plan to invest part of my paycheck every month in the market. Am I better off investing as soon as the check clears, or waiting until I see a dip?” Comparing BTD to the well-known dollar cost averaging method they found that on average BTD resulted in 18.7% lower ending wealth.

The Bottom Line

“Buy the dip” makes for a catchy slogan, but it doesn’t hold up as a systematic strategy. The research reveals that BTD typically positions investors opposite to momentum, leading to underperformance—especially during the extended downturns when protection matters most.

Rather than trying to catch falling knives, investors may be better served by either staying consistently invested or, if they insist on tactical positioning, aligning with rather than against market trends. As the authors conclude, while BTD has captured investors’ imagination, it hasn’t captured excess returns.

Larry Swedroe is the author or co-author of 18 books on investing, including his latest Enrich Your Future.

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.