Intraday Arbitrage Between ETFs and their Underlying Portfolios

- Box, Davis, Evans, and Lynch

- Working paper

- A version of this paper can be found here

Editor’s note: Seeing how the results may have shifted since the “ARK phenomenon” would be a great robustness test for this paper.

ETFs are growing at a rapid pace and becoming a significant contributor to intraday activity (and we are only making the problem worse!). Naturally, some will begin to wonder how the ETF innovation impacts trading in the underlying securities that ETFs own. Initially, it was thought that ETF trading would improve price discovery, however, recent academic research has concluded that ETFs may have adverse effects on the market.(1)

The paper under discussion jumps into the debate via a minute-by-minute intraday stock database to identify if ETFs have positive or negative effects on the efficiency of the stock market.

The core research question is the following:

- Do ETFs materially impact their underlying securities in a negative way?

What are the Academic Insights?

- No. ETF flows and demand shocks do not appear to have undue influence on the underlying constituents. But it’s complicated and we recommend you read the paper for more details.

The authors state the following:

No relationship between ETF order flow and returns on the constituent securities at 1-, 5-, and 10-minute intraday intervals, and only a weak relationship at a daily interval.Intraday Arbitrage Between ETFs and Their Underlying Portfolios, Box, Davis, Evans, and Lynch 2019

Their conclusion from a cadre of tests is as follows:

Identifying intraday arbitrage opportunities between ETFs and the constituents, we find little evidence that arbitrage opportunities precede trading in the underlying. Instead, arbitrage opportunities are initiated by shocks to the underlying and subsequently corrected through updates in the best bid and offer quotes. Thus, while we observe quote adjustments in response to price discrepancies, we find limited evidence of arbitrage trading. Additionally, our results indicate that bid-ask spreads remain steady during arbitrage opportunities. Not only are we unable to document arbitrage in the face of mispricing, we also find no evidence that the convergence of prices removes liquidity from the market.Intraday Arbitrage Between ETFs and Their Underlying Portfolios, Box, Davis, Evans, and Lynch 2019

Why does it matter?

ETFs represent the new kids on the block. New kids on the block, especially when they are stealing your lunch money, are bound to attract scrutiny from competitors, academic researchers, and politicians. A primary attack has been the accusation that ETF activity is distorting the market and making price discovery less transparent or adding to the lack of breadth in the market. This paper gives the ETF industry a soapbox to stand on and highlights that the product is not manipulating markets and price discovery in a material way.

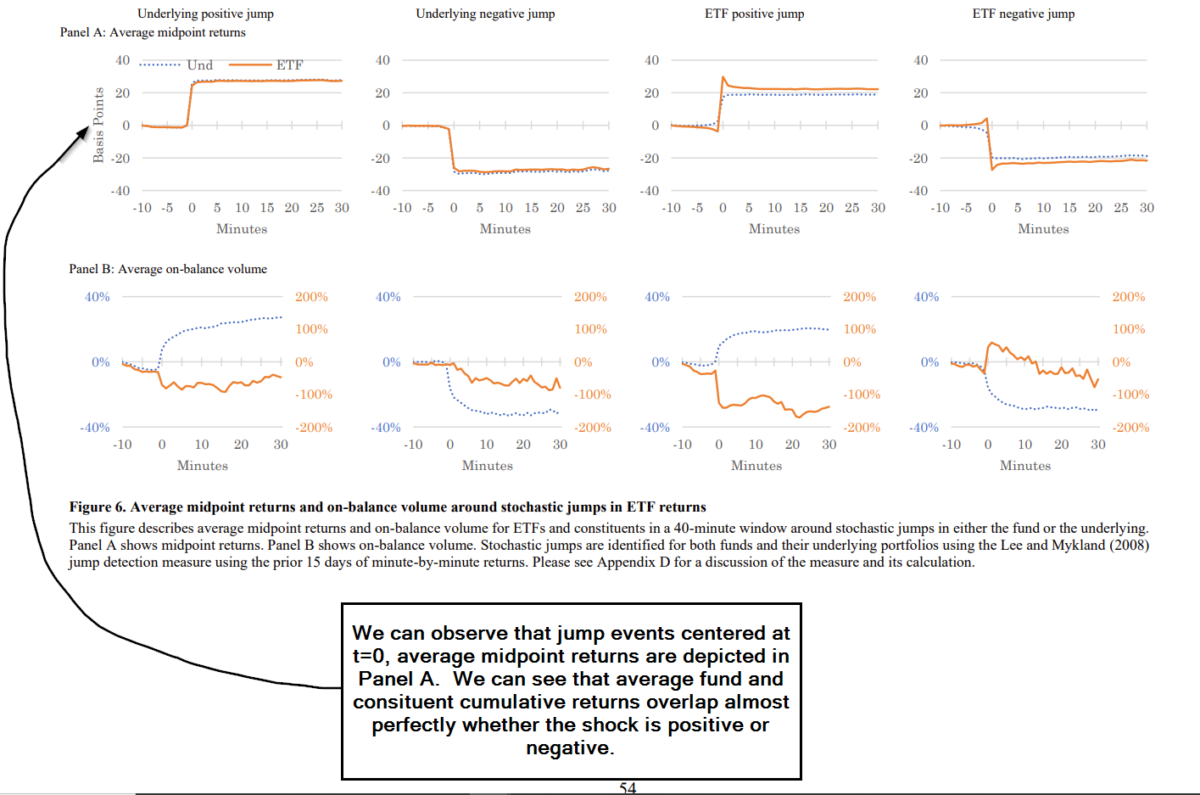

The most important charts from the paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Prior research suggests that ETF arbitrage affects the market quality of underlying securities. We directly test this proposition by examining minute-by-minute returns and order imbalances, but find little evidence that trading in ETFs impacts the underlying. Panel vector autoregression shows ETF returns largely follow the underlying returns. We also find that mispricing events are preceded by underlying price and order imbalance shocks, corrected by ETF quote adjustments unrelated to order imbalance, inconsistent with an arbitrage explanation. Extending our analysis to a daily frequency also reveals little to no relation between ETFs and the market quality of their constituent securities.

References[+]

| ↑1 | For investors that don’t work directly with ETF’s, exactly how ETF’s function and trade aren’t as straightforward as appears on the surface. Due to the somewhat complicated process of ETF activity in the secondary market, we wrote a white paper on Understanding How ETF’s Trade in the Secondary Market. That post will set a solid baseline of understanding for you to fully appreciate this paper. You can also check out our piece on how to start an ETF, which will give the reader insights into the ecosystem and moving parts associated with ETFs. |

|---|

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.