Core Research Categories

Click Here for Category Archive

Fixing the poor performance of the book-to-market ratio

August 19th, 2024|

On the Persistence of Growth and Value Stocks

February 16th, 2024|

The Magnificent Seven

November 17th, 2023|

International Value Stocks Offering “More Bang for the Buck”

October 5th, 2023|

Value and Profitability/Quality: Complementary Factors

August 11th, 2023|

Click Here for Category Archive

Enhancing Momentum Strategies

June 13th, 2025|

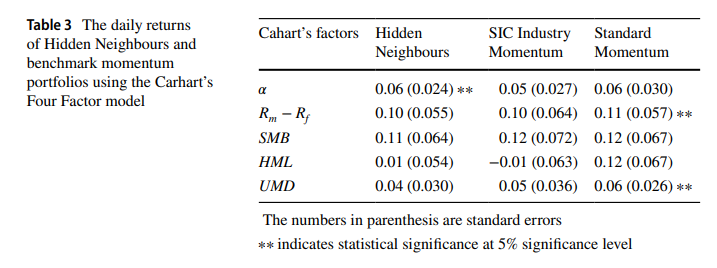

Enhancing Industry Momentum Strategies: Finding Hidden Neighbors

April 18th, 2025|

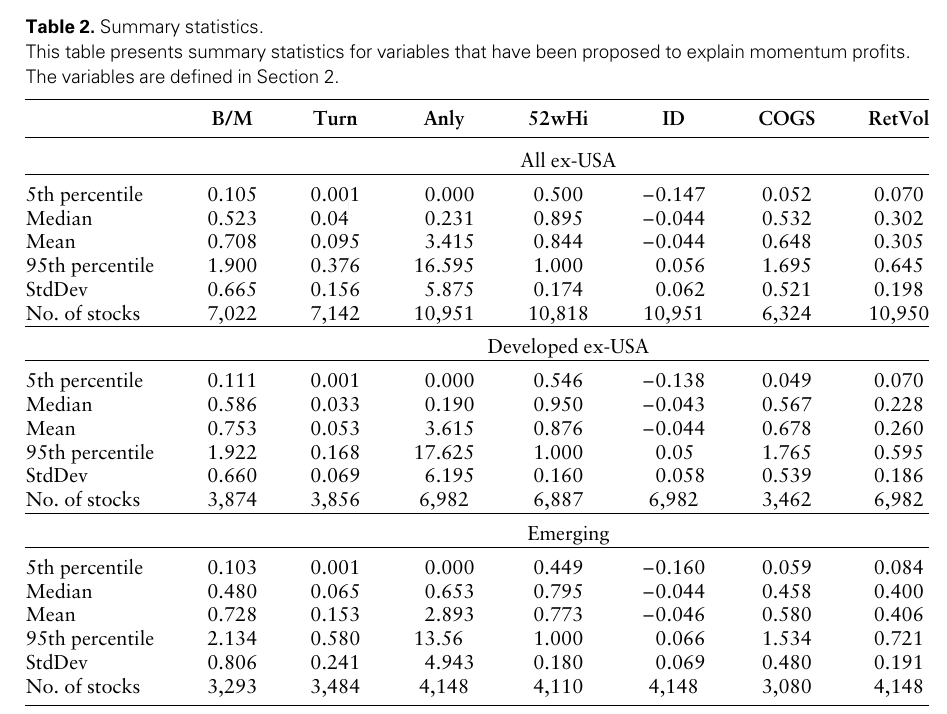

Understanding What Drives Momentum in Global Stock Markets

April 7th, 2025|

Frog in the Pan Momentum: International Evidence

December 9th, 2024|

Can smart rebalancing improve factor portfolios?

September 3rd, 2024|

Click Here for Category Archive

Natural Gas and Oil Spread: Opportunity or a Pain Trade?

October 5th, 2012|

News and Google Hits: A Path to 20% Alpha?

December 9th, 2012|

Tactical Asset Allocation Insights via the Geeks from Thinknewfound

February 16th, 2017|

Technical Analysis may actually work!

May 2nd, 2011|Tags: Technical Analysis, Cross-Sectional Profitability, abnormal returns|

The Dirtiest Word In Finance: Market Timing

March 20th, 2017|

Click Here for Category Archive

Value Factor Diversification: Is Quality Better Than Momentum?

June 26th, 2020|

ETF-prenuers: An Introduction to ETF White Label Services

June 24th, 2020|

What’s the Story Behind EBIT/TEV?

May 1st, 2020|

Is Passive Investing Better than Active Investing?A Critical Review.

January 2nd, 2020|

Trend Following: The Epitome of No Pain, No Gain

June 26th, 2019|

Momentum Investing, Like Value Investing, is Simple, but NOT Easy

September 18th, 2018|