Diversification is the only free lunch in investing.

If you’ve spent even a day exploring the world of finance, you’ve likely encountered this common truism. But chances are, you’ve also heard stories of someone turning a small stake into millions by going all-in on just one or two stocks. That contrast raises a natural question for many investors: how many stocks should I actually own in my portfolio?

Too many stocks, and you might be leaving opportunities on the table. Too few and you risk losing your shirt!

So how do we strike a balance?

Let’s cut to the chase and start with a foundational principle to guide us through this question.

First off, if you’d rather watch the video version of this blog, make sure to check it out here:

Here’s the bottom line: You should own as many stocks as you can—so long as doing so doesn’t meaningfully hurt your expected return.

Your portfolio’s size should strike a balance between reducing risk and preserving return potential. The main question is: What is that number?

The 20-Stock Myth (and What It Misses)

You’ve probably heard the old rule of thumb: own at least 20 stocks. Where does that come from?

The logic hinges on idiosyncratic risk—the notion that owning just a handful of companies leaves your portfolio vulnerable to any one of them tanking, potentially dealing a serious blow to your nest egg. But as you add more stocks to a small portfolio, that company-specific risk falls off rapidly. By the time you hold around 20 names, most of that risk has been diversified away.

But here’s the catch: that only controls for idiosyncratic volatility. It says nothing about the mean in the midst that idiosyncratic risk. You could pick 20 awful companies and have low idiosyncratic volatility… around a terrible return.

This is what authors Elton and Gruber found in their paper Risk Reduction and Portfolio Size: An Analytical Solution.

“By measuring risk by the dispersion of a portfolio return around the mean return of that portfolio, they neglected the risk associated with the probability that the mean return on the portfolio held will be different from the return in the market. Put another way, the risk from holding a single security rather than the market is not just due to the variability of that security’s return but is also due to the uncertainty of what the average return on that security will be” (416)

In other words, Elton and Gruber reframed risk to include uncertainty around expected returns—not just variability around them. Their conclusion? Holding 20 stocks is not enough.

So how many should you own?

Again, no clear answers here. But according to their paper, most of this risk is minimized around the 50-100 stock mark.

So… More Stocks Is Always Better?

Not necessarily.

Let’s go back to our principle: own as many stocks as you can until you start diluting your return.

If you don’t expect to gain edge via stock selection, holding as many names as you can is not a bad bet. But if you believe you have an edge—whether through active stock picking or systematic investing—then you should consider reducing the number of bets you make.

Factor Investors: Let’s Test It

If you’re a systematic or factor investor (e.g., targeting value or momentum stocks), we can study the numbers.

Let’s examine the largest 1,500 U.S. stocks from 1992 onward and examine portfolios targeting different top slices of value and momentum names—top 5%, 10%, 20%, top third, and top half.

Here are our findings.

Momentum (2-12)

As you can see, the less stocks that were owned, the more return. Although all momentum portfolios beat the market, the difference between the top 50% and top 5% portfolios is dramatic. Holding fewer stocks gave stronger factor exposure—and better returns.

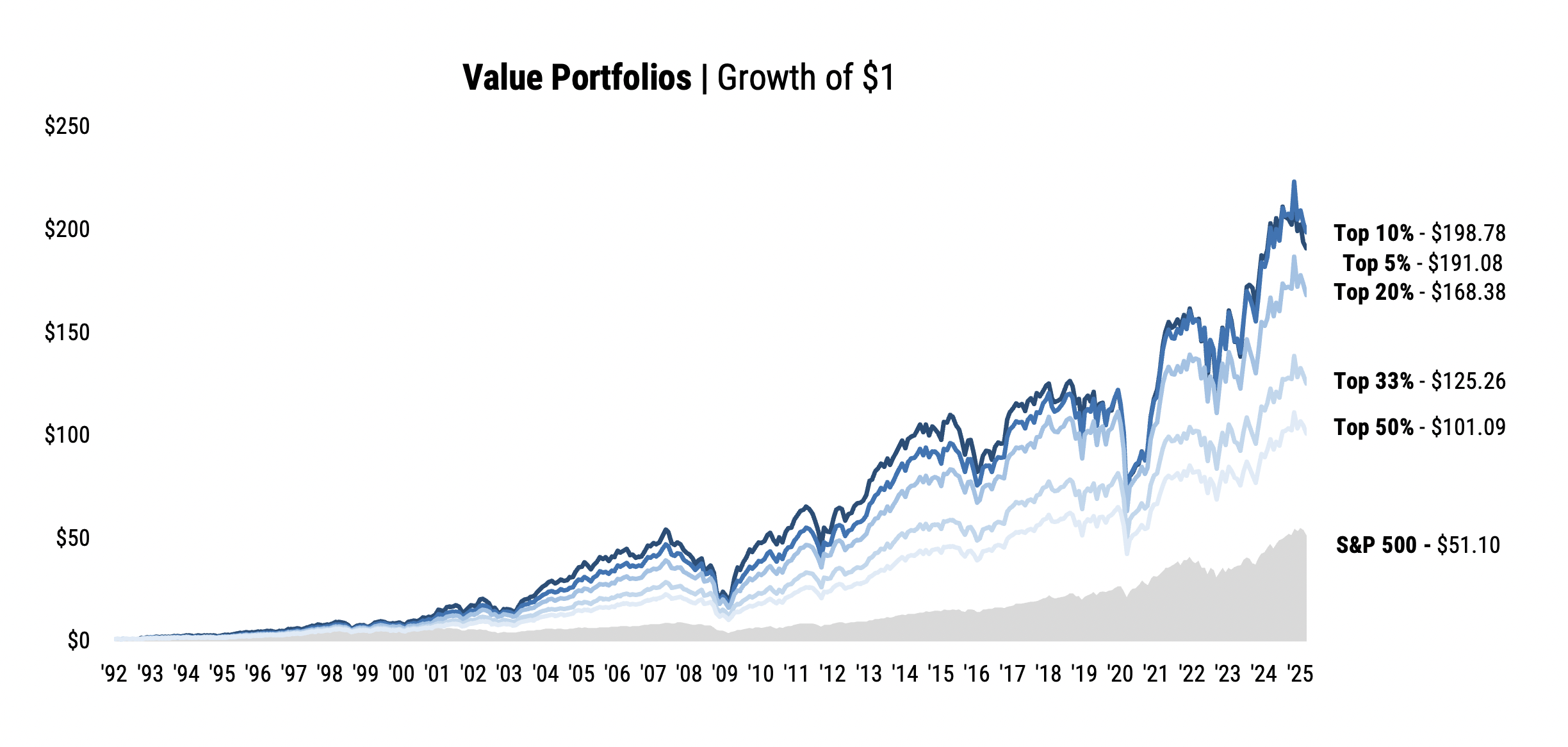

Value (Earnings-to-Price)

Value stocks also showed higher returns with more concentration—up to a point.

Interestingly, the cheapest 5% of stocks slightly underperformed the top 10%. While the “deep value” slice comes with its own challenges during the sample period (likely due to no quality screeners and path dependency of returns), the idea still holds: in general, the cheaper the portfolio, the better the return.

The Concentration Trade-Off

For factor investors, owning fewer, high-conviction names improved exposure and return potential. But that’s a double-edged sword—it comes with greater volatility and tracking error.

So what’s the sweet spot?

There’s no doubt that concentration helped historical long-only factor returns. So if your main goal is “compound your face off” owning 50 to 100 holdings could strike a nice balance between risk and return: Enough names to control idiosyncratic risk without excessively diluting factor exposure.

But What If That Still Feels Risky?

If owning 50–100 names feels too concentrated, there are two smart ways to expand your universe without giving up much expected return:

1. Target Both Factors

Rather than targeting just value or just momentum, consider investing in both. Because these factors are relatively uncorrelated, combining them offers meaningful diversification—without significantly hurting expected returns. Simply owning more names within a single factor won’t improve diversification or boost returns the way incorporating a second, distinct factor can.

2. Go Global

Adding international stocks increases the number of names and adds geographic diversification, but won’t necessarily dilute your factor loadings. You still get exposure to high-octane value and momentum names—just across different economies and markets.

Depending on your level of conviction, this may be enough for your equity exposure (roughly 200-400 stocks in total). But if you still feel uncomfortable with this number of stocks, you can always add the market back to ease tracking error and conviction concerns.

Bonus Tip: Go Beyond Stocks

Once your equity portfolio feels dialed in, consider adding exposure to other asset classes like bonds and commodities, and implement other evidence-based, highly diversifying strategies like trend following.

These can further reduce volatility and smooth returns—especially in challenging equity environments.

Final Thoughts

To summarize what we’ve talked about:

- 20 stocks may reduce volatility, but it’s not enough to reduce return uncertainty.

- 50–100 stocks strikes a better balance between expected return and risk.

- For factor investors, concentration improves returns—owning less stocks has historically improved returns.

- Seek smart diversification by investing in both value and momentum both in the U.S. and international markets.

At the end of the day, your portfolio should reflect a strategy you believe in and can stick with over the long haul. If adding broad market exposure helps you stay the course, that’s a perfectly reasonable path. But even introducing a modest allocation to concentrated value and momentum has historically made a meaningful difference—enhancing both diversification and long-term return potential.

Sources: Elton, Edwin J., and Martin J. Gruber. “Risk Reduction and Portfolio Size: An Analytical Solution.” The Journal of Business 50, no. 4 (1977): 415–37.

About the Author: Jose Ordonez

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.