“How much income can I reliably draw from my retirement savings?” For most households with IRAs/401(k)s (and without defined-benefit pensions), the answer is maddeningly uncertain—because both markets and lifespans are uncertain. Inflation-indexed life annuities would solve much of this, but they’re rarely available. This research offers a practical framework that gets close: pair a simple stock portfolio with a ladder of inflation-indexed bonds (TIPS) and spend using an annually recalculated “virtual annuity.” The result aims to avoid both rocks: the risk of outliving assets and the chronic underspending that many “safe” rules produce.

The Only Other Spending Rule Article You Will Ever Need

- Stefan Sharkansky

- Financial Analyst Journal, 2025

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

ARVA: a simple, actionable framework

Construct the portfolio with two building blocks: (1) a TIPS ladder held to maturity to deliver a real, predictable income stream; (2) a risky bucket invested in a low-fee broad U.S. equity index fund. Withdrawals from the risky bucket follow an amortization formula (annually recalculated), while the TIPS ladder sets the income floor.

Why ARVA dominates fixed-rate rules

Fixed-rate rules (e.g., 4% with guardrails) either risk depletion or, more often, force households to live below their means and die with outsized legacies. ARVA’s math respects the budget constraint and adjusts withdrawals to market reality—so assets are scheduled to be depleted at the chosen horizon, not prematurely.

Stocks for the risky bucket; bonds belong in the ladder

Historically, a 100% equity risky bucket amortized at the long-run real geometric mean (~6.9%) produced higher lifetime withdrawals than blended stock/bond funds with similar downside in the lower quantiles. If you want bond exposure for income stability, hold TIPS to maturity in the ladder—not volatile bond funds.

The TIPS ladder is the right volatility dampener

Because TIPS cashflows are real and known when held to maturity, the ladder sets a clear floor. Income variance of the total plan scales linearly with the stock fraction; adding more ladder lowers the dispersion and raises the worst-case withdrawal—without the correlation problems of bond funds.

Practical Applications for Investment Advisors

Start with the floor

Quantify the client’s essential “must-have” real income. Size the TIPS ladder to meet that floor with the desired confidence, given today’s real yields and the intended horizon (commonly 30 years; extend via ladder extensions if needed).

Calibrate the risky bucket to the client

Use the amortization formula with the equity bucket. Aim at the long-run real equity return (or your forward estimate) for the discount rate. Show clients the historical distribution of average and worst-year withdrawals for different stock weights.

Replace bond funds with the ladder

If the planning goal is stable, real cashflows, TIPS held to maturity are superior to bond funds, which add volatility and equity correlation. Let stocks carry the growth; let TIPS provide stability.

Explain variability honestly—then manage it

Withdrawals will vary. Frame variable equity withdrawals as “bonus” income above a secure floor. Increase ladder size to reduce variance, not guardrail constraints that can still force painful cuts.

Document the trade-offs

ARVA eliminates “probability of ruin” for the chosen horizon but replaces it with variable withdrawals. Fixed-rate rules reduce variance but almost guarantee underspending and large unintended legacies. Make the choice explicit.

How to Explain This to Clients

“Think of your retirement income in two parts. First, we build a secure, inflation-proof paycheck using a ladder of TIPS—your essentials. Second, we add a stock bucket that pays you like a recalculated annuity each year. That part will bounce with markets, but over history it raised total lifetime income versus common ‘safe’ rules, without raising the worst-case years. If you want fewer ups and downs, we simply put more into the TIPS paycheck and less into the stock bucket.”

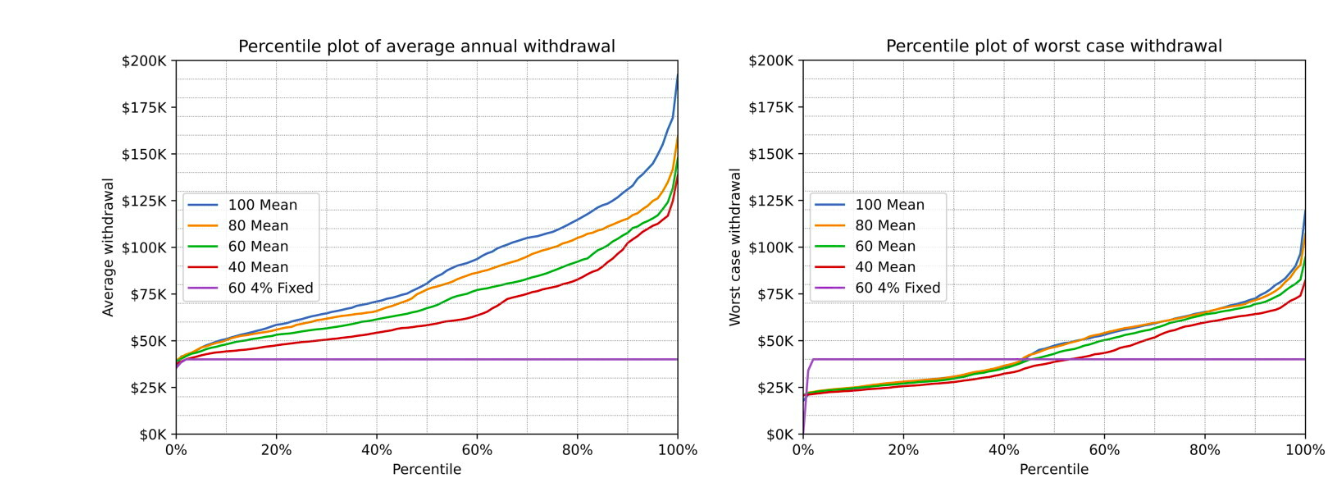

The Most Important Chart from the Paper

Figure 1: Percentile Plots for Average and Worst-Case Withdrawal Rates, Assuming a $1 Million Initial Portfolio

A percentile plot comparing (a) average annual withdrawals and (b) worst single-year withdrawals over 30-year histories. The visual shows:

- All-stock risky buckets under ARVA delivered higher median and upper-quantile incomes than mixed stock/bond risky buckets, with similar lower-tail outcomes.

- ARVA with a meaningful TIPS ladder reduces worst-case withdrawals relative to guardrails at comparable stock exposure, while maintaining higher average income.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

This work describes an actionable framework for constructing and drawing income from a portfolio of retirement assets. A sufficient portfolio consists solely of a ladder of inflation-indexed bonds, such as U.S. Treasury Inflation-Protected Securities (TIPS), and a stock market index fund. We consider longevity risk and time-varying spending patterns and show how to amortize decumulation of the stock asset to provide variable income without risking premature portfolio depletion. We explain theoretically and demonstrate empirically how this strategy is less risky and more effective at maximizing lifetime retirement income than are methods commonly used by financial advisors.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.