The Best of Strategies for the Worst of Times: Can Portfolios Be Crisis Proofed?

- Campbell R. Harvey, Edward Hoyle, Sandy Rattray, Matthew Sargaison, Dan Taylor, and Otto Van Hemert

- The Journal of Portfolio Management

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

This is part 2 (part one is here) of an excellent article that examines the feasibility and effectiveness of protecting equity portfolios using traditional passive means and more contemporary active strategies. It is jam-packed with information and analysis that is best consumed in two parts; however, a good summary of the article by Larry Swedroe can be found here. The focus in part 1 is the usefulness of traditional passive approaches. Part 2 gets after more complex and contemporary strategies. A deeper dive into the full article will not disappoint. (As a side note, Cam Harvey was just on the Meb Faber podcast — check it out if you have a few moments.)

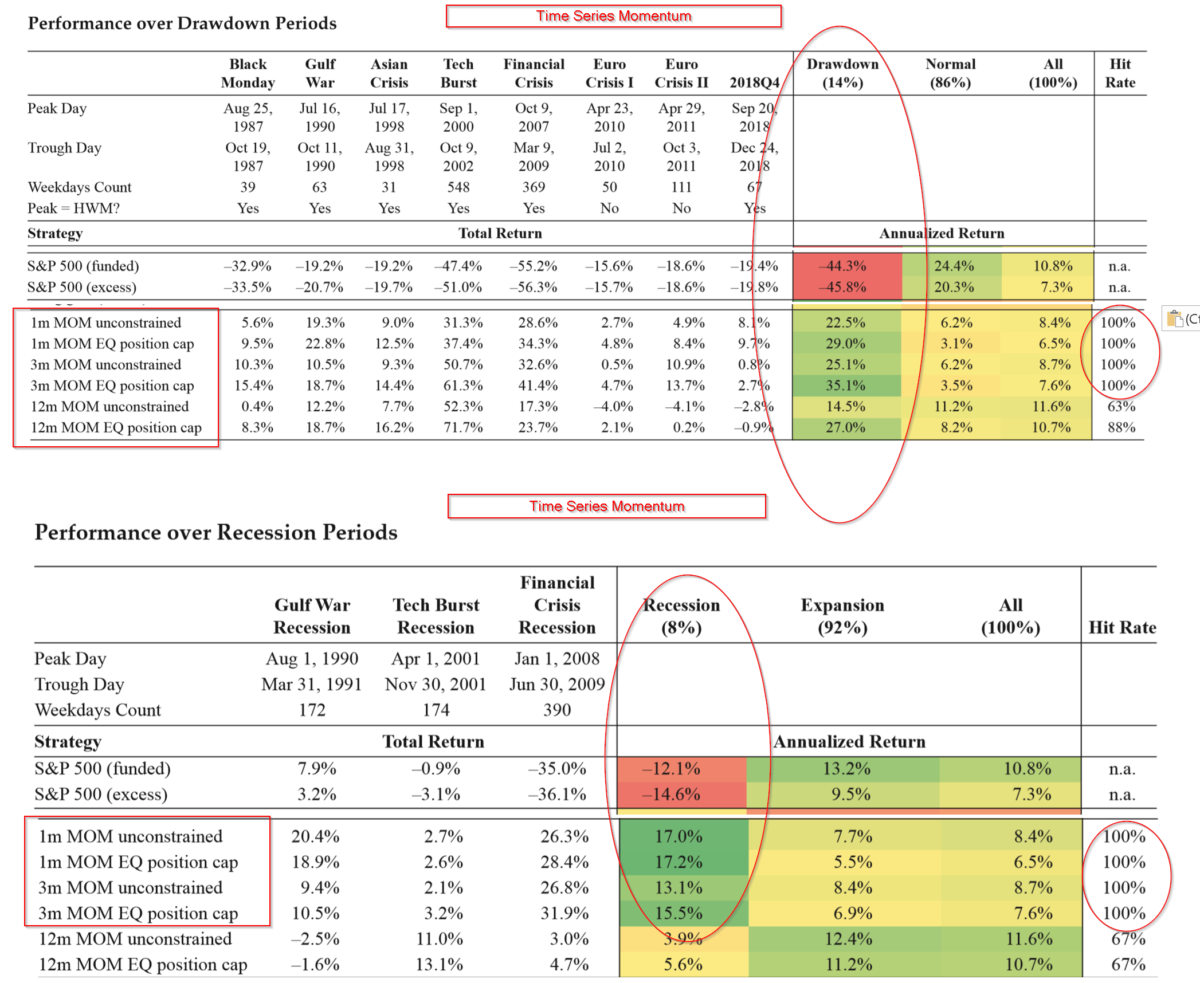

During the sample period of 1985 – 2018, 3 recessions and 8 (of the worst) equity drawdowns were identified for the US. Two active strategies employing times series momentum signals using futures contracts across all markets; and long/short positions on individual stocks using various factor signals are evaluated on the basis of performance during the recessionary and drawdown periods.

- Can long-only equity portfolios be completely shielded from crises (drawdowns and recessions) implementing times series momentum with futures?

- Can long-only equity portfolios be completely shielded from crises (drawdowns and recessions) by implementing long/short strategies with individual stocks and factors?

- How do the strategies from part 1 and part 2 compare for each type of crisis? Which is best? Which is worse?

What are the Academic Insights?

- YES. Using times series momentum of 1,3 and 12 months in duration to signal positions in futures across commodities, currencies, equities, bonds and interest rate markets, two hedges were considered: unconstrained equity and equity constrained to zero percent. However, both were constrained to achieve similar volatility at 10%. Transaction and costs of slippage for the 3-month signal were estimated at 0.6% to 0.8% annually. In the first chart below, note that the hit rate was 100% for drawdowns for the 1 and 3-month momentum signals for constrained and unconstrained weightings. The hit rate dropped quite a bit for the 12-month signal. One drawback: the hedges did produce asymmetrical returns relative to the market during the drawdowns. Results for recessionary periods are shown in the second chart. The hit rate was also 100% for the 1 and 3-month signals, but dropped to 67% for the 12-month signal. Returns during these periods were roughly symmetrical with the size of market decline.

- YES. Long/short portfolios were constructed using factors including: size, value, profitability, investment, cross-sectional momentum, quality and low volatility. Of the seven factors, only profitability and quality exhibited a hit rate of 100% and symmetrical returns for drawdowns and recessions. Apparently the “flight to quality” is an accurate explanation, just not in the usual context of gold and bonds. The correlation between quality and the market was -.48 and -.27 for profitability for both types of crisis periods. Interestingly, value, investment, CS momentum, and low volatility as strategies actually turned in negative returns during recessions. For CS momentum and low vol, returns were in league with the size of the market decline itself.

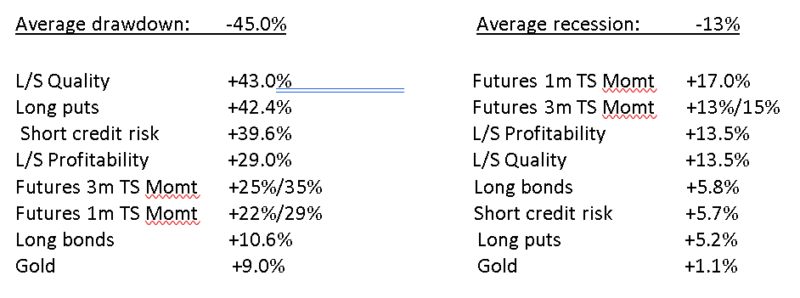

- Considering only those strategies with 100% hit rates and relative hedging effectiveness for drawdowns: L/S quality and long puts were the clearest and most convincing winners, with short credit risk a close runner-up. Moderately effective strategies were 1 and 3 month times series momentum via futures and L/S profitability were moderately effective in terms of returns. Long bonds and gold were abysmal relative to the other strategies. A somewhat different pattern emerged for recessionary periods, where the strategies separated into two distinct groups. Strategies that worked to effectively crisis-proof long-only equity portfolios included (in order): L/S Quality, 1-month times momentum, 3-month times series momentum, and L/S profitability. Less effective, where the hedging was only half of that necessary to offset a market decline of approximately 13%, included with not much distinction: long puts, short credit risk and long bonds. Surprisingly, the absolute worst was gold, especially during recessions. The average annual return was only 1.1% as protection for an average market decline of 13%. Not much of a safe haven, is it?

Why does it matter?

A great contribution by standardizing the performance of typical hedges during crisis periods. It gives substance to the effectiveness of generally held ideas about “flights to quality” (stick with stocks) and “safe havens” (not much there). Ignoring all costs, here’s my take on the relative ranking on average returns from each hedge.

The most important chart from the paper

Abstract

In the late stages of long bull markets, a popular question arises: What steps can an investor take to mitigate the impact of the inevitable large equity correction? Hedging equity portfolios is notoriously difficult and expensive. In this article, the authors analyze the performance of different tools that investors could deploy. For example, continuously holding short-dated S&P 500 put options is the most reliable defensive method but also the most costly strategy. Holding safe-haven US Treasury bonds produces a positive carry but may be an unreliable crisis-hedge strategy because the post-2000 negative bond– equity correlation is a historical rarity. Long gold and long credit protection portfolios sit between puts and bonds in terms of both cost and reliability. Dynamic strategies that performed well during past drawdowns include futures time-series momentum (which benefits from extended equity sell-offs) and a quality strategy that takes long (short) positions in the highest (lowest) quality company stocks (which benefits from a flight-to-quality effect during crises). The authors examine both large equity drawdowns and recessions. They also provide some out-of-sample evidence of the defensive performance of these strategies relative to an earlier, related article.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.