Core Research Categories

Click Here for Category Archive

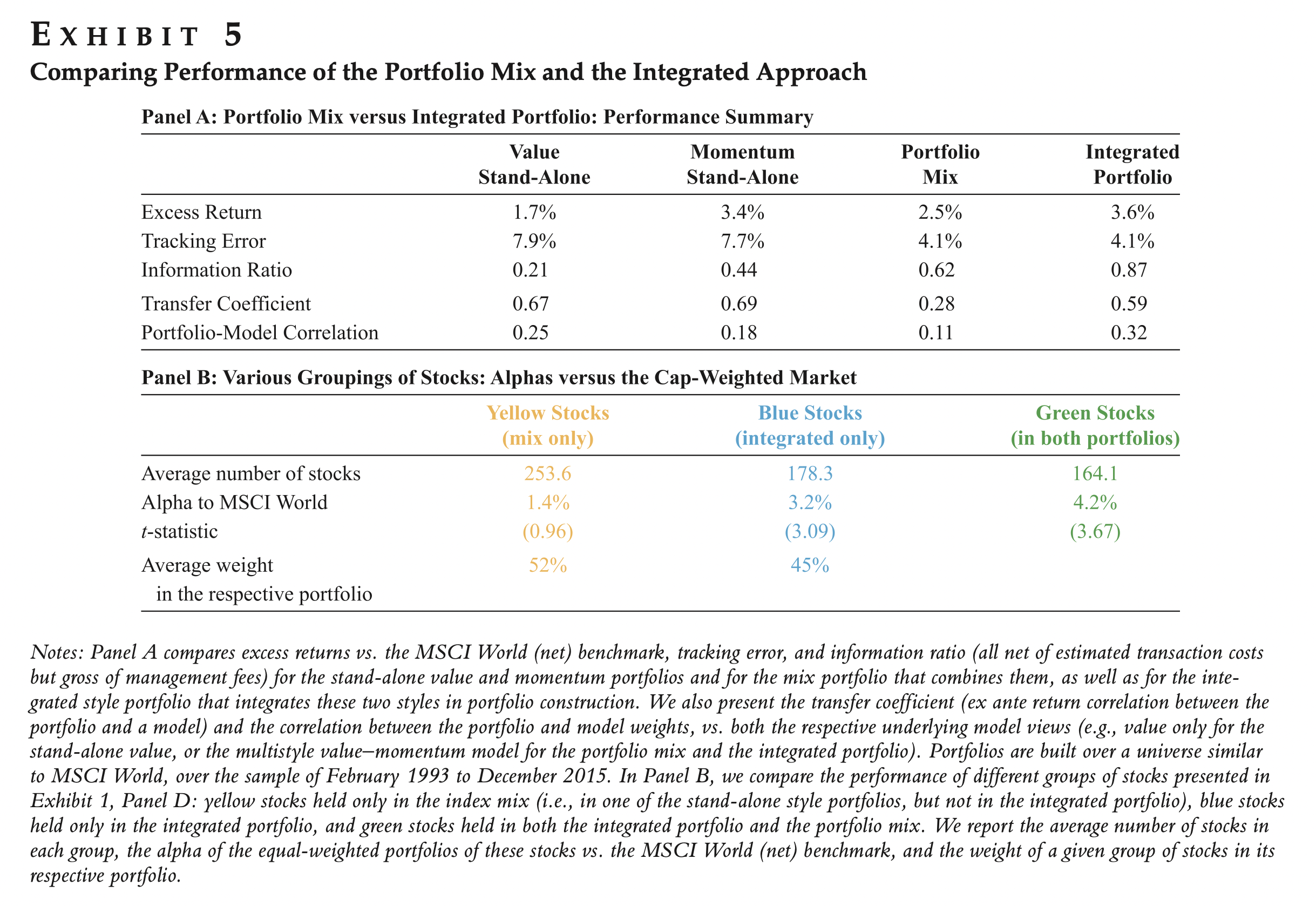

US Value Stocks Trading at Historically High Discounts

April 4th, 2025|

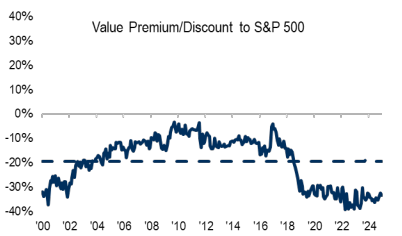

Valuations Reflect U.S. Exceptionalism

February 28th, 2025|

Analysts set price targets using trailing P/E ratios

September 30th, 2024|

Can smart rebalancing improve factor portfolios?

September 3rd, 2024|

Click Here for Category Archive

Revaluation Alpha: Why Past Factor Returns May Be Misleading

January 30th, 2026|

Do indexes time the market?

January 20th, 2026|

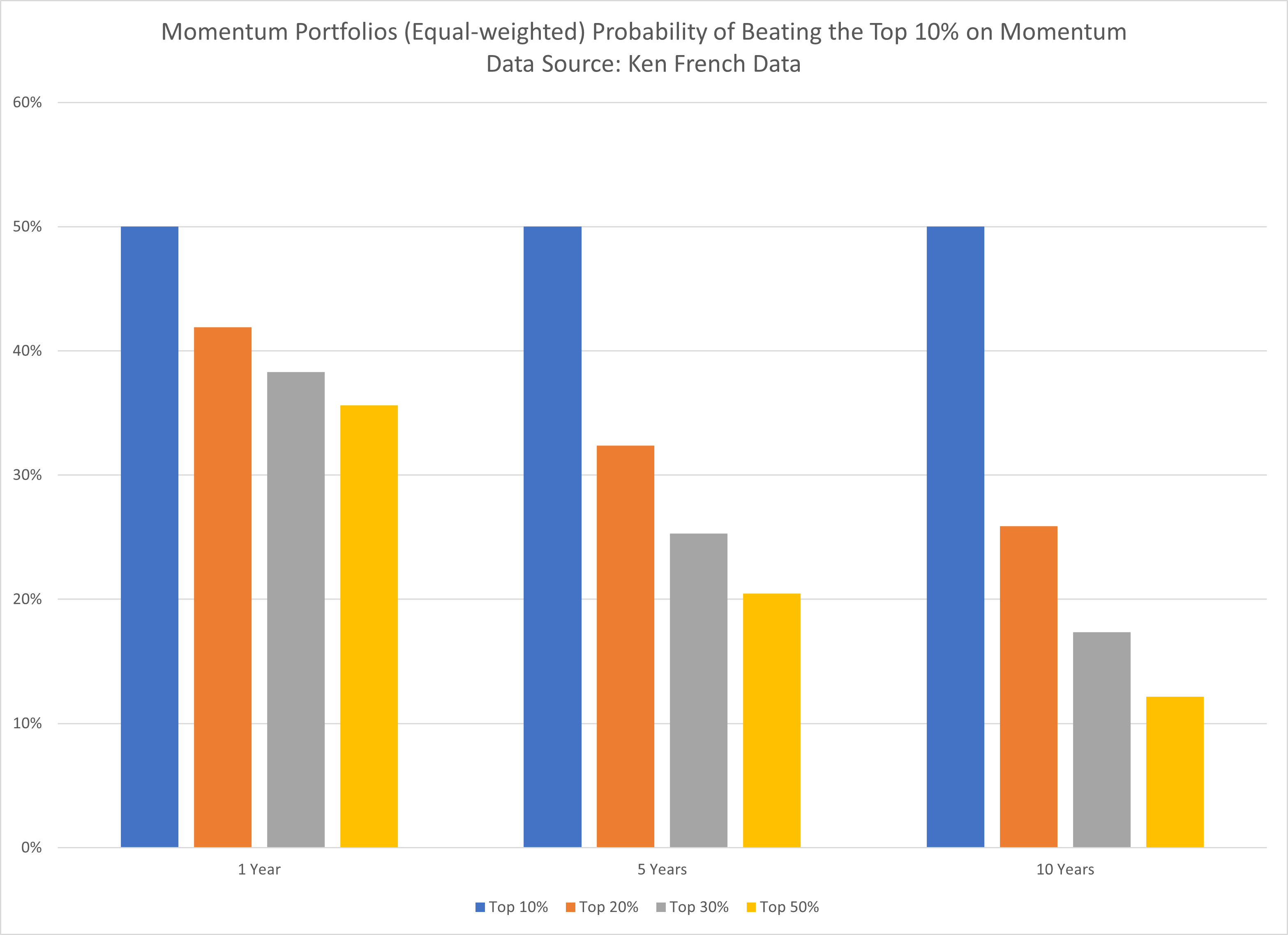

Momentum factor investing: Evidence and evolution

November 24th, 2025|

Click Here for Category Archive

Book Review — Market Timing with Moving Averages

December 20th, 2017|

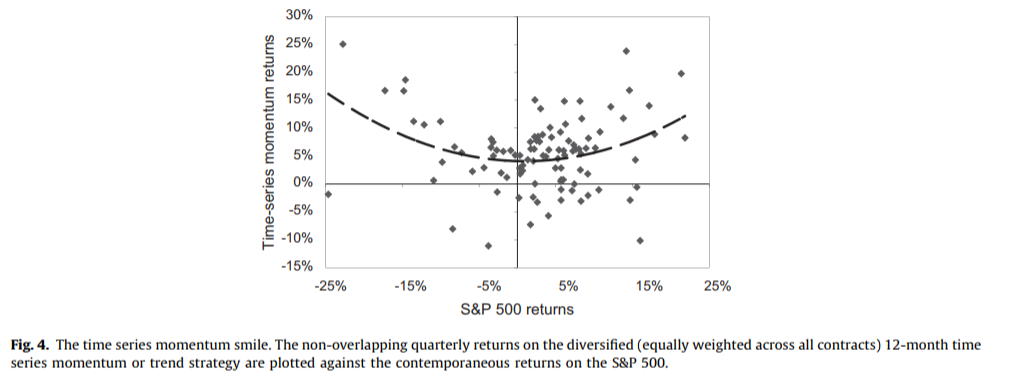

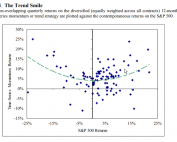

Diversification Benefits of Time Series Momentum

August 10th, 2017|

Do Trend-following Managed Futures Increase Safe Withdrawal Rates?

November 8th, 2017|

Time Series Momentum (aka Trend-Following): A Good Time for a Refresh

February 8th, 2018|

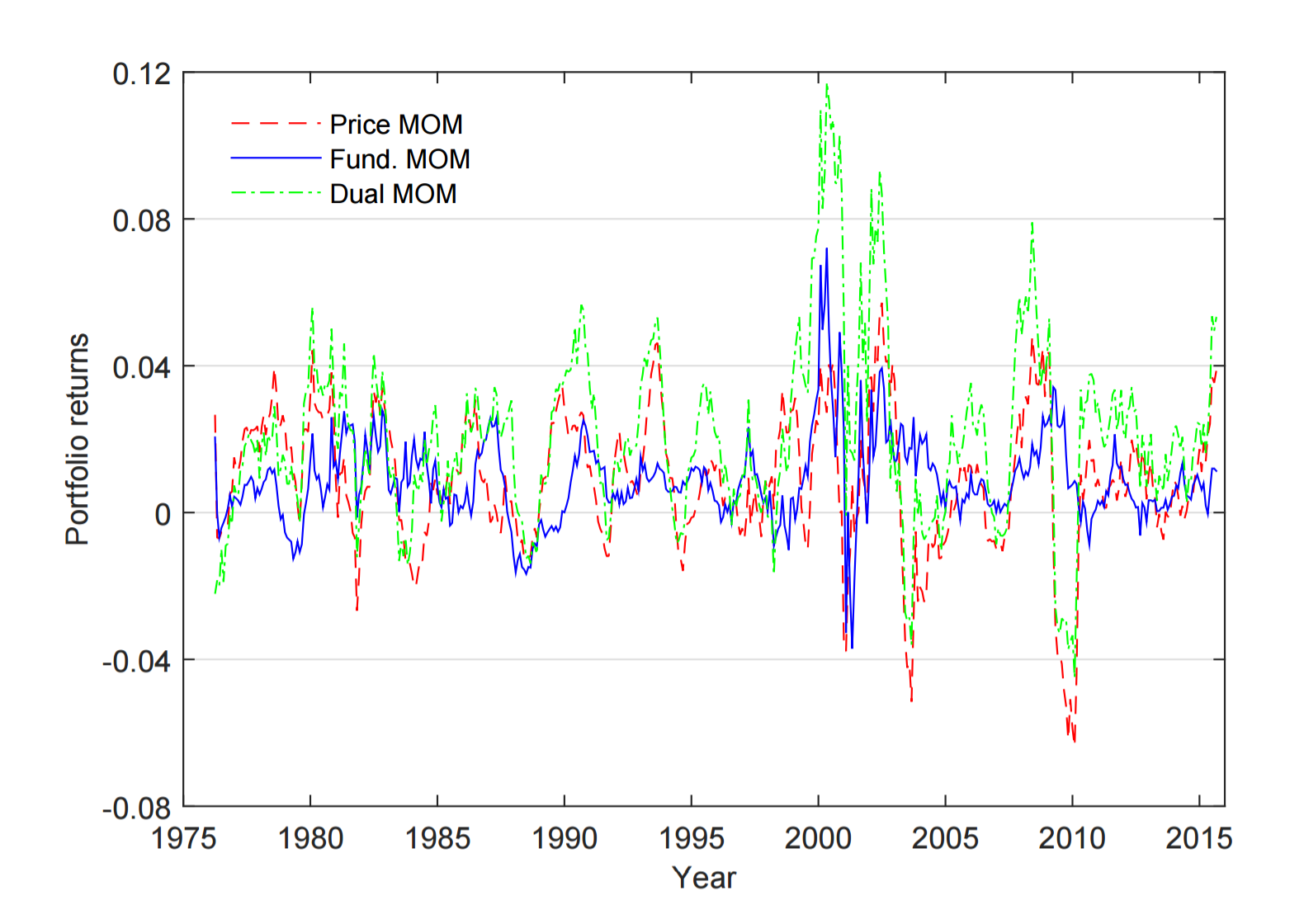

Dual Momentum with Stock Selection

March 14th, 2017|

Click Here for Category Archive

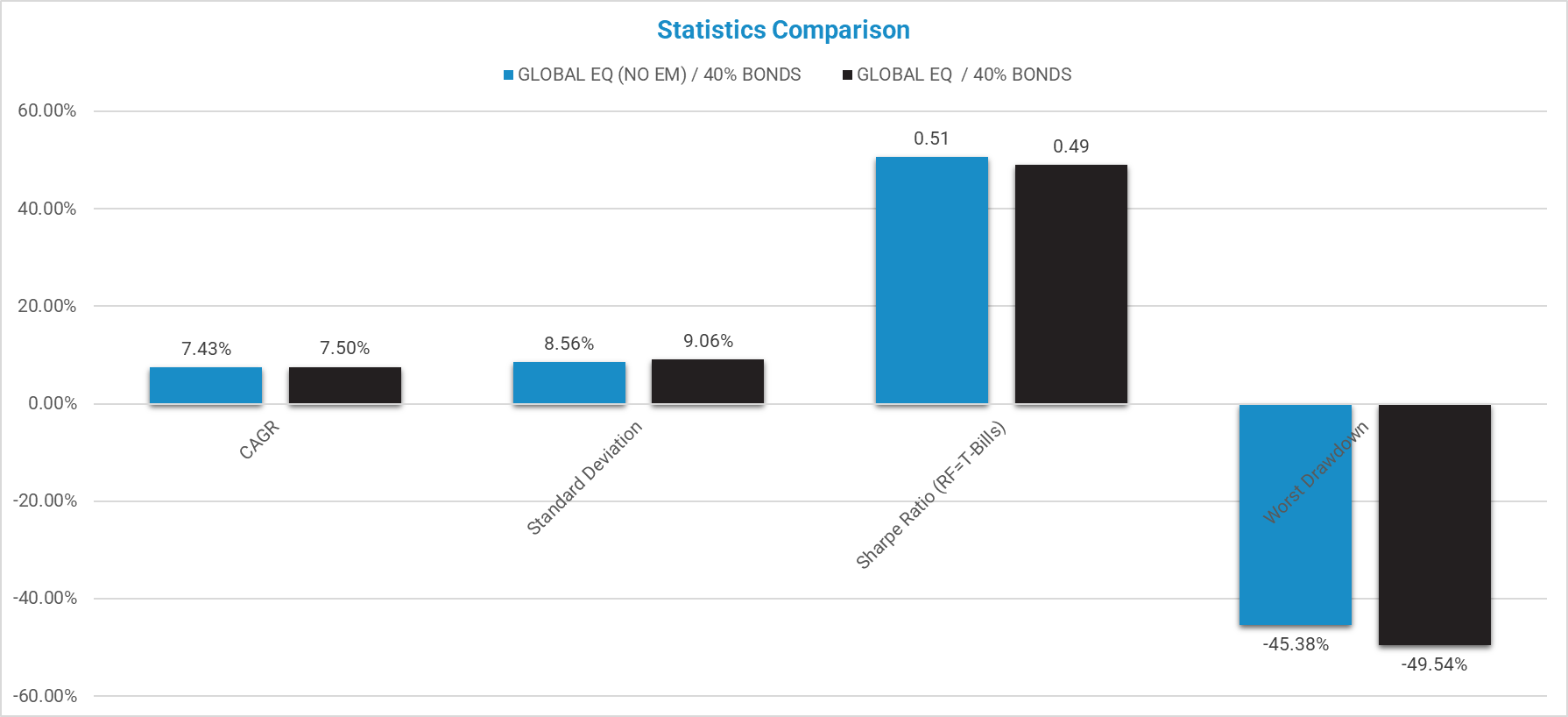

Does Emerging Markets Investing Make Sense?

June 17th, 2022|

How to Start an ETF? Resources and FAQ

November 16th, 2021|

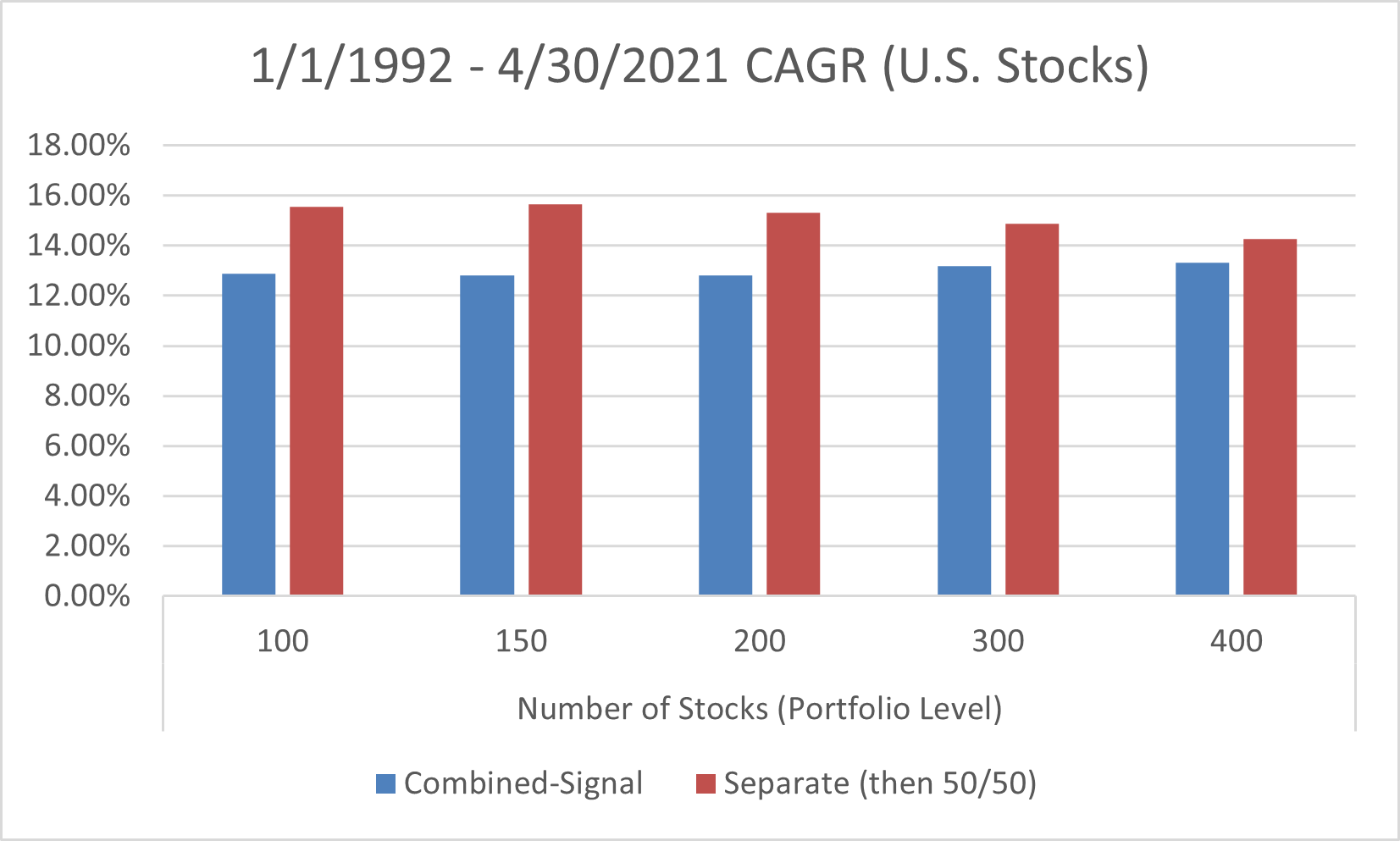

Value and Momentum Investing: Combine or Separate?

May 25th, 2021|

How Portfolio Construction Impacts the Reliability of Outcomes

April 16th, 2021|

Value Investing: An Examination of the 1,000 Largest Firms

August 18th, 2020|