Unlike equity and bond investing, investing in commodities is a less familiar undertaking for many. Commodities behave differently than stocks and bonds, pose different risks, and can be taxed differently. And let’s be blunt: few retail and/or professional investors understand how to use commodity futures.

To address our own blind spots in the marketplace, we’ve spent the past few years investigating academic research and examining trading systems and strategies in the commodity futures space. At this stage I’d say our knowledge is fairly extensive, but we’re still learning and trying to get better. After acknowledging our own educational blind spots with respect to commodity futures, and subsequently studying and learning about the different ways they can be traded, used for hedging, and integrated into portfolios, we’re always curious to see how other “professionals” think about these contracts. Based our review of the product landscape and numerous discussions among “professional” asset allocators, the results don’t look promising.

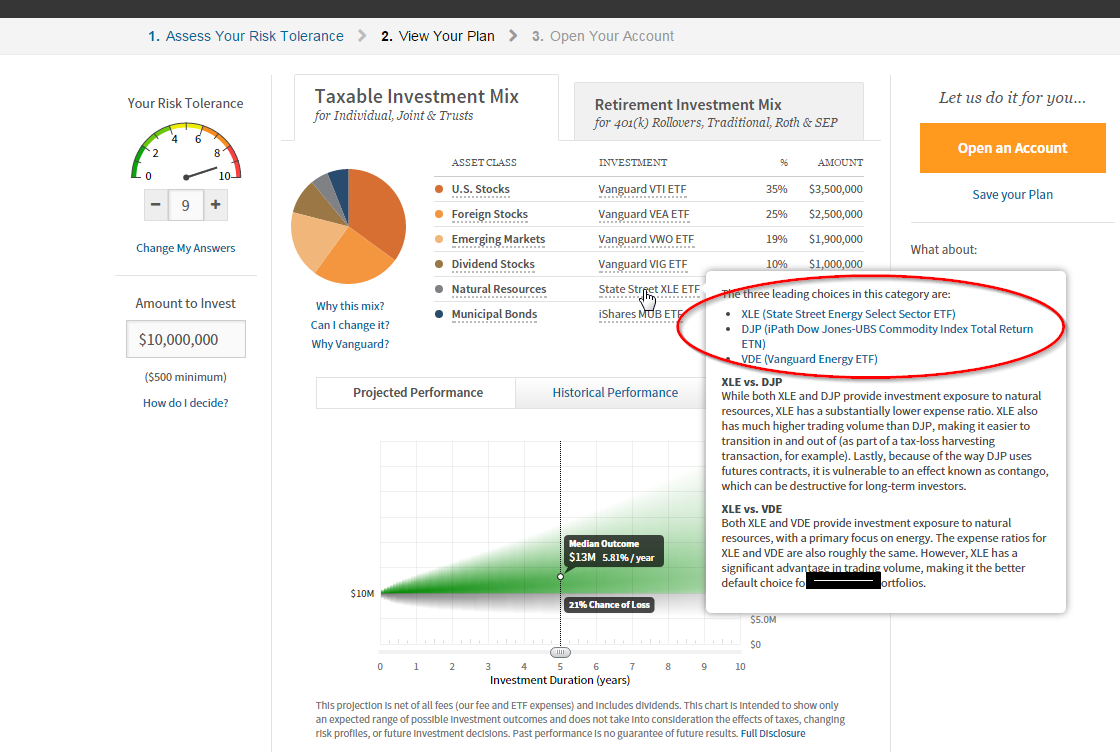

For example, consider the discussion below from a popular robo-advisor’s website. The site compares equity-based ETFs, XLE and VDE, which buy the stock of commodity-related firms (e.g., Exxon or Chevron) to DJP, a futures-based ETN, which buys baskets of commodity futures based on the commodity’s “liquidity and economic significance.” Odd, to say the least.

First, the underlying assumption in the robo-advisor’s discussion is that these securities are somehow the same, which is implicit in their reference to tax-loss harvesting, which bounces investors across the 3 options so they can book losses, but maintain the same “exposure.” But the problem is that these exposures are not the same. The chart below highlights this fact without the use of numbers or equations or basic knowledge of commodity futures.

Oddly enough, the robo advisor highlights that XLE and VDE are “better” because they are “cheaper.” But how can one describe “cheapness” when one is comparing apples to oranges? Next, the commodity index chosen (DJP) doesn’t even consider the factors that matter in commodity investing (e.g., term structure and momentum). DJP is a classic case of products chasing performance.

To be clear, this isn’t a bash session on robo-advisors–we think robos are doing some great things in the business–to include better transparency, which is why we were able to actually get the chart above (most advisors/sites keep it “proprietary”). Nonetheless, the discussion is indicative of financial advisor knowledge of commodity futures.

So let’s try and get smart about commodity futures

First, a recap of what matters in commodity futures trading:

And here are some great papers on the subject by Erb/Harvey:

- Common misconceptions on Commodity Futures Investing

- The Tactical and Strategic Value of Commodity Futures

The lessons from Erb/Harvey are as follows:

- Commodity futures are NOT a play on commodity spot prices.

- Commodity futures should NOT be considered an asset class, but a trading strategy.

- Commodity futures do NOT deliver equity-like performance.

And here is the biggest common misconception we see (highlighted above):

Investing in commodity futures is not the same as investing in equities tied to commodities

For example, owning oil futures is not the same as owning Exxon stock.

If you don’t believe us, check out the lengthy post on this subject that we wrote recently.

What’s the bottomline?

Any good advisor should know how and why they invest a client’s wealth. A good advisor will certainly make bad calls and lose money at times, but the onus is on the advisor to make informed decisions.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.