Core Research Categories

Click Here for Category Archive

Increases CAPE Ratio Predictability with a Simple Adjustment

March 23rd, 2026|

Revaluation Alpha: Why Past Factor Returns May Be Misleading

January 30th, 2026|

Is Value Investing Dead?

January 23rd, 2026|

Intelligent Concentration: A Synopsis of Warren Buffett and Diversification

September 12th, 2025|

Equity duration and predictability

September 8th, 2025|

Click Here for Category Archive

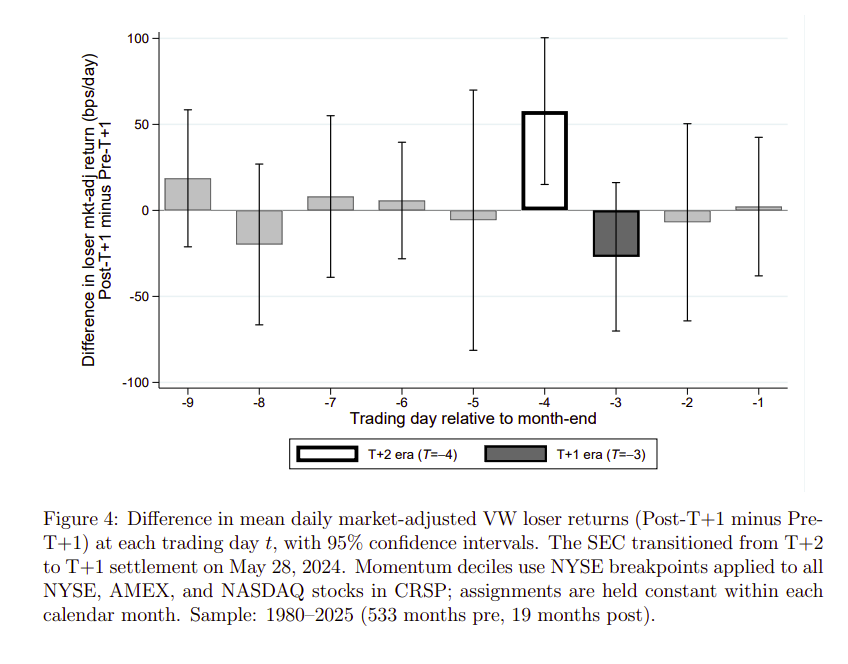

The Intramonth Momentum Cycle

July 13th, 2026|

Should Your Mom Have Private Equity in Her 401K?

May 4th, 2026|

Click Here for Category Archive

The Global Value Momentum Trend Philosophy

June 6th, 2017|

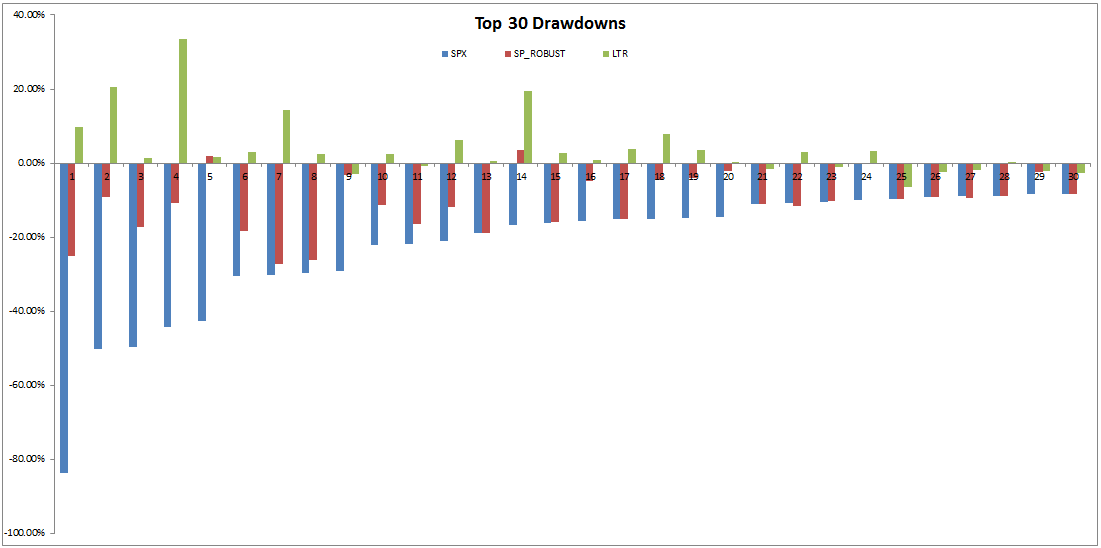

Avoiding the Big Drawdown with Trend-Following Investment Strategies

August 13th, 2015|

The World’s Longest Trend-Following Backtest

November 9th, 2015|

Trend-Following: A Deep Dive Into A Unique Risk Premium

October 18th, 2017|

Are Factors Better and More Diversifying Than Asset Classes?

February 23rd, 2018|

Click Here for Category Archive

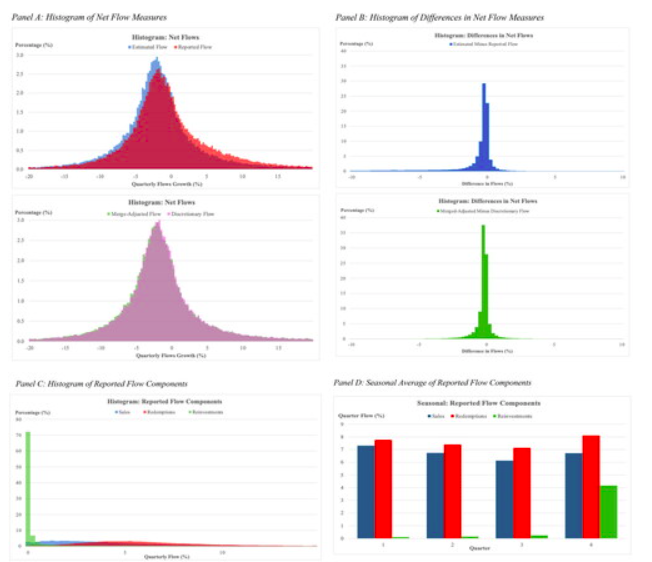

Do Mutual Fund Flows Really Say What We Think They Say?

November 3rd, 2025|

Equity duration and predictability

September 8th, 2025|

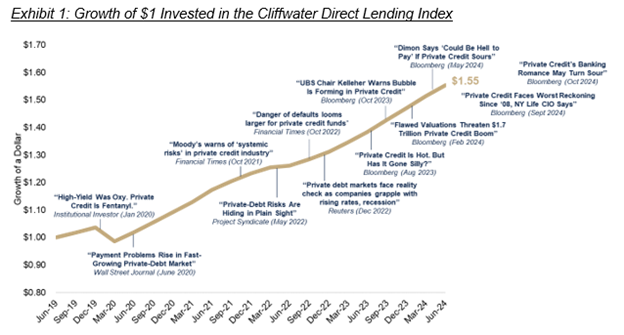

Is There A Bubble In Private Credit?

February 7th, 2025|

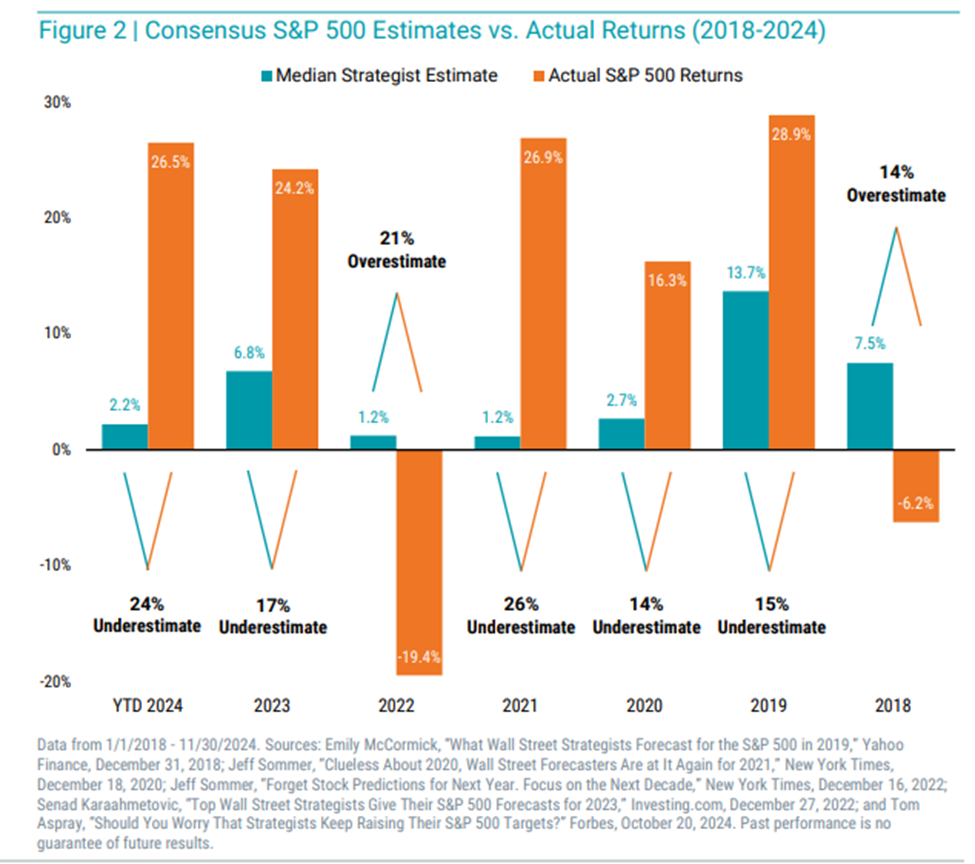

Nine Lessons the Market Taught in 2024

January 31st, 2025|

Long-Only Value Investing: Size Doesn’t Matter!

June 15th, 2023|

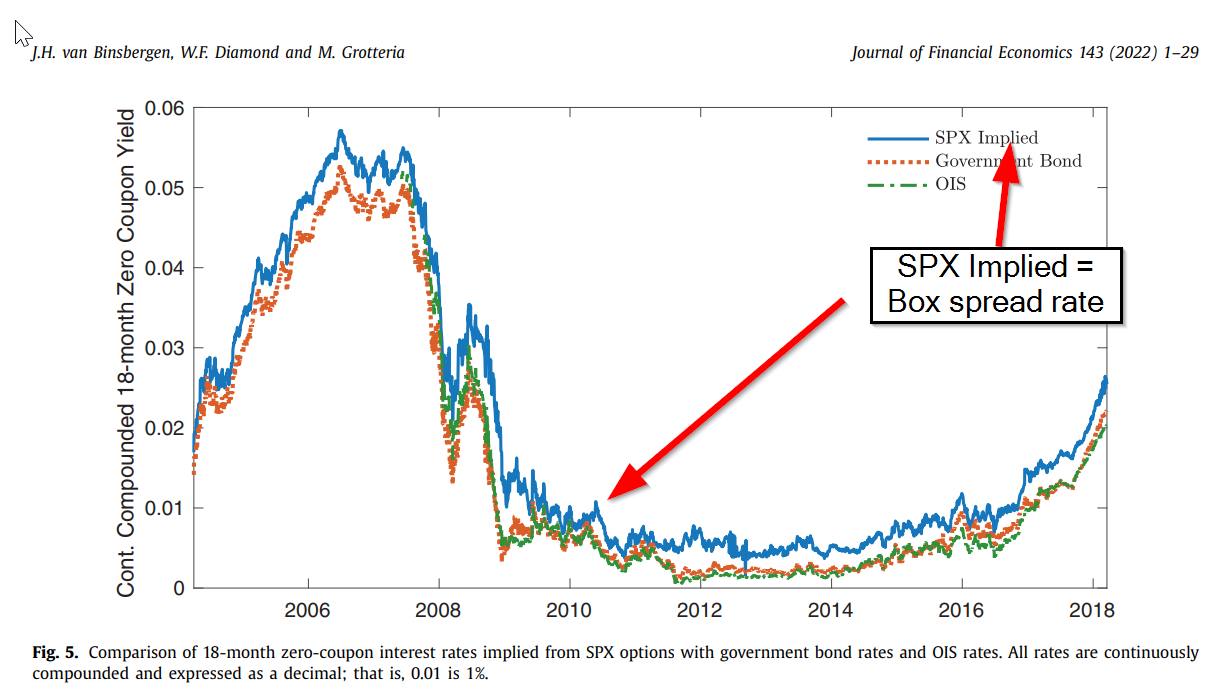

Box Spreads: An Alternative to Treasury Bills?

May 10th, 2023|