Assuming you haven’t been living under a rock, you’ve almost certainly heard something about robo-advisors. Millenials seem to love them while “old school” advisors are dismissive at best or terrified at worst. Some even believe they are poised to take over the investment management industry entirely. For better or worse, we even went ahead and built our own active robo-advisor over the past 6 months (built from scratch with in-house developers).

But what exactly are robo-advisors and why are some people freaking out about them?

Robo-advisors represent a product, but they also represent an idea. On the product front, a robo-advisor is simply software that executes an investment program. This concept has been around for many years–ever heard of a lifecycle fund? Robos just make this concept more user-friendly and accessible.

As an idea, robo-advisors represent a revolution for financial services: traditional financial advice can be too complex and too opaque; however, this advice can be simple and transparent. Robos directly facilitate this revolution. With this new transparency comes lower costs and thus, better expected performance.

Whether or not this revolution is real or perceived is in the eye of the beholder. In one corner you have Adam Nash, CEO of Wealthfront, preaching to the choir; however, today’s reality is that robo advisors only make up a few basis points of the total advisor market! No doubt the marketplace will change, but growing from 2 bps to a meager 2 percent of assets under management would require heroic growth. We believe robos are here to stay, but the timing of their final dominance is anyone’s guess. We also believe that robo-advisor technology should not be viewed as a threat to advisors, but as an opportunity to build a better customer experience and to service a less affluent client base.

Note: to get more depth on robos and the financial landscape, one can read our articles at the Wall Street Journal, the CFA Institute, and our treatise on making advice simple and transparent: DIY Financial Advisor: A Simple Solution to Build and Protect Your Wealth. Of course, there is also a variety of lucid analysis from other bloggers out there, such as AbnormalReturns, Kitces, Josh Brown, and Meb Faber (click the links to get their thoughts on robos). Victor Reklaitis also has a nice perspective of the robo landscape in the WSJ.

Why we built an active robo-advisor and why all advisors should consider it

Although every investment advisory business is different, we think our own experience can shed light on how and why the robo concept can be a good fit with almost any advisory business.

We have historically focused on delivering sophisticated, active exposures for tax-sensitive, long-term investors. Translation: we only work with really rich people. We love the high-net-worth and family office business and this will continue to be our main effort; however, delivering affordable, active solutions should not be limited to the rich and famous. On a daily basis, we get young professionals reaching out, saying: “I love you guys, love the research, and I’ve learned so much. I want to get involved. Can you manage my IRA account with $50k in it?”

Of course, such messages make us feel good that we are accomplishing our mission to empower investors through education, but we are obliged to turn away the business (and direct them to our free tools, etc.). We’re sure this happens to other investment advisors too.

Why can’t most advisors serve small clients?

Economics. In order to serve a small managed account (which involves a lot of marginal labor and other costs) we would have to charge so much that it would no longer be a win-win. One of our core beliefs is finding win-wins, so we can’t justify doing it, even if it means losing some clients that are willing to pay high fees.

With 8 full-time quant/computer geeks (and a small army of consultants/1099ers), we can realistically handle only a limited number of “high-touch, white glove” accounts. If we accepted every small request, we would quickly go out of business. This is why we maintain a $1M minimum for separately managed accounts. Without size, we cannot accomplish our goal to deliver affordable alpha.

But technology created an opportunity to support the little guy, efficiently.

We watched the investment landscape transforming with the rise of robo-advisors. Cloud-based advisors were springing up everywhere, delivering passive solutions to small accounts. A light bulb turned on. Why aren’t we doing this? Granted, we don’t have a $100 million in venture capital to burn on overpriced marketing and Palo Alto office space, but we do have the internal programming talent, a deep bench of financial knowledge, and actual experience as a financial advisor. But who needs strings-attached venture capital at frothy valuations?

But we had to be different. We didn’t want to spit out another generic allocation program that invested in generic Vanguard funds. The world already has a 0.30% advisor solution for that: Vanguard Advisor Services (human included). As an alternative, we created a robo-advisor that leverages our research and development and does something different. But doing something different than buy and hold Vanguard funds requires a deep knowledge of financial markets. And the VC-backed robos are technology companies first, but their asset management skills run a distant second. We think they sometimes make basic mistakes in their approach to asset management.

Thankfully, we are both a technology company as well as an asset manager. We can compete on technology and we think we have an edge versus the generic robo crowd when it comes to financial knowledge.

Disclaimer: We don’t claim to have a monopoly on good ideas and our solutions are not for everyone. Each client has unique circumstances, psychology, goals, and needs. Some investors probably don’t need an advisor, and we’ve written a book dedicated to helping those people achieve their goals, independently: DIY Financial Advisor. But many investors really need an advisor. And to be clear, these investors need a good advisor: honest, affordable, transparent, and focused on process–not performance. Good advisors often, but not always, serve a role in helping investors achieve their goals. So while we present our own logic behind our active robo advisory solution, we think all advisors and asset managers with good ideas need to get things set up with a robo-advisor. We don’t have a monopoly on good ideas. There are some incredible thinkers out there and most of them aren’t at large institutions — they’re out blogging and educating the investing public.

Our active robo-advisor: A unique application of robo-advisor technology

An active robo-advisor? Whoa, hold on. Isn’t “active” a dirty word in asset management these days? Like a North Korean military parade, every “expert” seems to be goose-stepping to the drumbeat of passive investing. Almost all robo advisors are passive, and why not? Active managers, in the aggregate, underperform passive investing by approximately the amount of their management fee. This finding is widely documented in academic research. Thus, it makes sense to stop trying to beat the market, go passive, and focus on lower fees. This approach is Jack Bogle’s formula for long-term success (Ben Carlson has a nice example showing the success of the “Bogle” approach). Of course, this approach can work: lower costs for passive ETFs, plus low robo management fees, equals a decent solution. The math works against a traditional financial advisor trying to compete with this solution.

So why build an active robo-advisor? This would seem to fly in the face of Bogle’s logic. Shouldn’t we all just drink the passive Kool-Aid and join the parade? Not so fast.

There are three reasons why we believe an active robo-advisor can add value:

- We believe stock prices aren’t perfect: The research is clear: Non-closet-indexing portfolios, with value and momentum characteristics, generate higher expected returns than passive portfolios.

- We believe in downside protection: Buy and hold won’t get you there. Protecting a portfolio from large losses matters and trend-following seems to be a reasonable approach.

- We believe in affordability: Affordable active solutions can create long-term win-wins.

1) We believe stock prices aren’t perfect

The Efficient Market Hypothesis (EMH) states that it is impossible to beat the market, since prices always reflect all available information. We agree with the implication (money doesn’t grow on trees), but disagree with the logic (efficient prices prevent money from growing on trees). We believe prices are NOT always correct, but also recognize that exploiting opportunities is costly. On net, prices are sometimes not correct (EMH is wrong), but money still doesn’t grow on trees (markets are competitive).

In order for an active approach to work, an investor needs to identify 1) a process that presumably works, but 2) also needs to identify how to minimize the cost of exploiting these opportunities. The biggest cost of active approaches is the requirement that an investor have a long-horizon and a willingness to maintain discipline to a specific approach. In other words, investors in active strategies need to have the courage and conviction to be the last man standing when these strategies inevitably “stop working” and before they start working again. Or perhaps you like the United States Marine Corps adage, “Pain is weakness leaving the body.” Bottomline: active investing is simple, but not easy.

Which active strategies have stood the test of the time and require extreme discipline and courage to exploit?

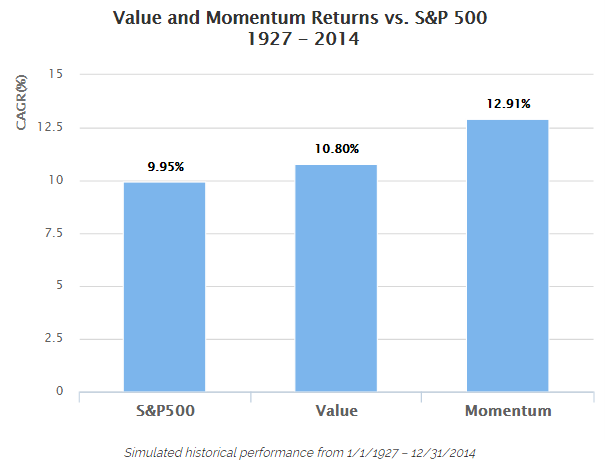

There is endless debate on “what works,” but of all the so-called anomalies in the world, buying cheap stocks (value) and buying strong stocks (momentum) seem to be the most compelling. Additionally, combining value and momentum in a portfolio generates a risk/return profile that is still unexplained by traditional asset pricing models. In short, we believe in a value and momentum system and we’re sticking to it.

Below we highlight some basic historical results associated with generic value and momentum strategies, as described in the academic literature:

- Data for Value and Momentum portfolios are taken from Ken French’s website: Value and Momentum.

- The Value portfolio is formed annually, while the Momentum portfolio is formed monthly.

- The returns shown are net of fees as follows: Value portfolio (1.00% management fee and 0.50% transaction costs); Momentum portfolio (1.00% management fee and 2.50% transaction costs).

- The S&P 500 portfolio is the S&P 500 Total Return Index and is shown gross of any management fees or transaction costs.

- Hypothetical performance results have many inherent limitations, some of which, but not all, are described in these disclosures. No representation is being made that any fund or account will or is likely to achieve profits or losses similar to those shown herein. In fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently realized by any particular trading program. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

- All returns are total returns and include the reinvestment of distributions (e.g., dividends).

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

The results are clear: buy cheap stocks that everyone hates and buy strong stocks that everyone loves. We’ve got our own ideas on how to exploit the value premium and the momentum premium, but in the end, value and momentum are open secrets. The reason we believe these well-established strategies will continue to be effective is because they don’t work all the time. You should be skeptical if someone says a strategy will work all the time (ask Madoff’s investors).

2) We believe in downside protection

Most robo advisors, consistent with passive investing, believe it is a fool’s errand to try to “time” the market. As the story is told, investors simply need to identify an asset allocation mix that is appropriate for their risk tolerance and simply ride the rollercoaster with a buy and hold mentality. Throw in an annual rebalance to keep things proportional.

While this approach is 1) fairly tax-efficient, 2) cheap, and 3) diversified, buy and hold approaches do not protect an investor from experiencing large drawdowns. The 2008 Financial Crisis is a perfect example of diversification gone awry. When correlations go to 1 (that’s quant speak for something stinky hitting the fan), as they tend to do during a crisis, owning a “well-diversified” portfolio simply means everything you own–save Treasury Bonds–goes down at the same time. Buy and hold simply accepts substantial drawdowns as part of the business. For example, an equal-weight portfolio mix of passive domestic equity, developed market equity, real estate, commodities, and 10-year Treasury Bonds suffered a maximum drawdown of -46.3% from May 2008 to February 2009. A more risk-averse and “well-positioned” investor with 60% in domestic equity and 40% in 10-year Treasury Bonds didn’t fair much better, with a -28.1% drawdown from Nov 2007 to February 2009. God bless diversification, but diversification isn’t a panacea (as some robos position themselves). To see why downside protection matters, look no further than the chart below.

If an investor experiences a 50 percent loss on a portfolio, at a 7 percent return, it will take almost 11 years to recover. But if an investor keeps the drawdown manageable, say to 15 percent, then the recovery period is under 3 years. For retired investors or investors with sensitivity to large losses, telling them to simply buy and hold after a 50% face-rip is a great way to lose a few teeth or have one’s nose broken. Implementing some form of downside protection, in addition to good old-fashioned diversification, seems like a good idea, assuming there is some reasonable way to do it.

But how does one avoid massive drawdowns?

There are only two ways to prevent large drawdowns:

- Bury your money in watertight boxes throughout your backyard

- Use a system to time market exposure

Option 1 has obvious costs — no returns — but obvious benefits — no losses. For those who prefer market returns (or live in a condo without a yard) Option 2 has some promise. “Timing” is a dirty word among many in the business, but we don’t represent the “many” and we don’t feel like eating large losses. If the evidence supports something that could work, we are happy to be non-conformists. Like many research and data-driven academics, we are natural skeptics, so our baseline view for the “how do we minimize large drawdown” question is that nothing could beat buy-and-hold. However, our research led us to a compelling alternative hypothesis: long-term trend-following. We believe there is substantial evidence that following simple, rules-based trend-following systems, can prevent large portfolio drawdowns, without having a substantial impact on long-term expected returns. Of course, there is no free lunch — sticking to these systems is incredibly difficult and requires extraordinary discipline. Also, these systems do not minimize volatility (that is why portfolios earn expected premiums over time), and there is a non-trivial risk of whipsaws — getting out of the market when it heads down and then seeing it shoot immediately higher. But for our specific mission — trying to minimize large drawdowns — trend-following is our best solution.

Remember these three takeaways:

- Many robo-advisors place you in buy-and-hold portfolios because they believe timing the market is impossible, and no one can be blamed when the portfolio suffers a major loss (“Hey, all the other advisors are also down a bunch, you can’t fire me!”).

- Market drawdowns can decimate your wealth. It can take years, if not decades, to recover.

- Our robust risk management system is designed to mitigate major market drawdowns and help preserve capital when markets correct.

3) We believe in affordability

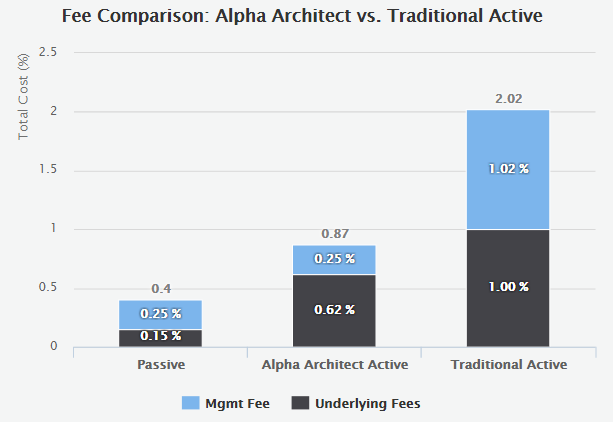

Recall that most robo advisors are predicated on the notion of providing the absolute lowest cost approach, which relies on cheap passive allocations. Nothing is wrong with buying as cheap as possible. If you are buying a commodity, whether it be gasoline, corn, or low cost passive indices, cheaper is better. But active investing is not about being low cost, but rather, it ‘s about being the highest value. Truly active strategies have scalability issues and are costly to develop and operate, which means the following:

- An investor can certainly use a passive robo-advisor and pay an all-in fee of around 0.4%–not a terrible decision. However, you sometimes get what you pay for (see drawdown discussion above).

- We will never deliver the lowest cost strategy in the market–that’s not our goal–but we do seek to be the best value in the market. We want to deliver high quality at half the cost of the all-in costs of traditional active offerings. Plus, you can always call and get a human to answer the phone.

- We seek to deliver an affordable, active, globally diversified, downside-protected, asset allocation solution. Passive robo-advisors don’t deliver these important elements!

Fee estimates are based on current fee structure but are subject to change. Underlying fees for the comparison above reflect the “Moderate” risk exposure. Fees can be higher or lower for different risk exposures. Management fee estimate based on Parametrix 2015 report and underlying fee for Traditional Active (1%) is based on estimates from the Forbes Article: “The Heavy Toll of Investment Fees.”

What’s the bottom line? We want to create an alternative to expensive active management for investors with limited assets (Billionaires can negotiate better fees than the rest of us and get cheap active management already). We can accomplish this mission because we are technology-focused (higher operational efficiency) and we are a vertically integrated firm with asset management capability and advisory capability. We are also a direct-to-consumer oriented firm: We don’t pay brokers or banks to sell our products.

In the end, we want our products to be bought, not sold.

We’re also up-front about our investment services. We tell people what we’re going to do and how we’re going to do it. We also plow a majority of our personal investable capital into our strategies. If an investor believes in what we believe, we should do business; if an investor doesn’t believe in what we believe, there are armies of financial service firms in the world that will be ready to accept their business. Of course, our vertically integrated system, where we serve as the investment advisor and develop some of the underlying investment products, creates an inherent conflict of interest because we have an economic incentive to use our own asset management products at the expense of other products. For example, there might be a “better” value investing strategy available in the market, but because we receive fees on the use of our value investing strategy, we will use this product instead of the “better” version. On the flipside, the upside of our vertical integration is we can lower total costs to the consumer because we have the capability to serve as an advisor and investment product developer, simultaneously (Vanguard has a similar model in the passive space with Personal Advisor Services). Nonetheless, despite the opportunity to lower total costs to the consumer, we understand there is a potential conflict of interest in the use of our “proprietary products” and we have structured our culture and compliance program to deal with this reality. Moreover, we try and minimize the issue for clients by being radically transparent about our processes, by investing our own capital in our own products, and by serving as a legal fiduciary on all advisory services–we always seek to do the right thing based on our assessment of the evidence and the client’s goals. Assuming an investor can get comfortable with our approach to addressing the inherent conflict of interests associated with an advisor that also manages funds, in return, these clients can access an affordable active management solution that seeks to deliver a strong value proposition at lower costs. We can deliver lower costs because we can serve as both an advisor and asset manager, which means we gain economies that we can pass to the consumer.

We have a different option for investors

If you have reviewed and have confidence in the evidence relating to 1) active value and momentum expected long-term returns and 2) the ability of simple, rules-based systems to protect investors from large drawdowns, we believe our robo-advisor delivers a compelling value-proposition:

We seek to deliver an affordable, active, globally diversified, downside-protected, asset allocation solution.

In the investing world, ultimately you are on your own to understand how to best position yourself for long-term success. There is risk in relying on the perceived judgment and/or discretion of others. That’s why we encourage investors to do their own homework and review the evidence so they can understand how and why we invest using the systems and strategies we use. As we stated earlier, we are radically transparent and our mission is to empower investors through education. We’re here to help and find win-wins. If you don’t believe in and agree with the evidence we can share with you, then you are free to go elsewhere. Again, our passive robo competitors are a reasonable alternative.

Also, if you are a forward-looking advisor, and want to deliver an affordable solution for your clients, who have unique needs and unique goals, we can help you build your own white-label robo-advisor (passive, active, or anything in between). As we said up front, we don’t claim to have a monopoly on great ideas, but we believe in helping the financial service industry move into the 21st century.

Bottom line: If we can help facilitate a better financial service industry in the future, we’re in. Contact us and we’ll chat.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.