For decades, traditional commercial banks dominated the mortgage market. However, over the last 20 years, a massive shift has occurred, with “shadow banks”- non-depository institutions like Quicken Loans -capturing nearly half of all originations. While many attribute this to new technology or post-crisis rules, recent research reveals a deeper economic catalyst: the secular decline in interest rates.

The Secular Decline in Interest Rates and the Rise of Shadow Banks

- Sarto and Wang

- Journal of Finance, 2026

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

Regulation triggers credit migration, not just elimination

Falling interest rates act as a “negative shifter” for bank deposit demand. As traditional banks lose their funding advantage, they contract their lending, leading to a migration of credit to the less-regulated shadow banking sector. This is particularly salient for highly levered banks that are more constrained by capital requirements.

The “Net Worth Channel” follows the capital

A persistent decline in rates lowers Net Interest Margin (NIM), which hurts bank profitability and equity growth. Because banks are often constrained by leverage ratios, this loss of internal capital forces them to reduce their overall balance sheet size and loan supply.

The “Cost-Cutting” channel amplifies the shift

Banks respond to lower net interest income by slashing non-interest expenses, specifically salaries and fixed assets like branches. This reduction in physical infrastructure diminishes their ability to originate loans – both standard GSE mortgages and specialized non-GSE loans – effectively ceding the market to shadow banks.

Low rates distort competition independently of technology

While fintech shadow banks are growing, the research shows that non-fintech shadow banks also gained significant market share in counties where local banks were most exposed to falling rates. This confirms that the funding environment, not just better apps, is a primary driver of the shift.

Practical Applications for Investment Advisors

Monitor “Regulatory Leakage” and Systemic Risk

As lending migrates to shadow banks, it moves away from institutions with stable deposits and government backstops toward firms dependent on uninsured wholesale funding. This funding can “quickly evaporate” during financial stress, potentially creating new vulnerabilities in the credit market.

Understand the Impact of Branch Closures

The cost-cutting triggered by low rates means traditional banks are less likely to maintain a physical presence in certain counties. Advisors should recognize that this diminished branch network directly impacts a bank’s capacity to provide credit, regardless of borrower demand.

Use Rate Exposure as an Early Warning System

By monitoring a bank’s historical balance sheet sensitivity to rates, analysts can predict which institutions are most likely to lose market share or contract credit supply during persistent low-rate cycles.

How to Explain This to Clients

“Traditional banks used to have a ‘secret weapon’: your deposits. When interest rates were higher, they earned a big profit just by holding that cheap money. But with rates so low for so long, that advantage has disappeared. Banks are now making less money, closing branches, and lending less, which is why more and more people are getting their mortgages from non-bank online lenders who don’t rely on deposits to operate”

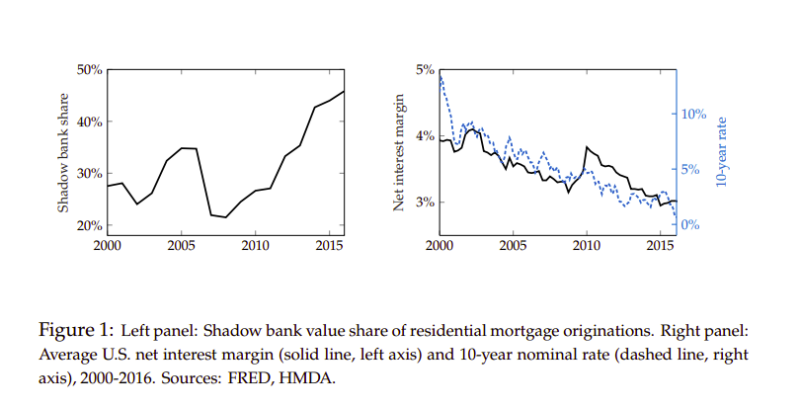

The Most Important Chart from the Paper

Figure 1 shows the Net Interest Margin of U.S. banks falling in lockstep with the 10-year nominal interest rate, alongside a simultaneous and inverse surge in the shadow bank market share.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Over the past two decades, shadow banks have significantly expanded their share of residential mortgage lending, even surpassing pre-financial crisis levels. This surge is often attributed to post-crisis regulatory changes and improvements in shadow banks’ technology. In this paper, we document a new driving force: the persistent decline in interest rates. When interest rates are high, cheap deposit funding provides banks with a significant competitive advantage against shadow banks relying on wholesale funding. As interest rates plummet, banks lose this advantage, experience a squeeze in their net interest margin, leading to diminished profitability, weaker growth, and cost-cutting measures such as branch closures. By contrast, shadow banks are able to gain market share. We test this mechanism using a shift-share empirical design based on differences in historical bank balance sheet composition. We find that banks more vulnerable to falling interest rates contracted lending as a response to lower profitability while also scaling back non-interest expenses on their branches. This created a fertile environment for non-banks to expand in areas with banks exposed to declining interest rates.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.