We believe deeply in the value philosophy as first described by Ben Graham: view stocks as ownership in a firm; buy with a margin of safety; avoid stories; think independently; and so forth.

In fact, I was so intellectually stimulated by value investing I wrote my dissertation on the subject, co-authored an entire book on value investing, and we’ve written numerous blog posts highlighting why value investing is compelling for long-term investors. I still follow my favorite value-focused blogs: OldSchoolValue, ValueWalk, Musing on Markets, BaseHitInvesting, etc.

We are fans.

But I’m not the only fan. The chorus of value cheerleaders, many of whom have been shellacked recently and who have value products to promote, seems to be growing louder.

For example, I just returned from the Morningstar ETF conference in Chicago, and most of the speakers talked up the opportunity in value:

Value is cheap relative to growth.Value is due for a good run.Low volatility is too expensive, but value spreads are great.And so on…

RAFI has probably told the most sophisticated story for a value rebound: see here, here, and here. The financial press is also contributing to the story. For instance, here’s a recent article that claims the “growth style [is] now in its ninth year of relative outperformance,” and offers some reasons why value investing may be poised for outperformance. Here’s another piece that suggests, “Value investing is rebounding.”

But is value going to rebound?

One of our intellectual mentors is Charlie Munger, and Charlie advises that in forming our views we should seek to, “Invert, always invert.” As Munger implies, sometimes when we re-frame a concept, we can gain new insights by thinking about it from a different perspective. Let’s give it a whirl…

- Current frame: Why might value rally?

- New frame: Why might value NOT rally?

Investing in value is a terrible idea

Mean reversion in a mean-reverting investing strategy sounds great, since we are value investors and we’d love to stop looking like idiots. But perhaps we shouldn’t discount the fact that there is a high probability we actually are idiots and promoting value at these levels is akin to promoting Bacardi 151 at an Alcoholics Anonymous meeting.

So are we buying a falling knife?

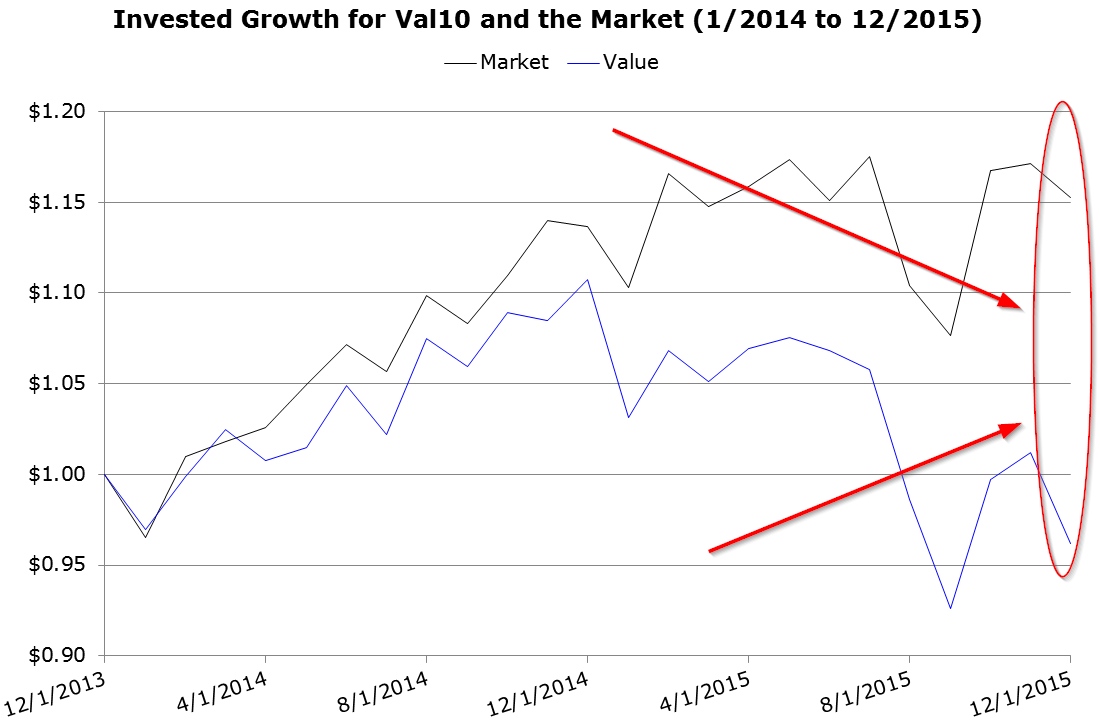

Value is certainly interesting because the strategy has gotten crushed. Here is a piece where we highlight this fact and here is the associated figure which compares the performance of the generic market (e.g., S&P 500), and Val10 (top decile b/m).

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Bottom line: The market has beaten generic value by over 19 percentage points from 1/2014 to 12/2015!

Just how good or bad is a 19 percentage point drag on the index?

According to conventional wisdom, if value has performed badly recently, then it is likely to perform better in the near future.

But what does it mean to say value has performed badly? How one measures if “value has worked” can be heavily influenced by the researcher. For example, are they looking at long/short HML-like portfolios? What valuation metric are they looking at? Equal-weight or market-cap weight construction? And so forth.

As with the 2-year invested growth chart above for value during 2014 and 2015, we’re going to keep this simple: long-only, market-cap weighted, sorted on B/M, using publicly available data so anyone can do the calculations on their own.

To calculate relative performance for value and the broad market we snag data from Ken French’s website:

- VAL_10 = Top Decile market-weighted value portfolio (Data). Our long-only “value portfolio.”

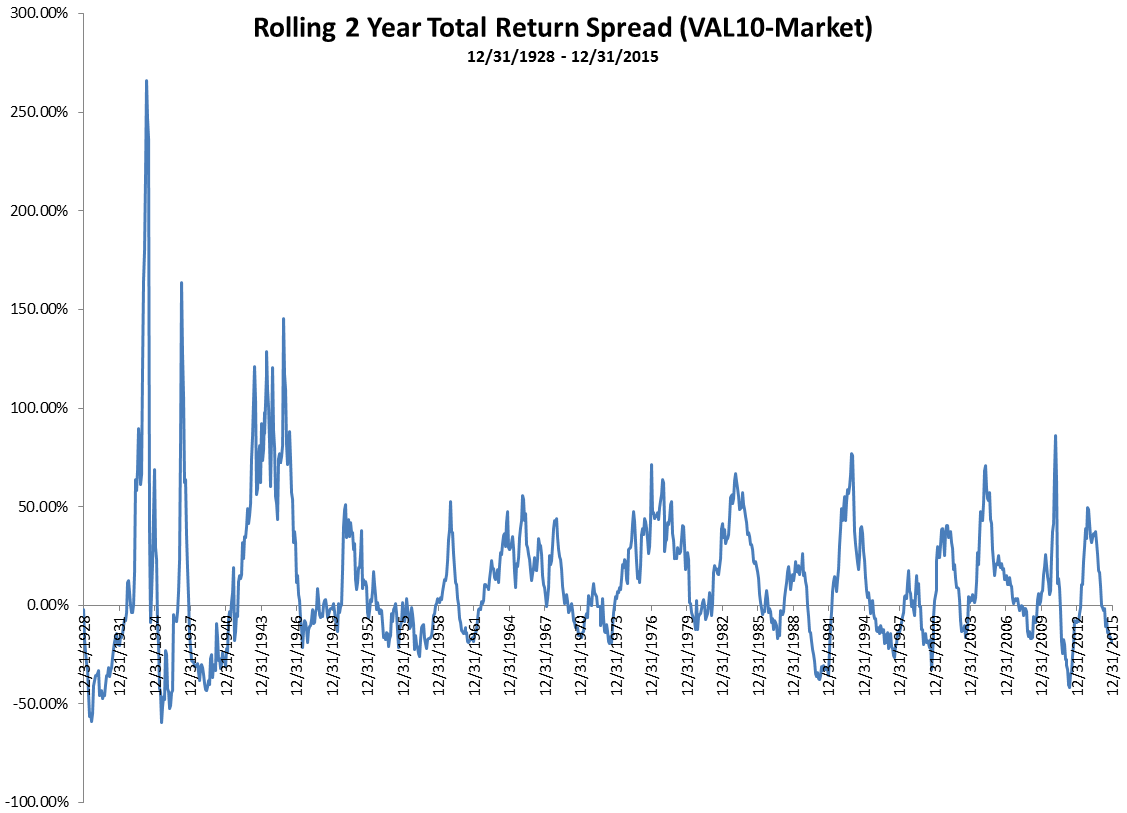

Val_10 has eaten a lot of pain the past 2 years. As highlighted earlier, from 1/1/2014 to 12/31/2015 the 2-year total return spread between Val_10 and the generic market is over 19%.

But just how “bad” is this, in a historical context? While 19 percentage points of underperformance over 2 years is a pretty painful run, is it such a rare occurrence that we should be confident that the pain simply can’t continue?

So should we listen to those singing the siren song of factor timing? Go all-in on value?

Here is a chart that looks at rolling 2-year total long-only return spreads between value and the market from 1929 to 2015:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Given this extended backdrop, the recent spread of -19% does not look especially out of the ordinary. 2-year spreads have been this bad, or worse, on many occasions in the past. In fact, with a generic deep value portfolio, one can expect to be trailing by 20 percentage points — or more — around 12% of the time. One can expect to be eating 10 points versus the index over a quarter of the time.

Life sucks as a value investor. In fact, value investing has been digging manager graveyards for over 100 years!

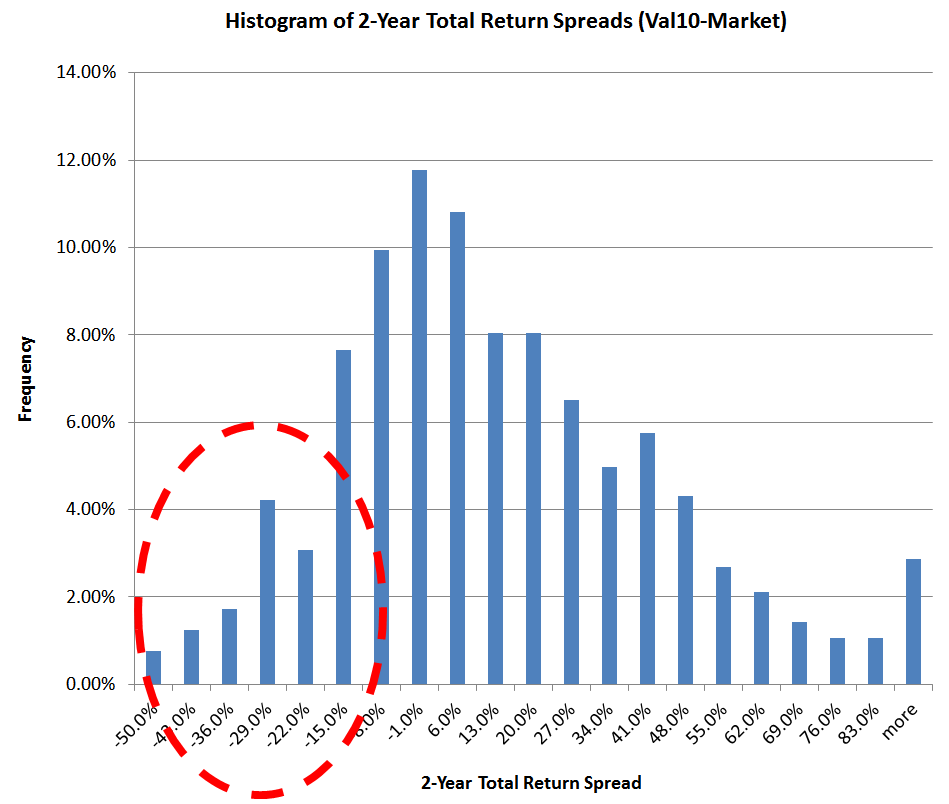

Here is the histogram of the value-market 2yr total return spreads:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

There is a lot of mass in the left tail of the distribution. And today, we’re not even very far out on the left tail!

Value can get a lot worse before it can get better

In short, value investing the past few years has been a bad experience, but things can get a lot worse before they can get better. Sadly, this is the lot of the value investor. Value investing is really a tragic story of pain, anguish, and heartbreak that never really has a happy ending. The expected gains are almost always offset with extreme relative performance pain. For instance, we asked here if investors were prepared for 6 years of tragic underperformance. But why stop there? Cliff Asness traded a live value strategy and lived through a 50%+ drawdown in the late 90’s when the market was cranking out 30% CAGRs. To say that Asness had brass balls would be an understatement–he had diamond crusted platinum balls (or as a reader suggested, diamond crusted tungsten carbide balls)!

Value investing is quite possibly the worst decision you will ever make — even at the current relative spreads. The pain will be unbearable and you will be forced to sell. Therefore, value investing is quite possibly the worst idea…EVER.

Editor note: Value investing, for those who have not been scared off already, is only viable for those who have a nuanced grasp and appreciation for the sustainable active investing framework. Read it. Buy and hold. Embrace the suck. If you are brave enough to be a value investor, here is an outline of our approach.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.