Core Research Categories

Click Here for Category Archive

Democratize Quant 2023 is Live. Sign-up!

April 26th, 2023|

How factor exposure changes over time: a study of Information Decay

April 17th, 2023|

Wes Discusses Value Investing Foundations with Isaiah Douglass

April 6th, 2023|

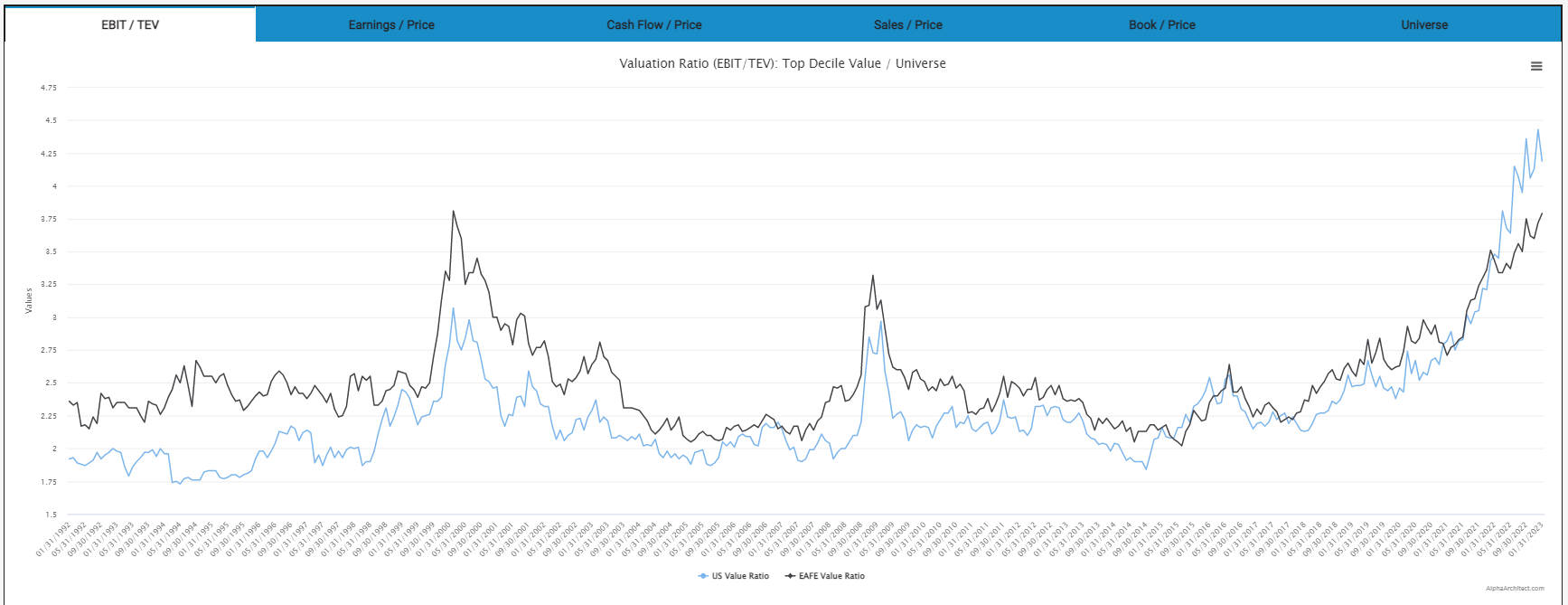

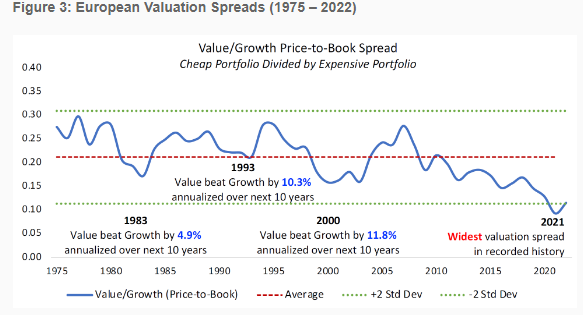

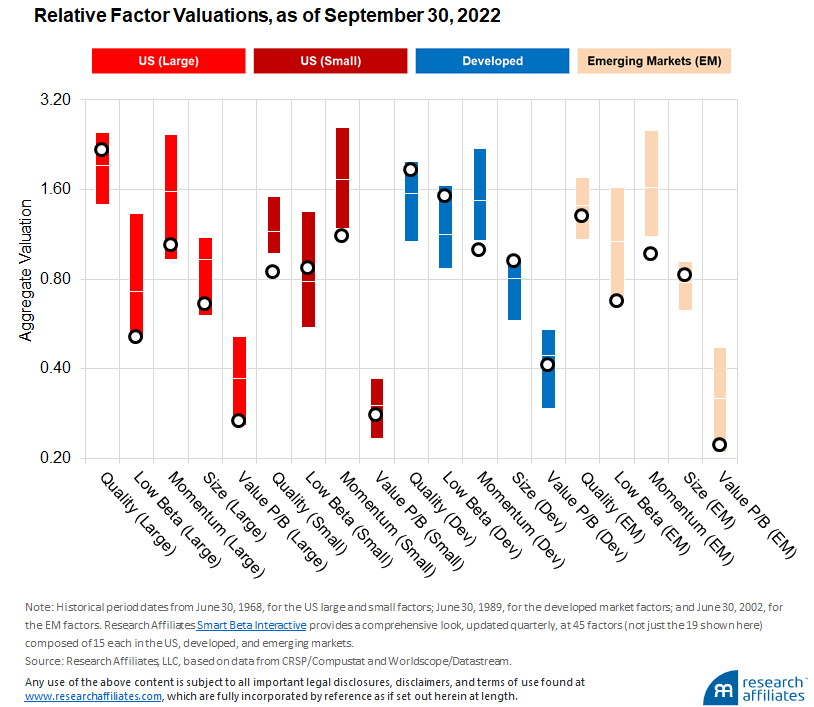

Compression: Can the Value Spread Expand Forever?

March 9th, 2023|

It’s Always Darkest Just Before Dawn

February 17th, 2023|

Factor Returns and the Information in Valuation Spreads

February 10th, 2023|

Click Here for Category Archive

Cut Your Losses and Let Profits Run?

March 1st, 2024|

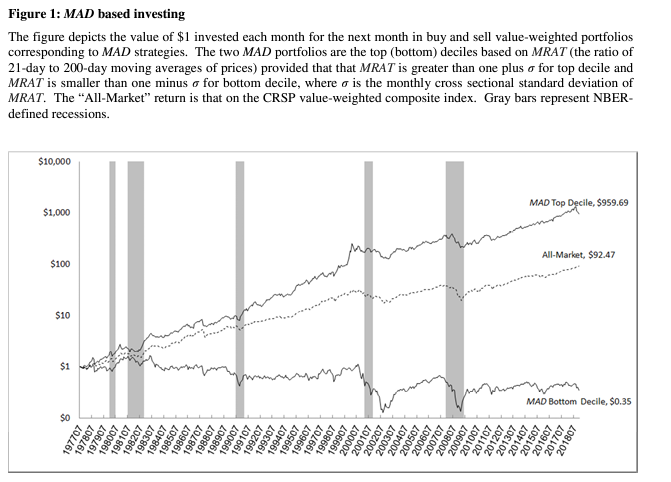

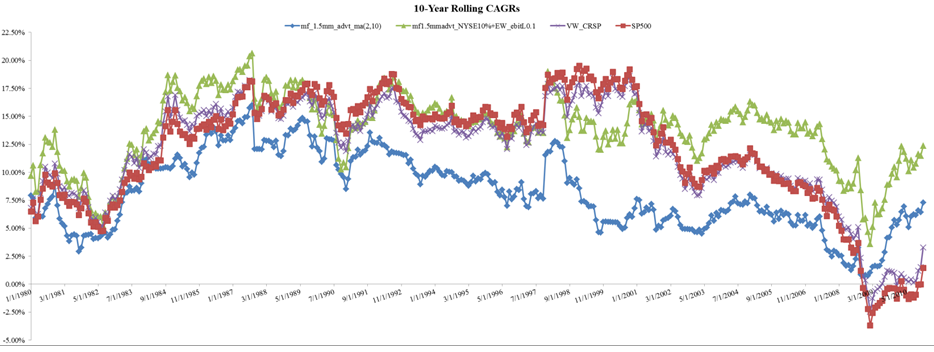

Moving Average Distance and Time-Series Momentum

January 26th, 2024|

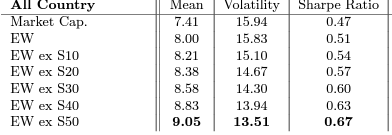

Outperforming Cap- (Value-) Weighted and Equal-Weighted Portfolios

January 19th, 2024|

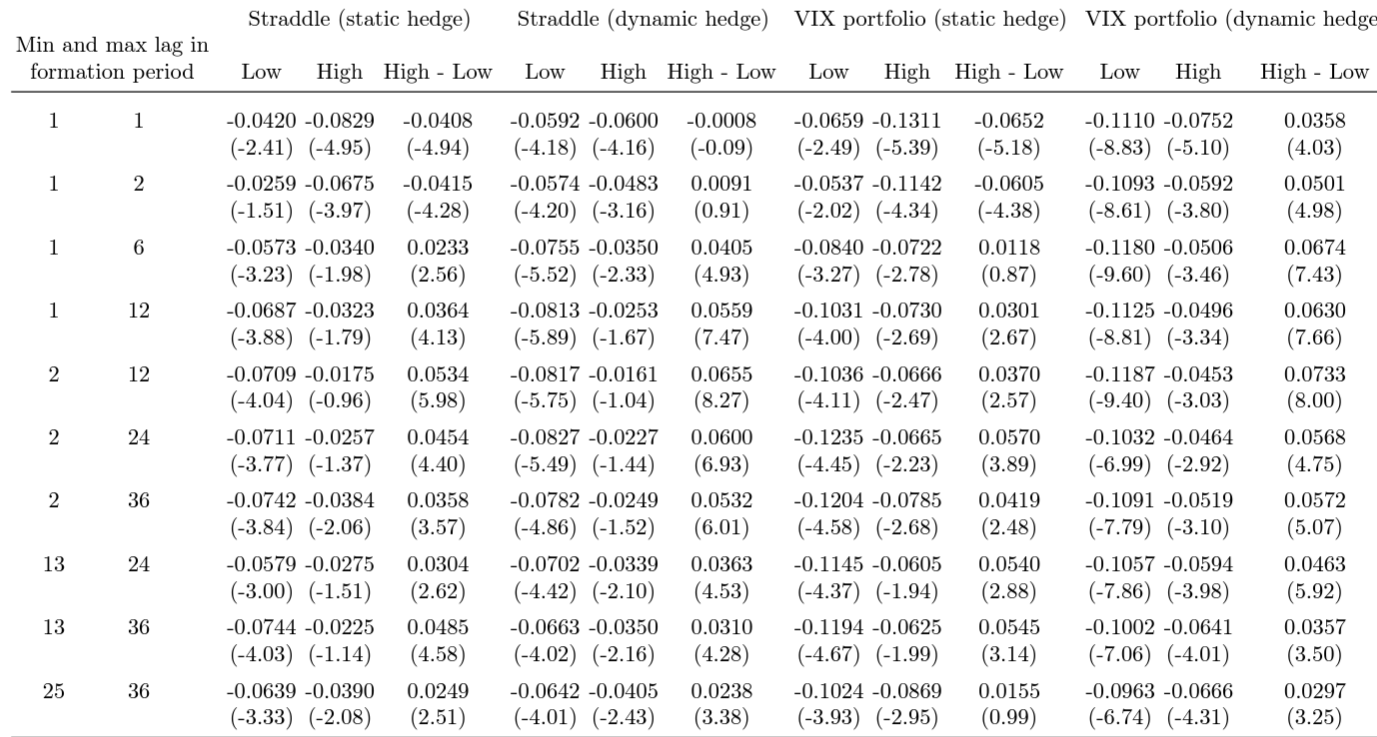

Momentum Everywhere, Including Equity Options

December 22nd, 2023|

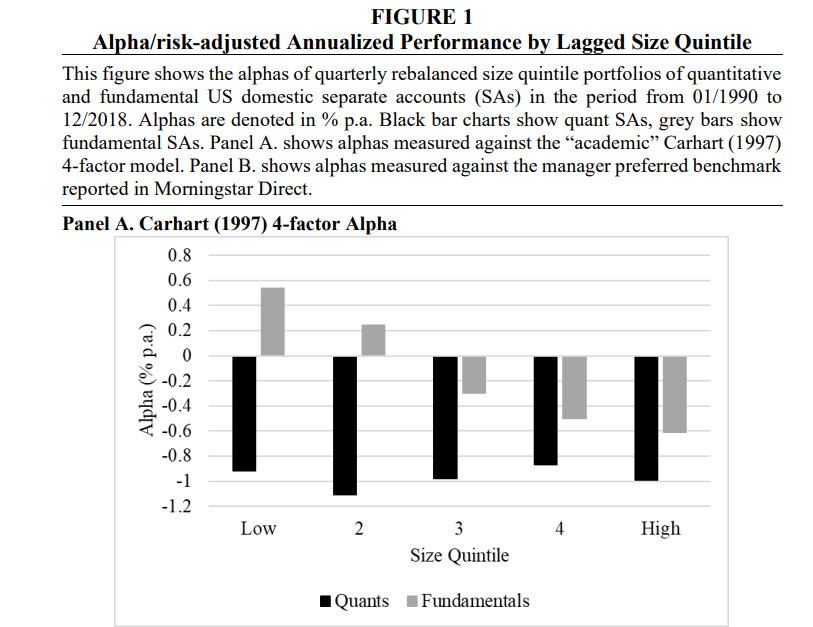

Diseconomies of Scale in Investing

December 8th, 2023|

A new twist on momentum strategies: Utilize overlapping momentum portfolios

November 27th, 2023|

Click Here for Category Archive

Using Trend-Following Rules to Enhance Factor Performance

January 4th, 2017|

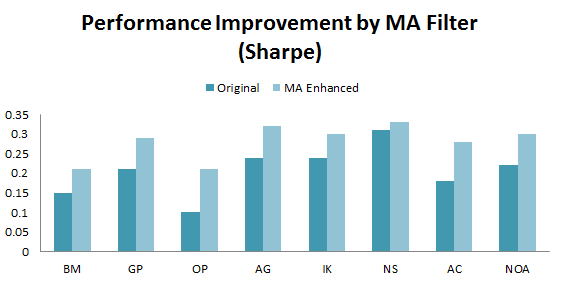

Magic Formula and MA Rules: A Bad Combo!

November 27th, 2011|

What is the correct benchmark for trend following?

October 16th, 2018|

How large is the tracking error created by trend following?

October 25th, 2018|

How to Use Trend Following within a Portfolio

December 4th, 2018|

Click Here for Category Archive

“Alternative” Facts about Formulaic Value Investing

April 22nd, 2017|

Factor Investing is More Art, and Less Science

February 3rd, 2017|

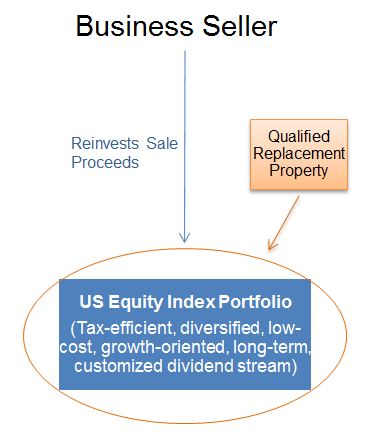

1042 Qualified Replacement Property: An Overview of ESOP Rollover Strategies

December 28th, 2016|

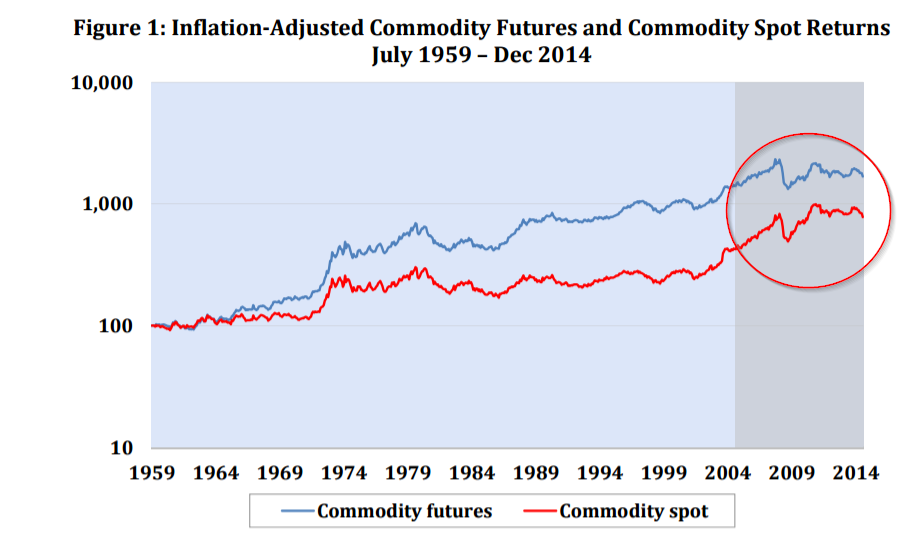

Commodity Futures Investing: Complex and Unique

December 21st, 2016|

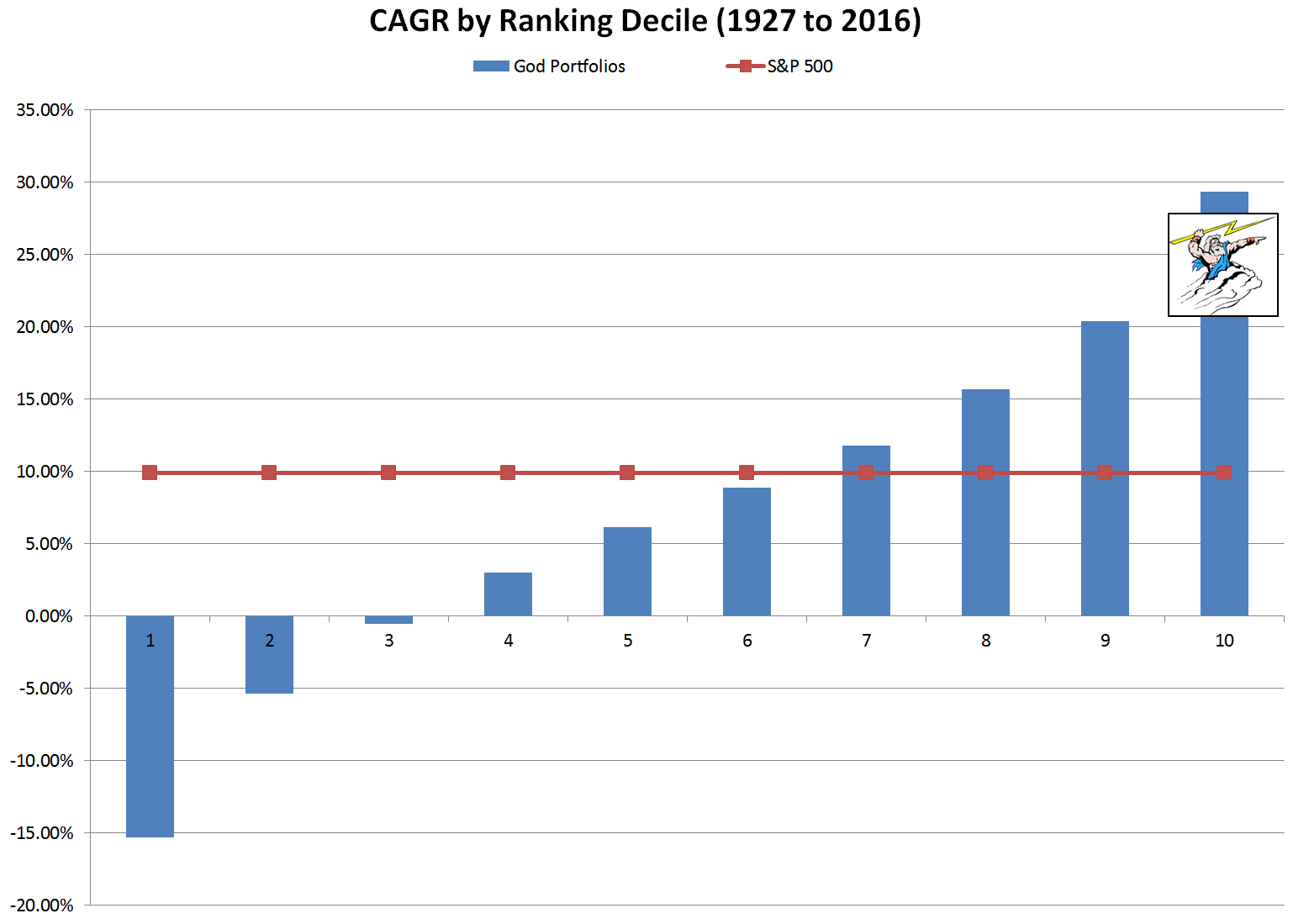

Even God would get fired as an Active Investor

February 2nd, 2016|

The Quantitative Momentum Investing Philosophy

December 1st, 2015|