A new working paper from Gennaili, Ma, and the one-the-only Andrei Shleifer.

Expectations and Investment

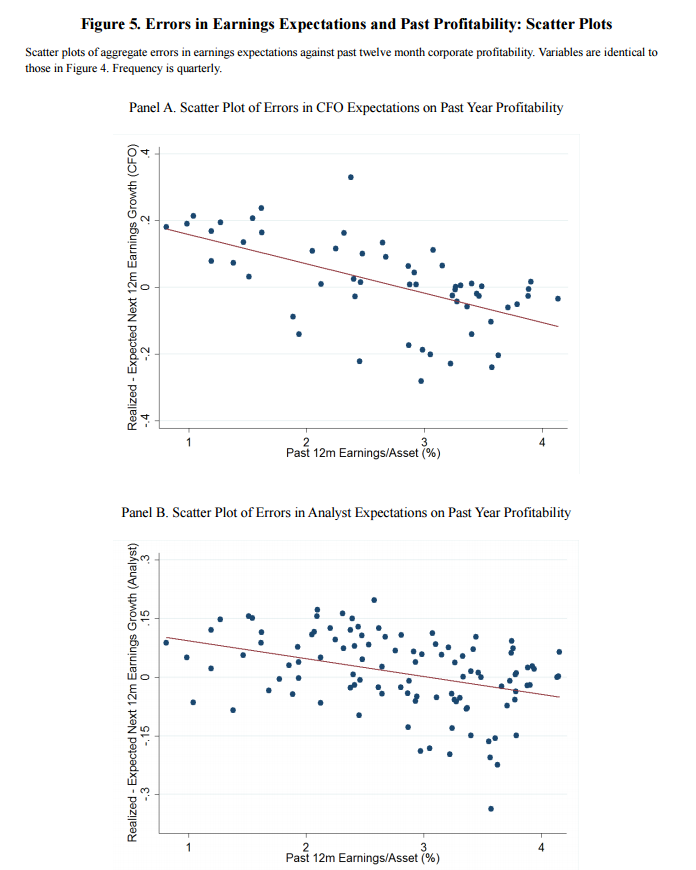

Using micro data from Duke University quarterly survey of Chief Financial Officers, we show that corporate investment plans as well as actual investment are well explained by CFOs’ expectations of earnings growth. The information in expectations data is not subsumed by traditional variables, such as Tobin’s Q or discount rates. We also show that errors in CFO expectations of earnings growth are predictable from past earnings and other data, pointing to extrapolative structure of expectations and suggesting that expectations may not be rational. This evidence, like earlier findings in finance, points to the usefulness of data on actual expectations for understanding economic behavior.

The authors find that “high past year profitability is correlated with over-optimism, while low past year profitability is correlated with over-pessimism.”

In other words, to win in a market, one must identify how the market forms expectations, identify how that expectation is systematically flawed, and then exploit it to your advantage.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.