Forecast bias is often treated as an abstract behavioral trait. Investors observe data, form expectations, and make decisions. But in reality, these biases shape real trades. Some investors extrapolate from recent performance. Others react in the opposite direction, and these differences affect which stocks they buy, which stocks they sell, and how they move money into equities. This paper introduces a new perspective. Forecast bias is not just about stated beliefs. It shows up directly in individual stock selection.

Extrapolators and contrarians: Forecast bias and individual investor stock trading

- Steffen Andersen , Stephen G. Dimmock , Kasper Meisner Nielsen , Kim Peijnenburg

- Journal of Financial Economics, 2026

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

Forecast bias affects real stock trades

The paper links a laboratory measure of forecast bias to actual administrative trading records. This allows the authors to move beyond surveys and show that biased expectation formation affects real-world stock selection. Investors do not just report different beliefs. They act on them.

Extrapolators buy recent winners

Investors with stronger extrapolation bias tend to buy stocks with higher past returns. A one-standard-deviation increase in forecast bias is associated with buying stocks whose past one-year return is about three percentage points higher. This supports the idea that extrapolators chase recent performance.

Contrarians buy relatively weaker performers

Investors with negative forecast bias behave differently. They are more likely to buy stocks with lower past returns relative to extrapolators. This shows that the same return history can lead different investors to make opposite choices depending on how they process information.

Sales depend more on capital gains than past returns

For selling decisions, the key performance measure is not the stock’s past one-year return. It is the investor’s own capital gain. Extrapolators are less likely to sell stocks with high capital gains, suggesting that personally experienced gains are especially salient when deciding what to sell.

Forecast bias also affects flows into stocks

The paper finds that investors with higher forecast bias increase stock allocations after strong market returns. However, forecast bias does not strongly predict when investors trade. It matters more for what they do once they are already trading.

The behavior is consistent across buying and selling

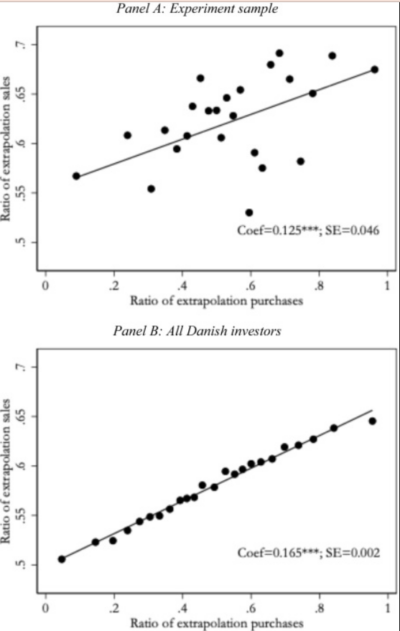

Investors who buy recent winners also tend to sell recent losers. This pattern appears not only in the experimental sample but also in the full universe of Danish investors. That consistency supports the idea that a common behavioral mechanism drives both purchase and sale decisions.

Practical Applications for Investment Advisors

Diagnose return-chasing behavior

Clients may not simply be “aggressive” or “conservative.” Some may systematically extrapolate recent performance into the future. This can lead them to chase winners and hold or sell positions based on biased expectations.

Separate beliefs from preferences

A client’s portfolio choices may reflect biased forecasting rather than true risk tolerance. Advisors should distinguish between what clients want and how they interpret recent performance.

Use disciplined rebalancing rules

Because forecast bias can affect both buying and selling, systematic rebalancing can help reduce emotionally driven or performance-driven security selection.

Pay attention to individualized capital gains

For sales, investors react strongly to their own gains and losses. Advisors should recognize that tax lots, purchase prices, and unrealized gains can shape behavior as much as market-wide performance.

How to Explain This to Clients

“Two investors can look at the same stock chart and reach very different conclusions. One may see recent gains and expect more gains. Another may see the same rise and expect a reversal. This paper shows that those forecasting differences matter. They affect which stocks people buy, which stocks they sell, and how they move money into the market. A disciplined process helps prevent recent performance from becoming the main driver of portfolio decisions. operate”

The Most Important Chart from the Paper

Figure 4 : his figure shows results of regressions of the relation between the ratio of extrapolation purchases and the ratio of extrapolation sales. An extrapolation purchase is defined as a stock purchase following a positive excess return over the prior 12 months, and an extrapolation sale as a stock sale following a negative capital gain. The ratio of extrapolation purchases (sales) is the number of extrapolation purchases (sales) divided by total purchases (sales) calculated over the period 2013 to 2021. The sample is restricted to investors with at least two purchases, two sales, and ten total trades. Panel A includes all subjects in our experiment conditional on meeting the restriction. Panel B includes all Danish investors conditional on meeting the restrictions. The number of observations in Panels A and B are 417 and 316,770, respectively. The solid line is the linear regression line, and the dots present 25 bins of observations.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

We test whether forecast bias affects individual investors’ stock trading by combining bias measures from laboratory experiments with administrative trade data. Forecast bias is positively associated with past excess returns of purchased stocks: Compared to contrarians, extrapolators purchase stocks with higher past returns. Forecast bias is negatively associated with capital gains of sold stocks. Forecast bias also explains investor heterogeneity in the relation between market returns and net flows. Taken together, forecast bias provides a unifying mechanism through which different salient performance measures — past stock returns, capital gains, and past market returns — shape corresponding purchase, sale, and net flow decisions.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.