We did a recent internal simulation study on the performance of cheap and expensive stocks based on a variety of valuation metrics.

We looked at all our favorites from our Journal of Portfolio Management paper, “Analyzing Valuation Measures: A Performance Horse Race over the Past 40 Years:“

- EBIT/TEV

- EBITDA/TEV

- B/M

- Gross Profits / TEV

- FCF / TEV

This value investing research is part of a larger academic paper, but I did want to highlight one aspect of our study that we thought more practitioner-minded readers would find fascinating.

Note: We focus our results on EBIT/TEV because it is our preferred measure for identifying “cheapness.” The results for other valuation metrics are quantitatively similar.

A PDF version of this is available here.

How Does Our Simulation on Cheap and Expensive Stocks Work?

First, break stocks down into different valuation deciles from 1963 to 2013 based on EBIT/TEV (we only focus on US mid/large cap to avoid weird micro/small cap outlier effects).

- For example, if there are 1000 stocks, stocks 1-100 go in the first decile; stocks 101-200 go in the second decile, etc.

Next, do 1000 simulations of random 30 stock portfolios drawn from the cheap stock decile or the expensive stock decile.

- For example, simulation #1 draws 30 random stocks each month from the top and bottom decile from 1963 to 2013. This is the rough equivalent of saying, “we are going to have a monkey throw 30 darts,” every month during the 50 year period, to establish in each month separate 30 stock portfolios. Once our monkey has thrown his 30 darts in each month, we will then have 600 separate monthly portfolios (12 months * 50 years) and will have made 18,000 (30 stocks * 600 months) individual stock picks. This represents one simulation. We do 1000 simulations for the top decile and 1000 simulations for the lowest decile.

Calculate the performance statistics for each simulated strategy from 1963 to 2013.

Each simulated strategy represents the returns a value-investing monkey (cheap stock buyer) or growth-investing monkey (expensive stock buyer) would achieve over the full time period. We calculate compound annual growth rates (CAGR), standard deviation, and maximum drawdown.

Tabulate the performance statistics for all 1000 simulations.

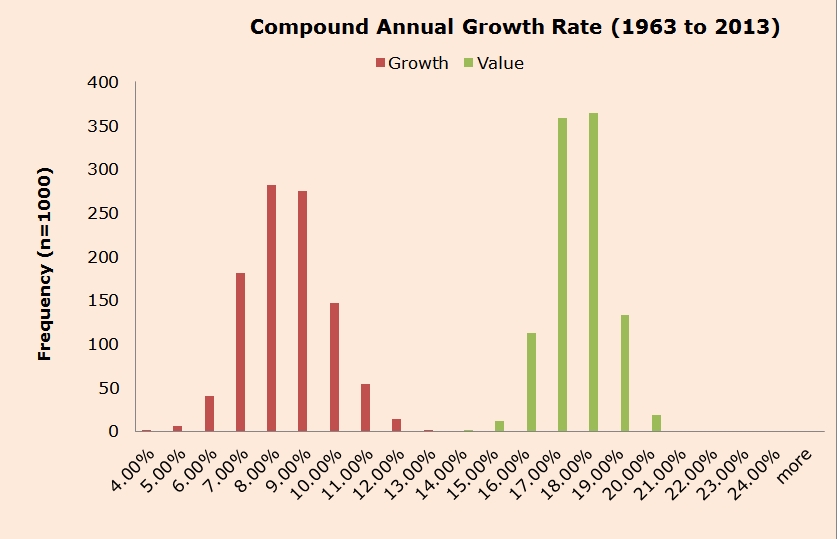

What Do the Returns to Value and Growth Stocks Look Like?

First, let’s look at the distribution of CAGRs (compound annual growth rates). Notice that there isn’t even a POSSIBILITY of a 30 stock portfolio of expensive stocks beating a portfolio of 30 cheap stocks. This is actually amazing. Typically, when you run a simulation with 1000 runs, you get overlap in the “tails,” or extreme ends of the distribution.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Clearly, buying expensive stocks is dangerous to one’s absolute returns.

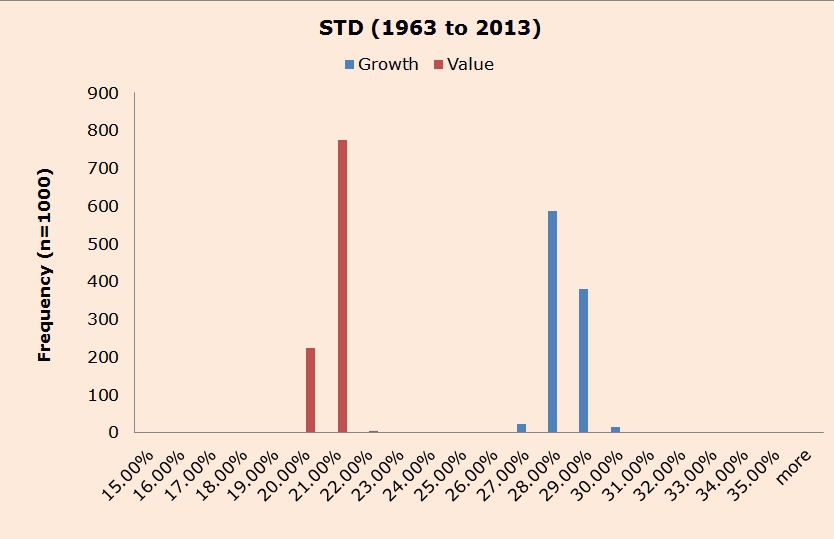

What Do the Risks to Value and Growth Look Like?

Volatility

The results above show that cheap stocks beats expensive stocks. But let’s look at standard deviations of the portfolios from our dart-throwing monkeys.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

First, you’ll notice that standard deviations are tightly bound, even across 1000 simulations. The histograms show another remarkable finding. No matter how you cut it, holding baskets of expensive stocks means more volatility–at least historically.

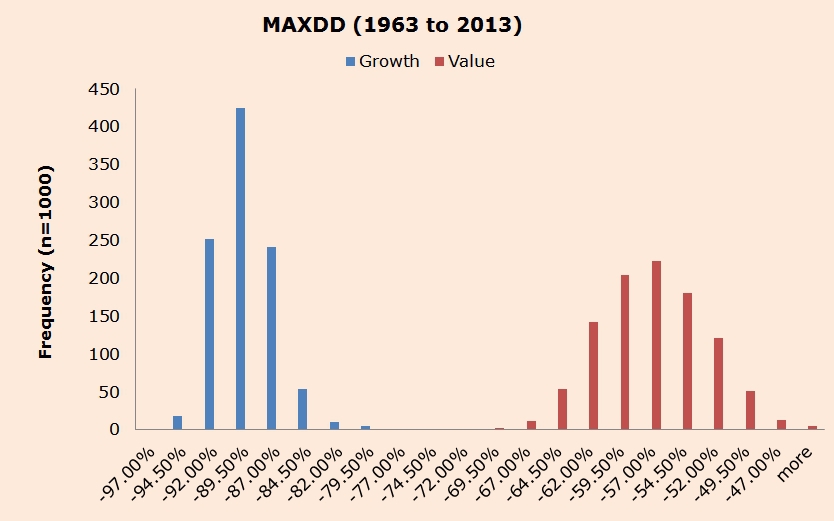

Maximum Drawdowns

Finally, what about maximum drawdowns associated with cheap and expensive stocks?

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

The evidence above suggests that cheap stocks protect the downside better than expensive stocks. The big drawdowns for value come in the 2008 Financial Crisis, whereas for growth, the largest drawdowns can come from the Internet Bubble burst or the 2008 Financial Crisis, depending on the simulation run.

Important to note, all strategies involve some massive volatility and stomach churning losses. Equity investing is NOT FOR THE FAINT OF HEART!

There is simply no way to “avoid drawdowns” when investing in equity.

Conclusions on cheap vs expensive stocks

One can’t even simulate a scenario where a diversified portfolio of the best performing 30 expensive stocks can beat the worst performing portfolio of 30 cheap stocks.

Why do investors allocate to expensive, or “growth,” stocks?

Margin of safety is the only investing rule that matters.

Stay cheap and be sure to review our best attempt at building a quantitative value investing system.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.