Christoph Reschenhofer contributes to the factor-based investment literature with his April 2022 paper, “Combining Factors,” in which he investigated the performance of multifactor portfolios formed via a combination of stock characteristics scores. He began by noting that while “the finance literature has made substantial progress in identifying factors that drive stocks’ risk and return characteristics … when it comes to implementing characteristics-based portfolio strategies, the academic literature offers little guidance. For example, what are the tradeoffs when defining the cutoff on a characteristic for a stock to be included in the portfolio? At which threshold should it be sold and replaced? Should several characteristics be combined for an aggregate score for each stock? If yes, how does this affect portfolio risk and return? Should different characteristics obtain equal weight when calculating an aggregate score?”

Reschenhofer’s analysis included the factors commonly used in asset pricing models: market beta; size (market capitalization); value (book-to-market ratio of equity); investment (change in total assets); profitability (revenues minus cost of goods sold, interest expense and selling, general and administrative expenses divided by the sum of book equity and minority interest); and momentum (total return from month t – 12 to month t – 2). In his main analysis, he defined a stock j score as the percentage of the market capitalization of all stocks in the universe with a characteristic value lower or equal to stock j divided by the total market capitalization of the stock universe. In the base case, the initial long-only (the way most individuals invest) portfolio consisted of all stocks with a score greater than or equal to 90, value-weighted. At the end of each month, the portfolio was rebalanced by selling the stocks with scores below 70 and purchasing those with scores above 90 that were not yet in the portfolio. His database covered all ordinary common shares traded on NYSE, AMEX, and Nasdaq during the period July 1967-June 2020.

Following is a summary of his findings:

- Equity portfolios formed based on scores on each individual characteristic exhibited positive risk premia, even after controlling for the market factor, and they exhibited above-market Sharpe ratios.

- Small firms differ cross-sectionally much more in their characteristics than large firms. For example, for small firms the difference between the book-to-market ratio of the top quintile versus the bottom quintile was approximately 1.6 when quintiles were defined by the number of firms; for large firms the difference was approximately 1.

- Factor premiums were all greater in small stocks than in large stocks.

- When comparing single characteristic portfolios with multivariate characteristic portfolios (where the aggregate score was calculated as the equally-weighted average of the individual scores), averaging multiple firm characteristic scores produced portfolios with more favorable risk-return characteristics (lower volatility and higher after-cost returns) than the market and those of portfolios sorted on univariate characteristics. The small-cap (large-cap) portfolio exhibited a 70 percent (25 percent) increase in Sharpe ratio after transactions cost compared to the market portfolio.

- The return, risk, and turnover preferences of portfolios formed on multiple characteristics were very sensitive to buy and sell thresholds, leading to dramatic changes in turnover. The sell-side thresholds mattered much more.

- While ignoring transaction costs, the highest Sharpe ratio was achieved by buying at a score of 92 and selling at 91. Considering realistic transaction costs, the optimal thresholds changed substantially to a buy threshold of 92 and a sell threshold of 72.

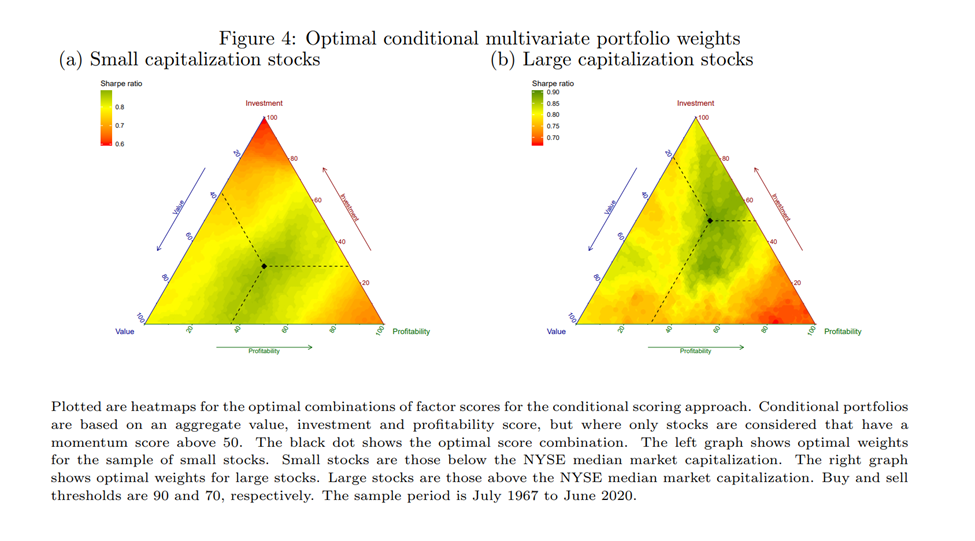

- A large proportion of the resulting portfolio turnover was due to the volatile momentum characteristic. To address this, the author analyzed portfolios based on only including stocks with an above-median momentum score (a conditional scoring approach) and found that it led to significantly lower portfolio turnover and more attractive Sharpe ratios, especially when considering transaction costs.

- Results were consistent for a wide range of robustness checks, including all subperiods over five decades and a European data set.

While Reschenhofer did identify optimal weights for individual factor characteristics (for small stocks the optimal weights were 36 percent value, 11 percent profitability, 28 percent momentum, and 5 percent investment; and for large stocks the optimal weights were 20 percent value, 47 percent investment, 31 percent profitability, and 2 percent momentum), his findings led him to conclude that a naive 1/N factor portfolio is a tough benchmark (the benefits of deviating from the simple equal weighting were moderate). He added: “Especially out-of-sample, portfolios based on equal weights on each characteristic are very difficult to beat.”

Investor Takeaways

Reschenhofer’s findings demonstrate the important role that portfolio construction rules (such as creating efficient buy and hold ranges or imposing screens that exclude stocks with negative momentum) play in determining not only the risk and expected return of a portfolio but how efficiently the strategy can be implemented (considering the impact of turnover and trading costs)—wide (narrow) thresholds reduce (increase) portfolio turnover and transactions costs, thereby increasing after-cost returns and Sharpe ratios. His findings also provide support for multiple characteristics-based scorings to form long-only factor portfolios, encouraging the combination of slow-moving characteristics (such as value, investment and/or profitability) conditional on fast-moving characteristics (such as momentum), to reduce portfolio turnover and transactions cost. Fund families such as Alpha Architect, AQR, Avantis, Bridgeway and Dimensional use such an approach, integrating multiple characteristics into their portfolios conditional on momentum signals.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data which may become outdated or otherwise superseded without notice. Third party data is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. Total return includes reinvestment of dividends and capital gains. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Buckingham Strategic Wealth® and Buckingham Strategic Partners® are not affiliated with AQR, Avantis, Bridgeway or Dimensional. Mentions of these specific fund families are not recommendations of their funds but only for informational and educational purposes only. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. LSR-22-284

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.