Are you considering investing in a buffer ETF?

Like with any investment product, it’s important to fully understand both the benefits and the risks before allocating capital. On the surface, buffer ETFs appear attractive: they seek to capture some upside while mitigating a portion of losses. However, this does not mean they are risk-free. In fact, under certain market conditions, these products can significantly underperform.

To see why, let’s first review how buffer ETFs are structured, then explore the risks they pose, and finally consider whether there are more effective alternatives.

By the way, this is the second of a three-part series on Buffer ETFs. If you want to read part 1, where we go through the ins and outs of how buffer products are built, make sure to check it out here.

Before that, if you’d rather watch the video version of this blog, make sure to subscribe our YouTube channel and follow this series there:

Let’s begin.

How Buffer ETFs Are Built

At their core, buffer ETFs use options strategies to engineer defined payoffs. The basic structure involves:

| Option Leg | Effect |

| Long deep in-the-money call | Mirrors equity-like payoffs |

| Long at-the-money put | Seeks downside protection |

| Short out-of-the-money put | Monetizes long positions; determines the buffer size |

| Short out-of-the-money call | Monetizes long positions; determines the cap |

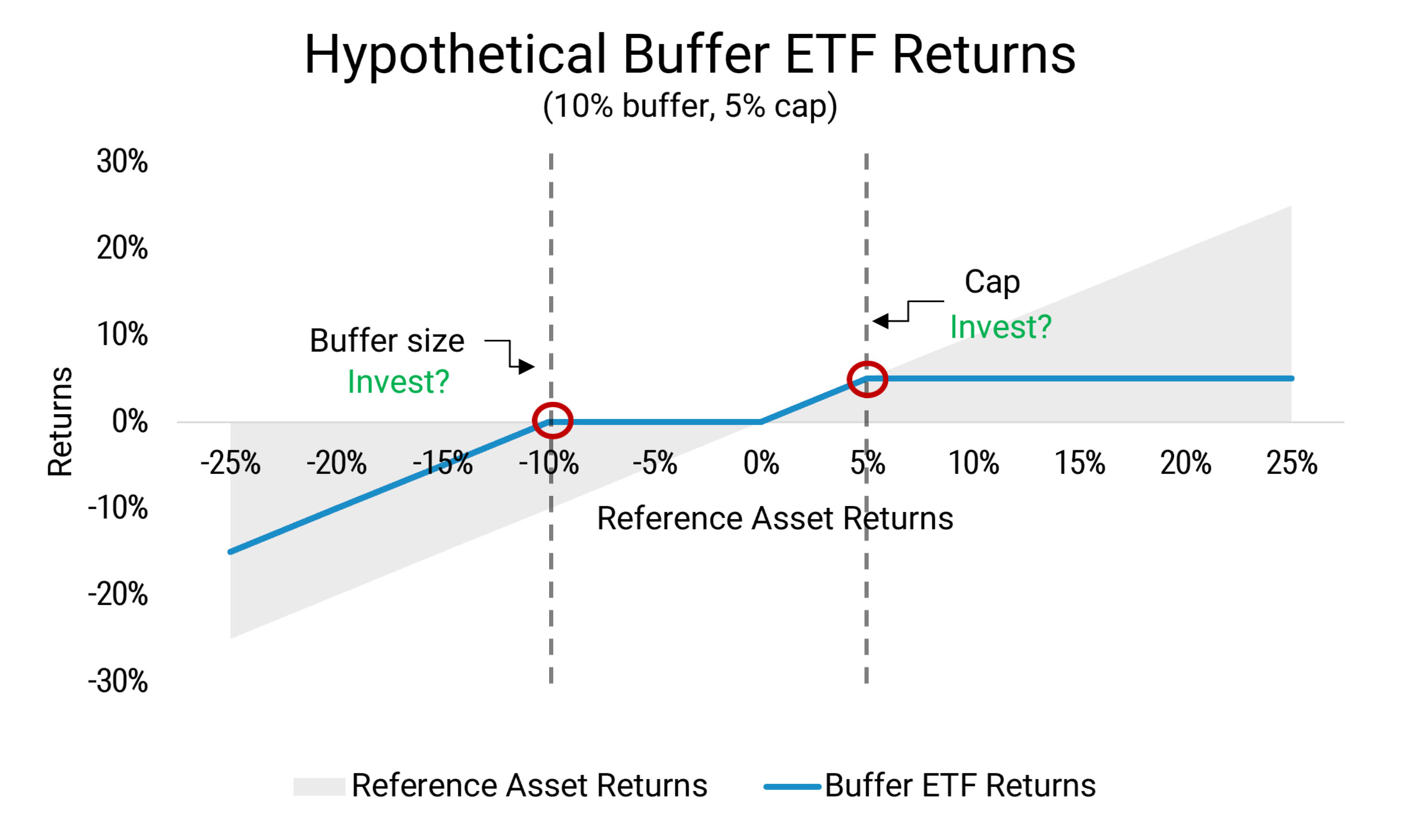

As an illustration, consider a hypothetical 10% buffer / 5% cap ETF. A manager would likely construct this buffer by monetizing the long positions by selling a 10% out-of-the-money put and a 5% out-of-the-money call.

Complexity and the Investor’s Dilemma

If the structuring has you scratching your head, you’re not alone. Options can be powerful, but they’re definitely complex. For many investors, buffer ETF mechanics feel like a maze—and it’s fair to wonder:

Can we get the same kind of payoff without all the financial gymnastics?

Why reinvent the wheel, layering on complexity, if a simpler setup can deliver something similar?

Don’t Take Your Buffer to the Grand Canyon

Picture this: a parent takes their kid out for a bike ride. The kid’s got a helmet on, so a tumble means maybe a scraped knee, not a trip to the ER.

Now change the setting. Same kid, same helmet, but this time they’re pedaling along the edge of the Grand Canyon.

Another parent sees this and yells: “What are you doing? Get that kid away from the cliff!” If your answer is: “Relax. He’s wearing a helmet”, you probably need a course or two on risk management (and parenting).

A helmet won’t stop a 1,000-foot drop.

Buffer ETFs work the same way. They’re fine for small bumps in the road, but if you’re banking on them to save you in a true market freefall, you’re fooling yourself.

Key Pitfalls of Buffer ETFs

Before going over the risks embedded in structured products, ask yourself the following three questions before buying a buffer ETF:

- Would you buy at the cap, when there is only downside?

At that point, the ETF offers no upside and only downside. Owning the underlying asset directly would at least preserve the possibility of future gains. - Would you buy at the buffer, when there is mostly downside?

Here, you face all the downside of the underlying but without its full upside potential. You’re assuming the same risks while limiting your returns. - If you wouldn’t buy at these critical points, why would you hold?

This reveals a structural issue: the ETF payoff can discourage holding at precisely the wrong times.

Simplifying the Payoff

Rather than thinking in terms of strikes, shorts, and longs, let’s make this way easier and think of these payoffs in terms of a normal distribution.

- The green area represents modest gains you can reasonably expect to capture most of the time.

- The gray area represents the small losses you may avoid thanks to the buffer.

- The red tail represents the extreme losses investors weather during severe market downturns.

- The right tail represents extreme gains that come once-in-a-blue-moon.

Unfortunately for buffer ETFs, the left tail is exposed, while the right tail is capped.

In practice, buffer ETFs leave investors missing out on life-changing gains while still being exposed to life-changing losses. This is why when examining performance data, buffer ETFs have often delivered disappointing results. By design, they seek to smooth returns, but this smoothing effect leaves wide gaps that must be addressed.

This combination can result in risk-adjusted underperformance, especially when compared to simpler strategies like holding equities outright or using more transparent hedging approaches.

Toward Better Solutions

So what can investors do?

If the goal is risk management, it may be worth exploring strategies that are:

- Simpler – easier to understand and monitor.

- More affordable – lower costs and fewer hidden trade-offs.

- More effective at addressing tails – targeting both catastrophic downside risks and the potential for outsized gains.

In our next blog we will explore alternatives to buffer ETFs that aim to close these gaps, offering investors the potential for better defense and better upside capture.

Final Thoughts

Buffer ETFs are marketed as an elegant middle ground between risk and reward. But upon closer inspection, they may be over-promising protection and under-delivering returns.

For investors, the key takeaway is not that buffer ETFs are inherently bad, but that they do not solve the core challenges of portfolio risk management. Before allocating to these products, investors should ask themselves whether the trade-offs truly align with their long-term objectives.

At the end of the day, thoughtful portfolio construction, robust diversification, and disciplined risk management may achieve what buffer ETFs promise—without the complex structures.

Read the third and final installment of this buffer ETF series and learn how to potentially improve upon or better recreate buffer ETF strategies.

About the Author: Jose Ordonez

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.