Core Research Categories

Click Here for Category Archive

Resurrecting the Value Premium

May 4th, 2021|

How Portfolio Construction Impacts the Reliability of Outcomes

April 16th, 2021|

Inflation and the Value Premium

April 15th, 2021|

Democratize Quant Conference Recap and Materials

March 25th, 2021|

The Forecasting Power of Value, Profitability, and Investment Spreads

February 25th, 2021|

Will the Real Value Factor Funds Please Stand Up?

February 8th, 2021|

Click Here for Category Archive

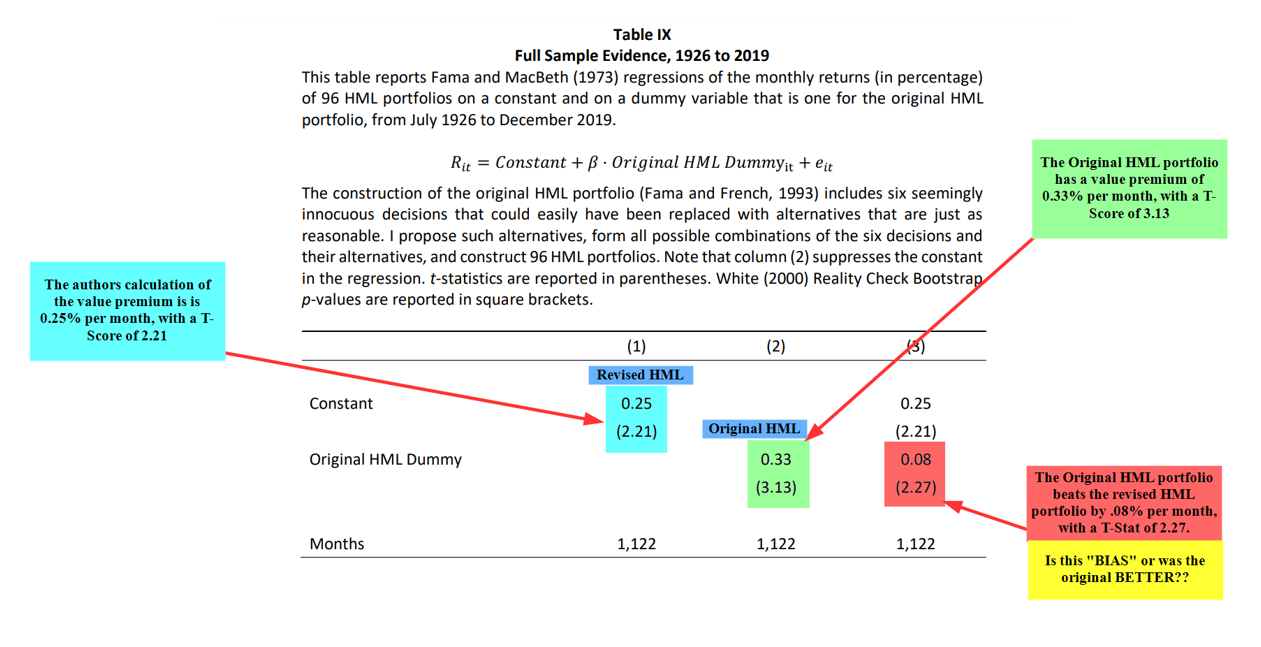

Is The Value Premium Smaller Than We Thought?

February 3rd, 2022|

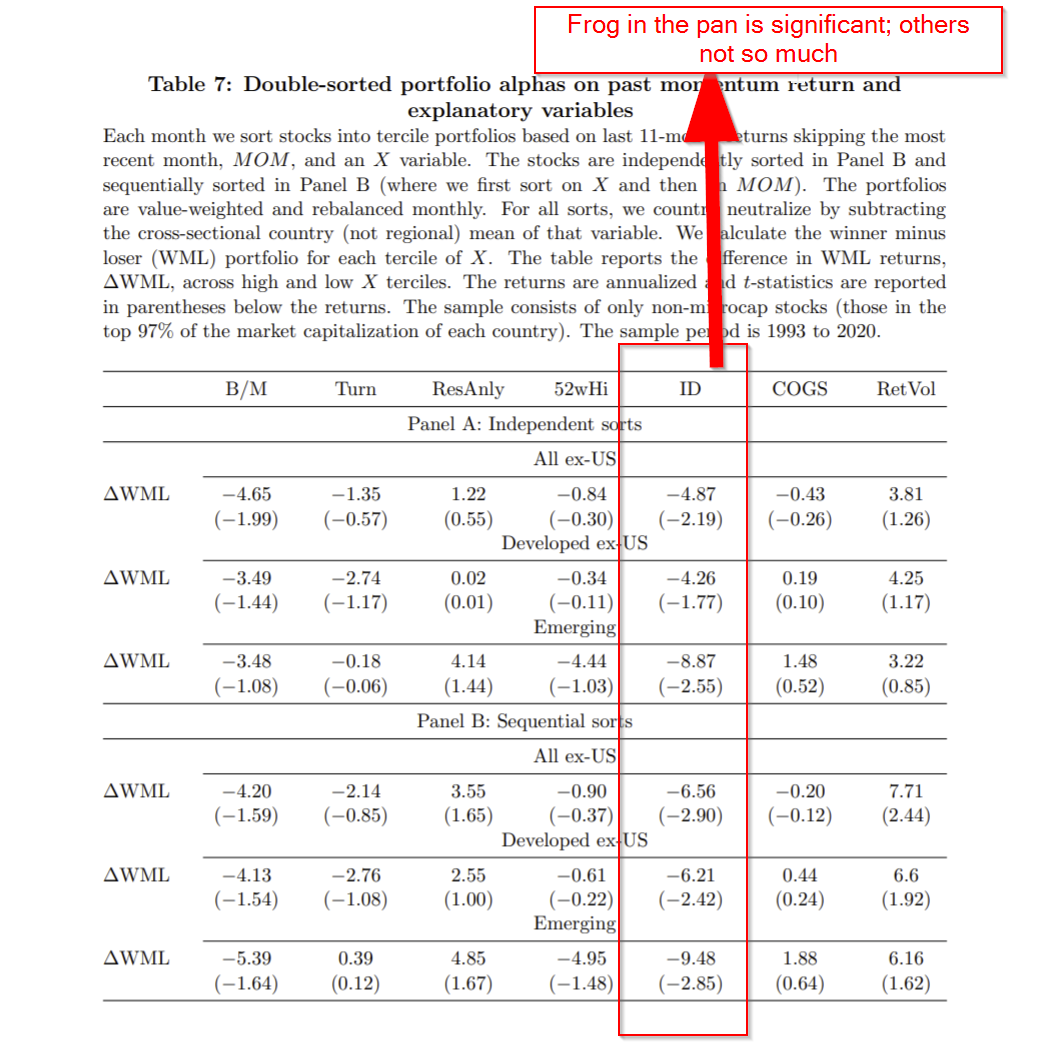

What Explains the Momentum Factor? Frog-in-the Pan is Still the King.

February 1st, 2022|

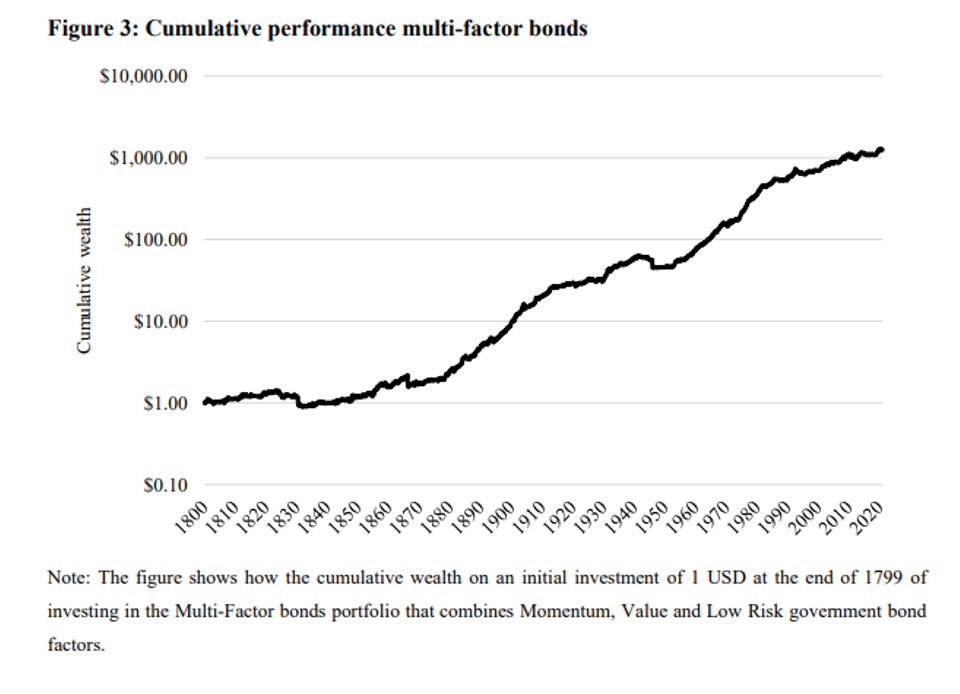

Factor Investing in Sovereign Bond Markets

January 13th, 2022|

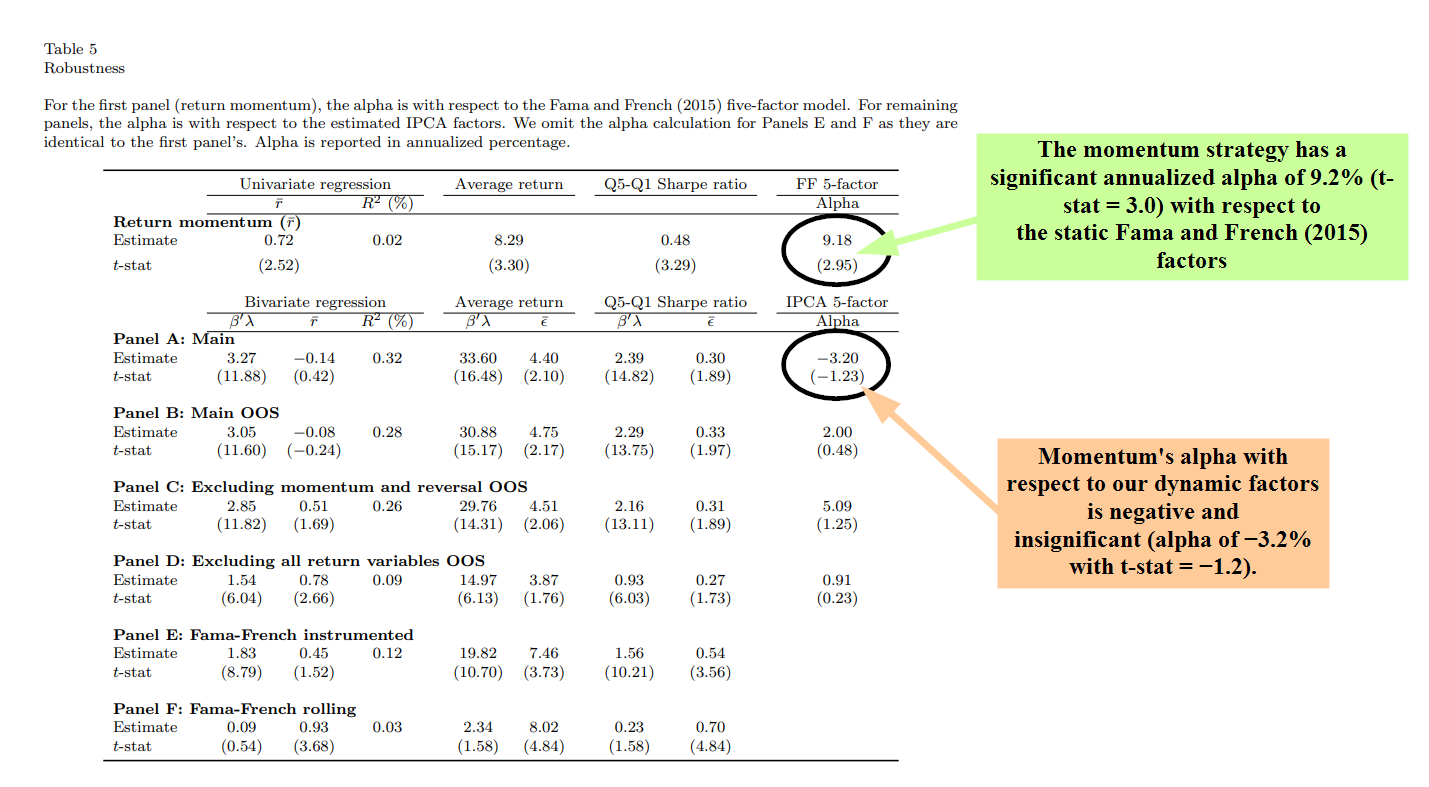

Understanding Momentum Investing

December 30th, 2021|

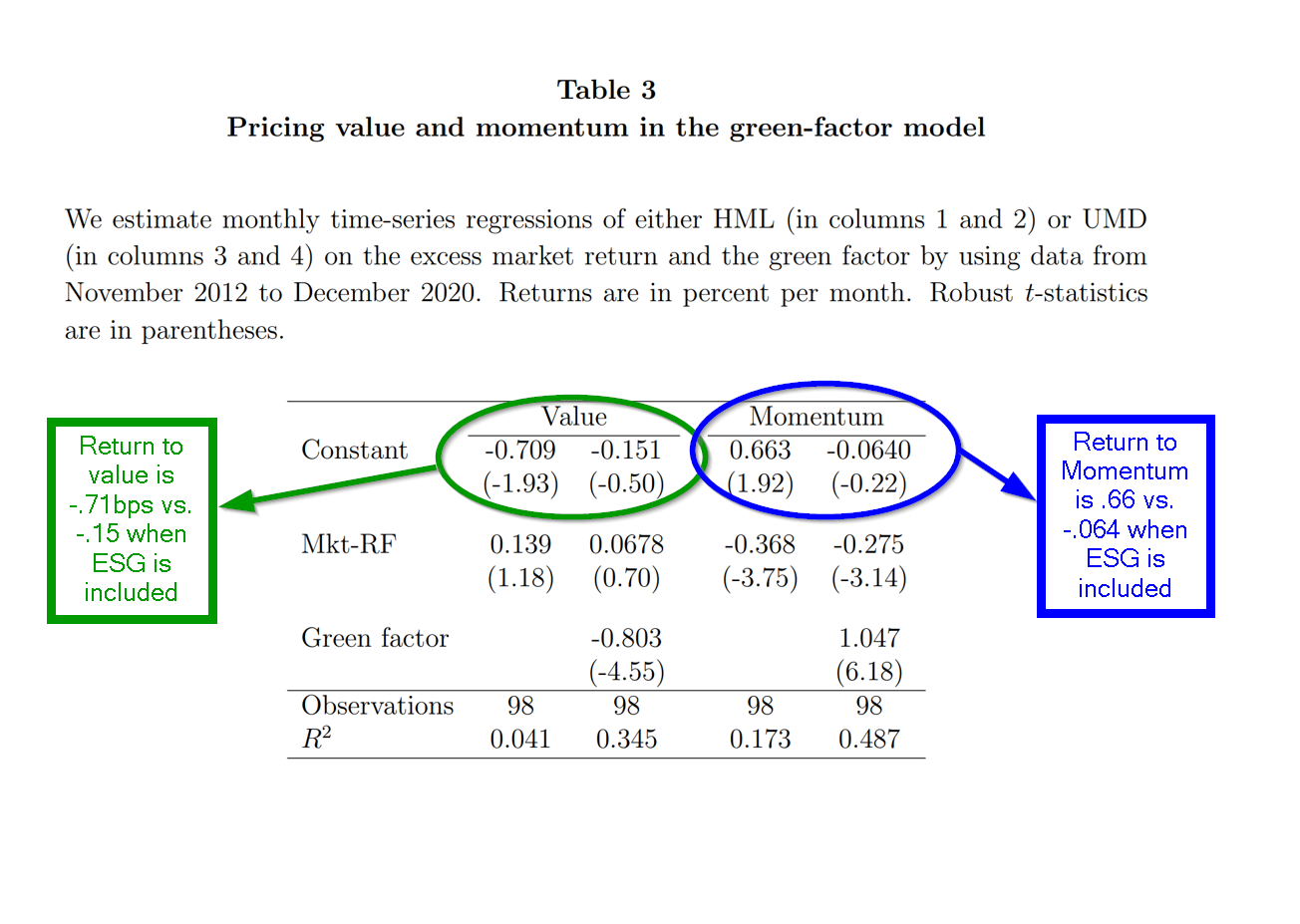

ESG Investing: Dissecting Green Returns

December 13th, 2021|

Factor Investing Deep Dive with Jack Vogel

November 12th, 2021|

Click Here for Category Archive

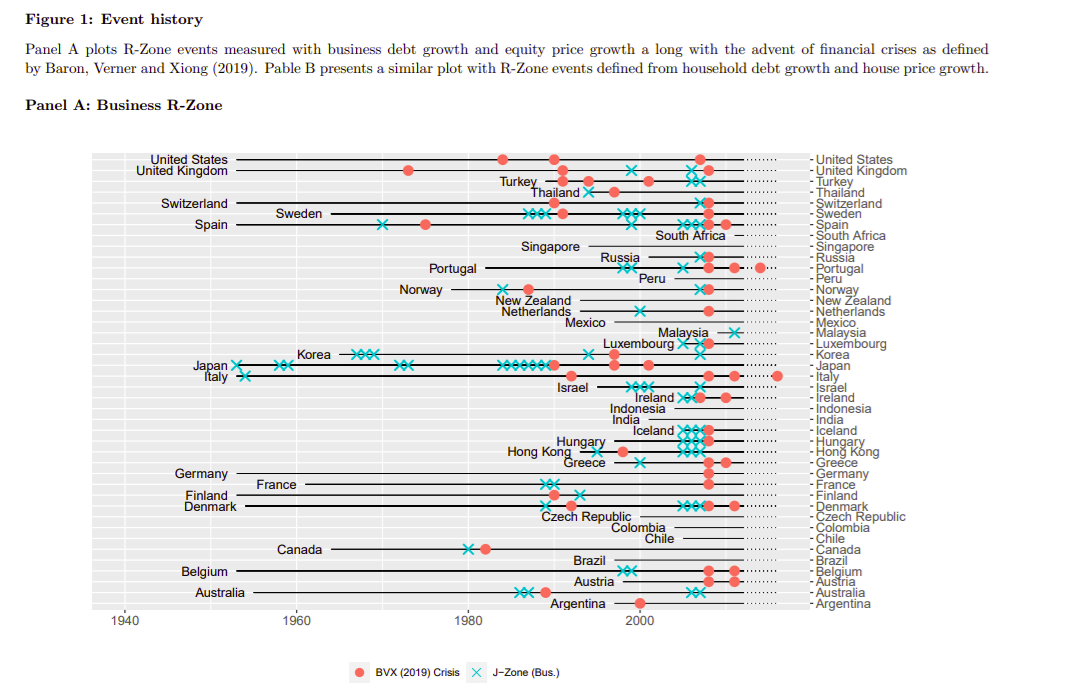

Are Financial Crises Predictable?

March 14th, 2022|

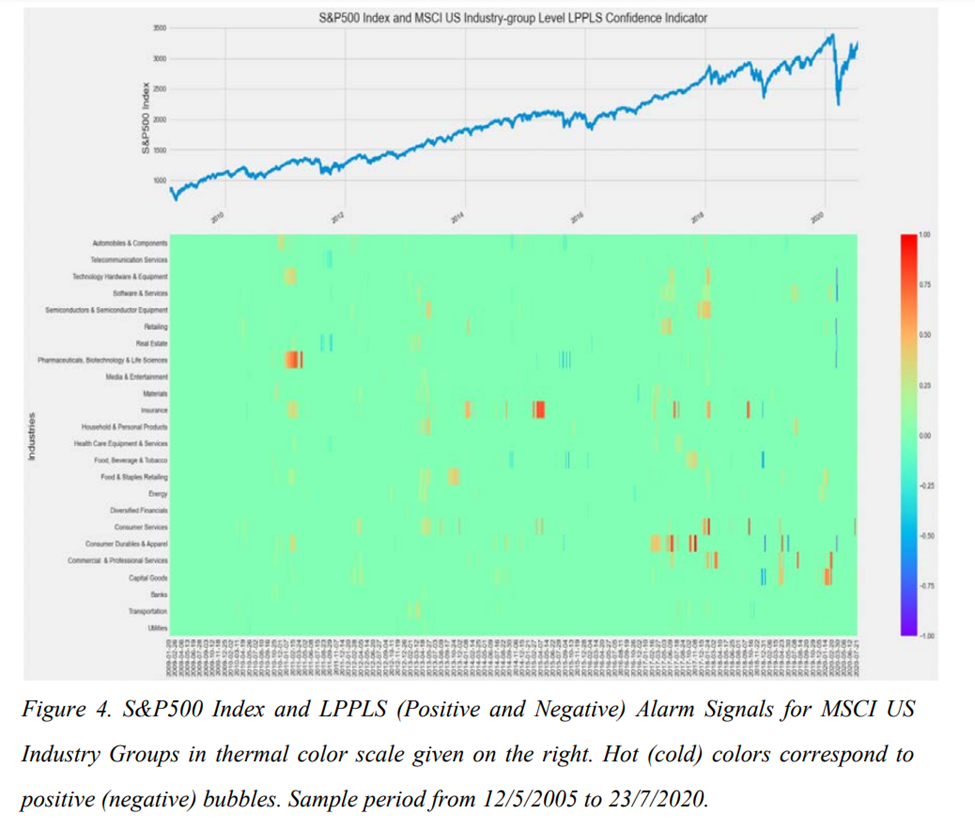

Are Stock Market Bubbles Identifiable?

March 31st, 2022|

Using Momentum to Find Value

May 5th, 2022|

Trend Following: Timing Fast and Slow Trends

May 19th, 2022|

Strategies to Mitigate Tail Risk

May 26th, 2022|