What is Quality?

- Jason Hsu , Vitali Kalesnik , and Engin Kose

- Financial Analysts Journal

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

The authors do a very nice survey on measures of quality found in the academic literature and in commercially available quality indexes. They examine seven quality categories including: profitability, earnings stability, capital structure, growth, accounting quality, payout/dilution and investment. In order to mitigate datamining biases the authors employ 3 criteria (Hsu, Kalesnik and Viswanathan, 2015 ) to establish an initial level of robustness for at least 25 measures plus composites drawn from the 7 categories. See Table 2 from the paper for a detailed list of categories and attributes considered. Once robustness is established, the authors test the resulting attributes as sources of long term returns using criteria suggested by HLZ and McLean and Pontiff (2016). Markets tested included the US, Europe, Asia Pacific ex Japan, Japan, and other Global developed markets.

- Do the various attributes or measures of quality found in academic studies and utilized by commercial index providers proxy for a common factor or common source of covariation?

- Which of the various attributes of quality are robust measures?

- Which of the robust attributes of quality likely represent a source of long term returns as opposed to simply being a byproduct of data mining biases?

What are the Academic Insights?

- NO. A pairwise correlation matrix of all quality measures indicates little to no significant relationships. The lack of correlational evidence indicates that the variables do not proxy for an “unidentified” common quality factor or a single anomaly. The authors suggest that the set of quality measures (as well as quality based commercial indexes) studied are best portrayed as a combination of signals constructed from a company’s financial and accounting characteristics. This result is in sync with the academic literature surveyed. The authors found no academic research where claims of a proxy for common covariation were made.

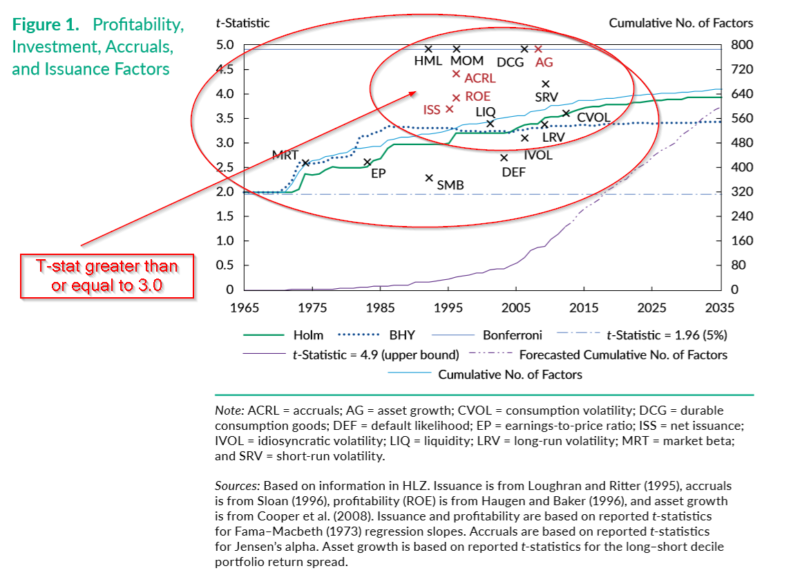

- FOUR, INCLUDING ROE (Profitability), AG (Investment or asset growth), ACRL (Accruals ), and ISS (Issuance factors or net issuance). See chart below for all categories tested with emphasis on the 4 robust measures. Robustness tests included 3 criteria: A measure was considered robust if it had garnered substantial attention in peer-reviewed journals; if statistical significance was immune to variations in time periods and geography; and if immune to legitimate variations in definitions of the measure as well.

- SAME FOUR. The HLZ criteria requires a larger t-stat to mitigate the impact of data mining biases. Three different methods for calculating the t-stat were utilized to determine significance in the context of the data mining biases. The criteria included: BHY, Bonferroni, and Holm methods to calculate the t- stat corresponding to the 5% confidence level necessary given the numerous tests conducted in factor searches. References for the 3 methods are provided in footnote 19 of the paper. All four of the robust factors identified in #2 and shown (marked in red) in the chart below, meet the stringent HLZ criteria. The authors conclude that the long term return performance of those four robust factors is not likely the result of multiple searches. The same could not be said for capital structure, earnings stability, and growth in profitability.

Why does it matter?

A readable and to-the-point analysis of a wide variety of commercial and academic measures of quality conducted across global developed markets. Although popular in a commercial sense, there is no standard definition for a quality factor and those definitions used in the practitioner sphere have received only minimal scrutiny. There are two takeaways: 1. Investors should consider the commercial quality products as an amalgamation of independent attributes that may or may not be a robust source of long term returns; 2. However, the knowledge provided here provides investors with a leg up on determining which blend (that is, index) of quality attributes is likely to produce a reliable outcome.

The most important chart from the paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Unlike standard factors, such as value, momentum, and size, “quality” lacks a commonly accepted definition. Practitioners, however, are increasingly gravitating to this style factor. They define quality to be various signals or combinations of signals—some that have been thoroughly explored in the academic literature and others that have received limited attention. Among a comprehensive group of the quality categories used by practitioners, we find that profitability, accounting quality, payout/ dilution, and investment tend to be associated with a return premium whereas capital structure, earnings stability, and growth in profitability show little evidence of a premium. Profitability and investment related characteristics tend to capture most of the quality return premium.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.