Thematic investing has exploded in popularity, with ETFs and products built around buzzwords like “AI,” “clean energy,” and “digital health.” But do these themes actually represent unique sources of risk and return, or are they just clever marketing? In their paper Thematic Investing: A Risk-Based Perspective, Candès, Hastie, Hogan, Kahn, Luo, and Spector develop a novel framework to measure whether thematic baskets capture real, coherent risks that matter for investors. Their findings challenge conventional risk models and highlight both the dangers and opportunities of betting on investment “themes.”

Thematic Investing: A Risk-based Perspective

- Candès, Hastie, Hogan, Kahn, Luo & Spector

- Financial Analyst Journal, 2025

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

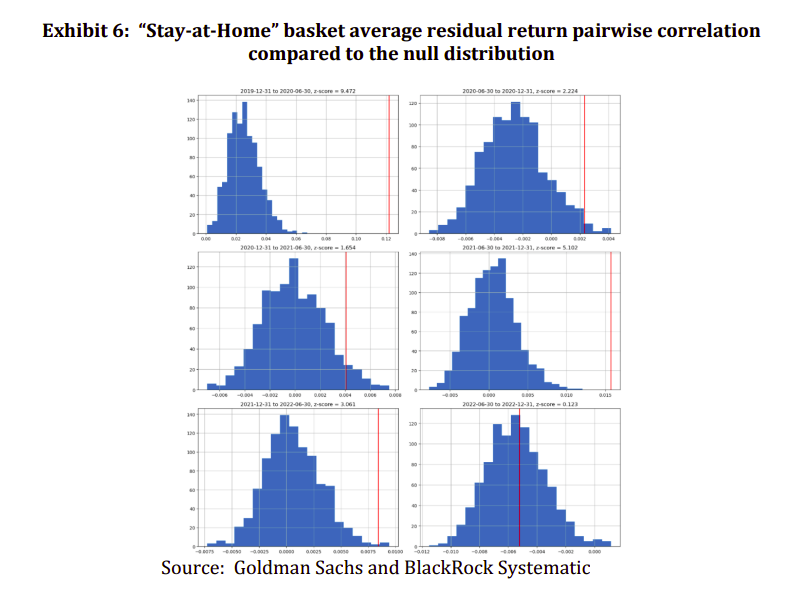

Many marketed thematic baskets (e.g. “AI,” “Clean Energy,” “Digital Health”) display statistically significant residual co-correlations beyond what standard factor models capture – i.e., transient but coherent risk themes

These coherent themes imply risk underestimation: ignoring them means portfolios may have twice the realized risk compared to model forecasts. Importantly, themes with detectable coherence also tend to show return persistence (trend behavior), offering potential opportunities for timing or tilting exposures. However, not all themes pass the coherence test – only a subset of baskets exhibit meaningful, measurable common shocks.

Practical Applications for Investment Advisors

Test theme coherence before buying: ask for historical residual correlation statistics. If the theme is “incoherent,” treat it like marketing, not strategy.

Adjust risk models: incorporate theme residual correlation estimates into risk forecasts to avoid underestimating portfolio volatility.

Tilt capital dynamically : overweight themes that show coherence and trending behavior; underweight or avoid weak ones.

Exercise caution with expensive thematic products : fees plus return drag eat into the limited persistence that these themes offer.

How to Explain This to Clients

“When a theme is truly ‘real,’ its underlying stocks move together more than random chance would suggest — even after you strip out standard factors. That extra co-movement is a hidden risk, but also a hidden opportunity. We can measure which themes behave coherently and selectively tilt toward those, while avoiding noisy marketing themes that lack any statistical backbone.”

The Most Important Chart from the Paper

Figure 6: These graphs show a scatterplot of thematic baskets. Those in the upper-right corner (high correlation + high persistence) are the rare themes worth paying attention to. Most others cluster near the origin — suggesting they’re little more than marketing wrappers.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Thematic investing has grown in popularity even without a clear definition. We propose a risk-based definition of a theme and focus on themes that involve significant transient correlations of residual returns. We present a bootstrapping style approach to determine the statistical significance of the average pairwise correlation among stocks in a thematic basket. Analyzing thematic baskets provided by an investment bank, we find evidence of statistically significant correlations. The thematic baskets with statistically significant average pairwise correlation will have risk levels above predictions. Furthermore, they exhibit statistically significant trending. Baskets with insignificant average pairwise correlation do not trend on average.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.