This paper reveals a striking pattern in U.S. mortgage markets: minority borrowers are more likely to complete applications, be approved, and avoid default when they interact with minority loan officers. Using detailed data linking millions of mortgage applications to individual loan officers, the authors show that even in a highly automated lending industry, racial alignment between borrower and lender leads to better outcomes. The effect is not driven by looser standards or higher risk-taking, but rather by better information gathering and borrower support. These findings suggest that workforce diversity in financial intermediation can meaningfully reduce racial gaps in credit access.

The Impact of Minority Representation at Mortgage Lenders

- Frame, Huang, Mayer, and Sunderam

- The Journal of Finance, 2025

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

Minority Loan Officers Increase Mortgage Origination Rates

When minority borrowers are paired with minority loan officers, application completion, approval, and origination rates all rise. For example, origination gaps between white and minority applicants fall by over 50% in same-race pairings.

Better Outcomes with Lower Default Risk

These improved origination outcomes do not come with higher risk. In fact, default rates decrease when minority borrowers are assisted by minority officers, implying better borrower-lender matching and soft information—not looser standards.

Representation Is Especially Lacking Where It’s Most Needed

Minorities are underrepresented in the loan officer workforce—just 15%, versus 39% in the general labor force. Worse, this gap is largest in areas with high minority populations, where the benefits of representation could be greatest.

Human Interaction Still Matters in the Age of FinTech

Despite the increasing automation of mortgage underwriting, the study finds that human discretion and support still drive outcomes—especially in small banks and for complex borrowers. Minority loan officers appear more effective at helping same-race applicants navigate paperwork and requirements.

Practical Applications for Investment Advisors

Understand the Role of Representation in Financial Services

Diversity isn’t just a human resources metric—it affects client outcomes. For firms serving diverse populations, matching clients with representative advisors or support staff may yield tangible performance and satisfaction gains.

Rethink Lending and Real Estate Partnerships

Advisors working with clients on mortgages should be aware of potential barriers in origination tied to representation gaps. Where possible, connect clients—especially minority clients—with brokers or loan officers who understand their backgrounds and challenges.

Consider Advocacy and Community Investment

Financial professionals and firms may want to support initiatives that recruit and retain minority professionals in mortgage lending, wealth management, and related fields. The impact on community financial health could be meaningful and measurable.

How to Explain This to Clients

“You may think mortgage decisions come down to credit scores and paperwork—but it turns out who helps you through the process matters. This research shows that when minority borrowers work with someone who shares their background, they get better results—more approvals, fewer defaults. Representation matters.”

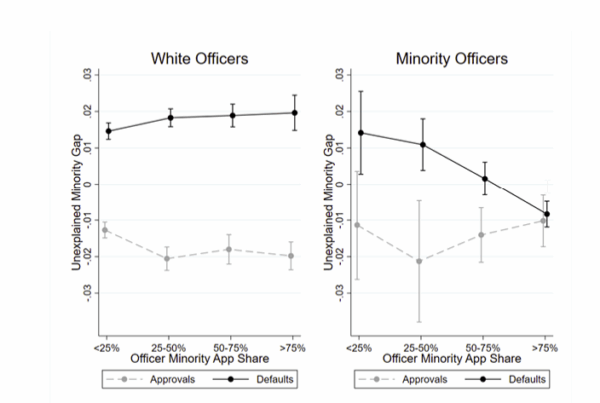

The Most Important Chart from the Paper

Figure 4: Loan Officer Race and Minority Gaps – Specialization

This figure plots unexplained minority gaps in mortgage approvals and defaults against the handling loan officer’s minority application share. The unexplained minority gap estimates come from OLS regressions with the full set of controls in Table 8, where the minority borrower indicator is interacted with indicators for each combination of white/minority officer and the group the officer falls into in terms of minority application share. The left panel shows the estimated minority gaps for white officers (with 95% confidence intervals), and the right panel shows the results for minority officers. The samples match those in Table 8. For approvals, the sample is all completed FHA home purchase mortgage applications in the HMDA database in 2018 and 2019. For defaults, the sample is all FHA home purchase mortgages originated from 2012 to 2018. Both samples implement the standard data filters described in Section 2.5.

Abstract

We study links between the labor market for loan officers and access to mortgage credit. Using novel data matching mortgage applications to loan officers, we find that minorities are underrepresented among loan officers. Minority borrowers are less likely to complete mortgage applications, have completed applications approved, and to ultimately take up a loan. These disparities are reduced when minority borrowers work with minority loan officers. These pairings also lead to lower default rates, suggesting minority loan officers have an informational advantage with minority borrowers. Our results suggest minority underrepresentation among loan officers reduces minority borrowers’ access to credit.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.