If you’re a factor investor, there will come a time when you will have to choose between mom and dad: Should you combine or separate your factor exposures? And make no mistake: You will have to make a decision!

While there’s no right answer, the way you structure your portfolio can have significant implications for returns, costs, and even your own behavior as an investor.

Let’s walk through the logic behind both approaches.

Before doing so, if you want to watch the video version of this blog, make sure to check it out here:

The Integrated Approach: One Portfolio to Rule Them All

The integrated approach involves selecting your preferred factors (such as value and momentum), scoring each stock based on a combination of those factors, and investing in the top overall picks.

In practice, this means you don’t end up buying the “top value” and the “top momentum” stocks separately; instead, you select names that score well across both dimensions. This helps avoid owning stocks that are strong on one factor but a nightmare on another.

By doing this, the integrated approach leverages a key insight: value and momentum are negatively correlated. In other words, a stock that looks stellar through a momentum lens might appear unattractive from a value perspective—and vice versa. If you only focus on one factor at a time, you risk ending up with positions that “contradict” each other.

For example, you could end up with a high-momentum stock that’s wildly expensive, or a crashing, dirt-cheap value stock with terrible performance. Integrating helps avoid these extremes by aiming for stocks that are solid from both perspectives.

The Mixed (or Siloed) Approach: Keeping Pure Exposures

The mixed approach builds separate sleeves for each factor. In effect, you’d target the best value stocks and the best momentum stocks while keeping them in their own lanes.

The advantage here is that you can focus on the purest expressions of each factor. Your value sleeve can hold the cheapest stocks available, while your momentum sleeve targets the strongest recent performers. There’s no need to compromise; you can go all-in on each signal.

And here’s where it gets interesting…

Head-to-Head: What the Evidence Says

Let’s bring some data into this.

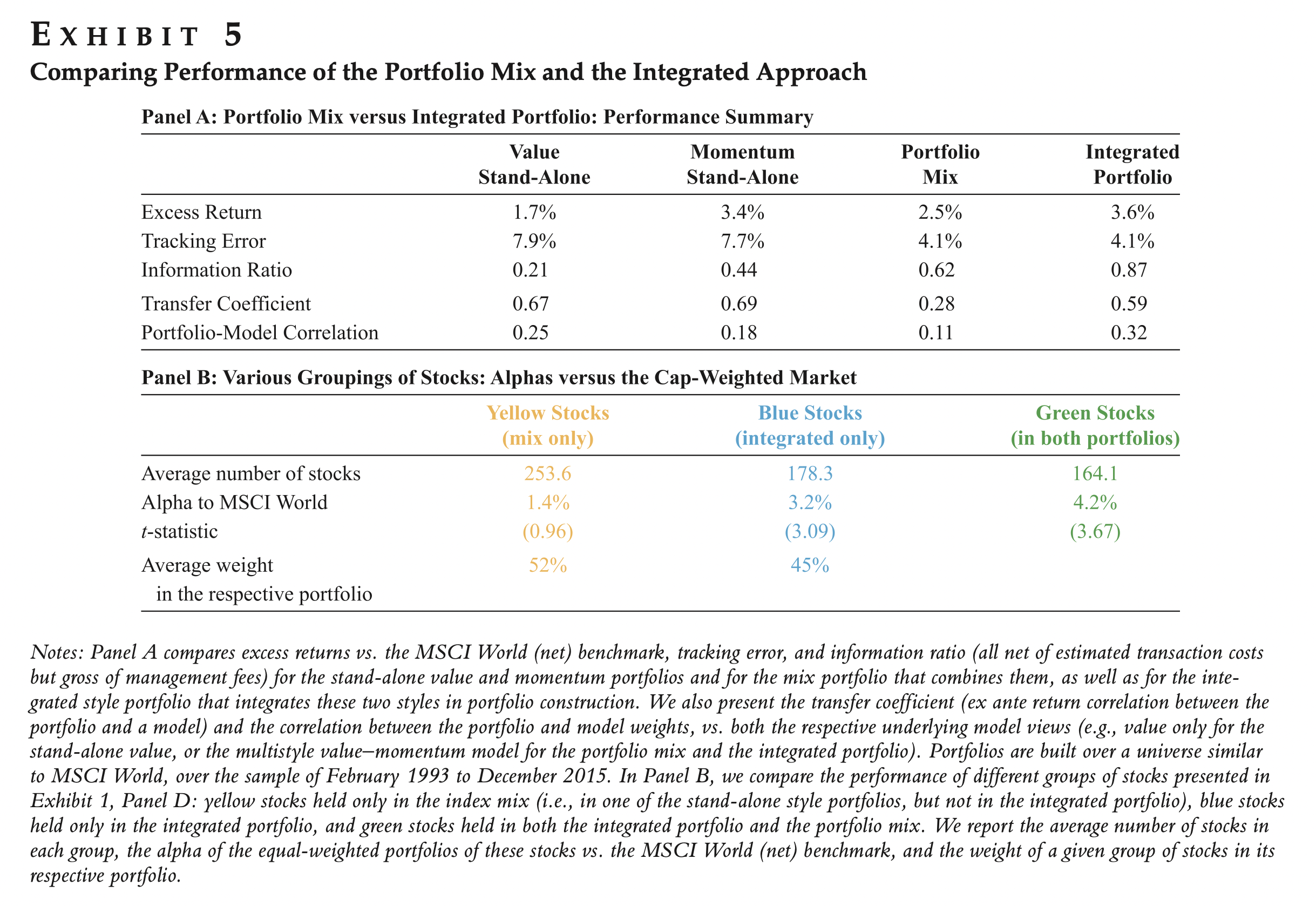

The AQR paper Long-Only Style Investing: Don’t Just Mix, Integrate finds that, when constrained by tracking error, integrated portfolios outperformed mixed ones.

In the following chart, you can see that the mixed (or silo) portfolio adds 1.4% of alpha to the MSCI World index. Not bad. However, that is a only a fraction of the 3.2% added by the integrated approach, and the 4.2% of stocks held in both.

In conclusion: given tracking error mandates, it seems that integrating may be the better option.

But hold on…

That outperformance comes with a catch: those mixed portfolios had to include way more stocks to meet the tracking error constraint.

What If You Unconstrain Stock Count?

Back in 2021, Jack looked at that exact question and ran a “horse race” where the number of stocks held in each approach was kept equal. For example, 100 value + 100 momentum stocks in the mixed portfolio versus 200 integrated picks.

The result? The mixed or silo portfolios came out ahead.

More specifically, the mixed approach performed better the less stocks you held. As you increase the number of holdings, the difference fades. But when you concentrate, owning only the strongest and cheapest stocks can have portfolio-wide benefits.

What About Risk?

You might wonder: are mixed portfolios just taking on more risk?

Surprisingly, the answer is… not really.

Historical Sharpe ratios for both approaches have been similar—noisy and inconclusive across U.S. and international data.

So… Which Approach Should You Use?

The answer depends on your goals and preferences.

The integrated approach makes sense for investors running long-short portfolios, where avoiding contradictory positions is crucial. It also suits those seeking exposure to multiple (or most) investment factors—such as value, momentum, size, quality, and low volatility—and regard all factors with equal or similar importance.

Another key advantage of integrated portfolios is that they tend to turn over more slowly. Because you’re not managing two separate sleeves, you avoid cases where one portfolio is buying a stock while the other is selling it—racking up trading costs with no net gain.

The mixed approach, on the other hand, may be better for investors who are less concerned about tracking error and more focused on maximizing expected returns. It also allows for cleaner attribution of returns and provides more behavioral clarity, making it a great strategy for those wishing to understand what’s driving portfolio performance.

Lastly, it’s also worth noting that not all factors behave the same. Value and momentum are particularly well-suited to the mixed approach because they benefit most from concentration. Other factors—such as size and low volatility—are generally not suited for concentrated portfolios. If these are factors you’re aiming to target, an integrated approach (or even a simple screening filter) may be the more appropriate route.

Sources: Fitzgibbons, Shaun, Jacques Friedman, Lukasz Pomorski, and Laura Serban. “Long-Only Style Investing: Don’t Just Mix, Integrate.” The Journal of Investing 26, no. 4 (November 27, 2017): 153–64.2017.26.4.153. https://www.aqr.com/Insights/Research/White-Papers/Long-Only-Style-Investing

Vogel, Jack. “Value and Momentum Investing: Combine or Separate?” Alpha Architect (May 25, 2021). https://alphaarchitect.com/the-best-way-to-combine-value-and-momentum-investing-strategies/

About the Author: Jose Ordonez

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.