Near the end of 2021, I wrote an article noting that value portfolios looked historically cheap based on valuation spreads. I found that in the next five years (after the peak), Value investing performed quite well.(1)

Following this post, I have received numerous questions related to the following question:

How did Momentum investing perform after the previous two valuation peaks?

This article answers this question.

Key finding: Momentum investing also performed well following episodes when value stocks were cheap. Of course, momentum portfolios did not perform nearly as well as value portfolios, but they did still beat the generic market.

We dig into the details below.

Current Valuation Spreads

Our website has a tool, the Visual Value Factors module, that allows individuals to see how cheap/expensive Value portfolios are on various measures.

What does our tool say about current valuations?

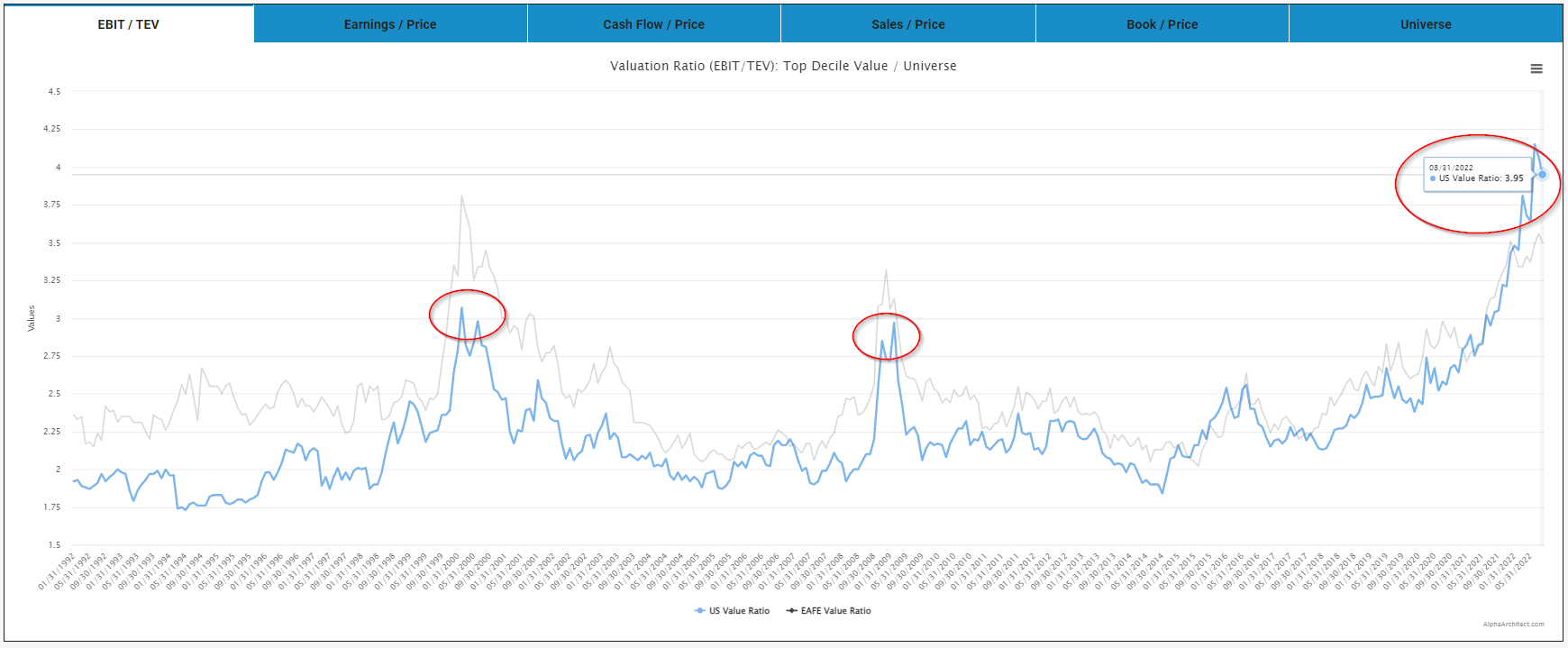

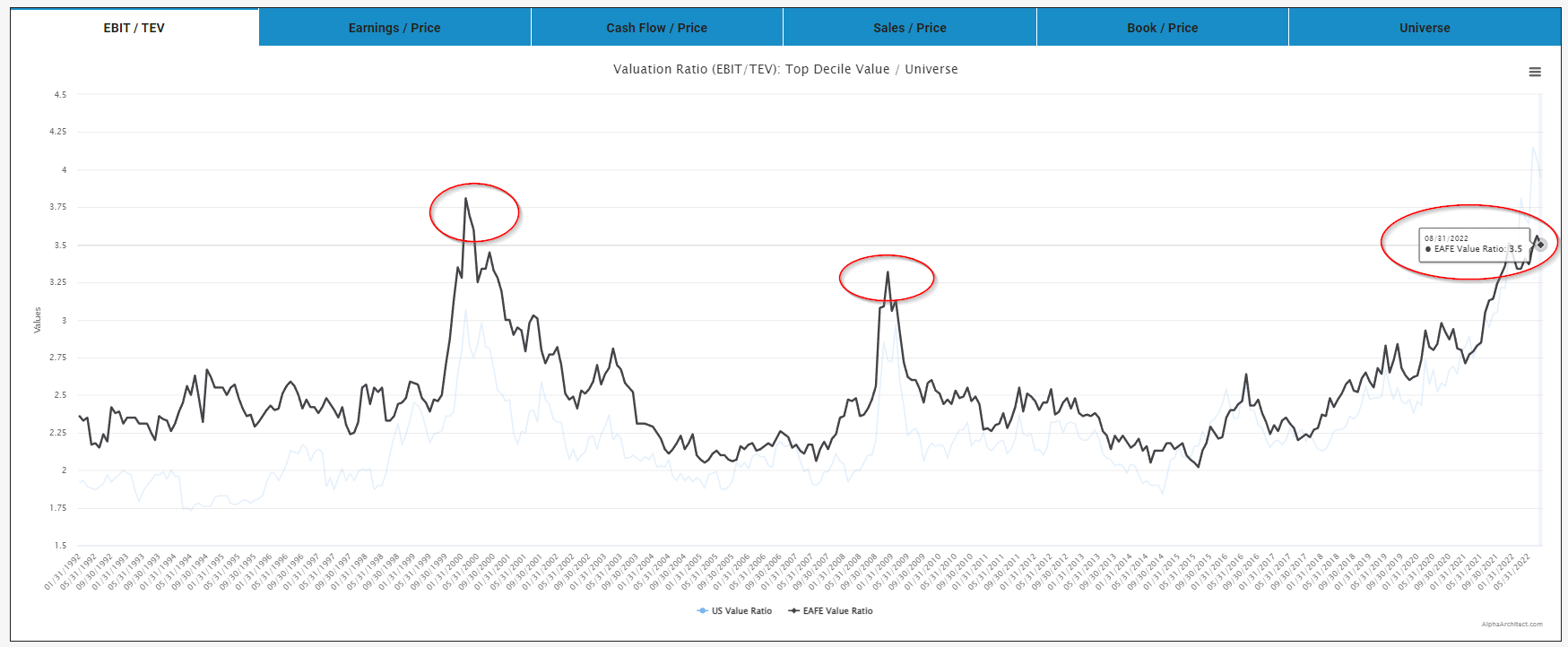

We use EBIT/TEV (our preferred valuation measure) to see how cheap/expensive a Value portfolio formed on EBIT/TEV is compared to the market.

U.S. Market:

International Developed Markets:

We note a few things:

- The two prior peaks were near 12/31/1999 and 12/31/2008

- Current spreads are as high (International) or higher (U.S.) than the past valuation peaks.

- Year-to-date, valuation spreads have not dropped significantly (in the U.S., on EBIT/TEV, it went up!).

These results are similar to AQR’s results.

So, let’s answer the question–How did Momentum investing perform after the previous two valuation peaks?

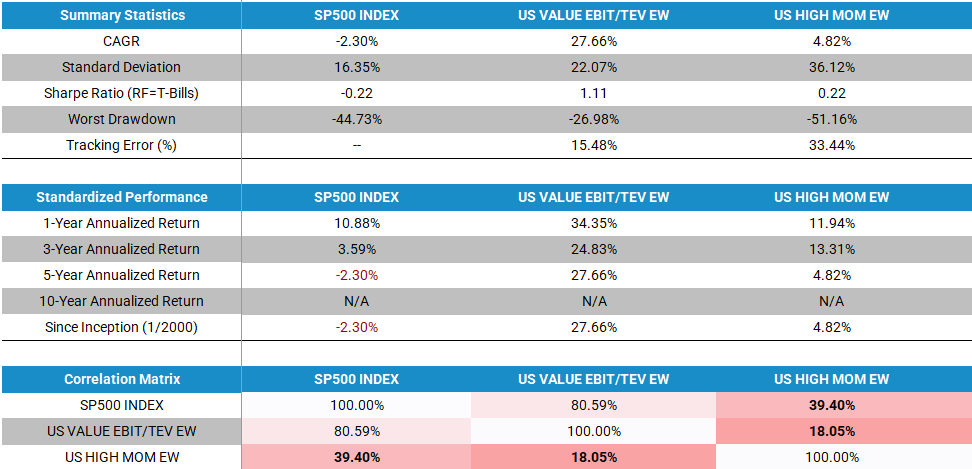

Momentum Investing from 1/1/2000-12/31/2004

We examine both a Momentum and a Value portfolio in the U.S. markets:

- The top decile on EBIT/TEV from our Factor Database (Value).

- The top decile on Momentum (12_2) from our Factor Database (Momentum).

The starting universe in either the U.S. or international markets is the 1,500 largest stocks in each market. So the top decile is a portfolio of ~ 150 mid/large-cap stocks. For the main results, the portfolios are equal-weighted.(2)

Below are the returns against the S&P 500 index. All returns are gross of any fees or transaction costs. Our value portfolios here are equal-weighted.

1/1/2000-12/31/2004 U.S. market:

What about International markets?

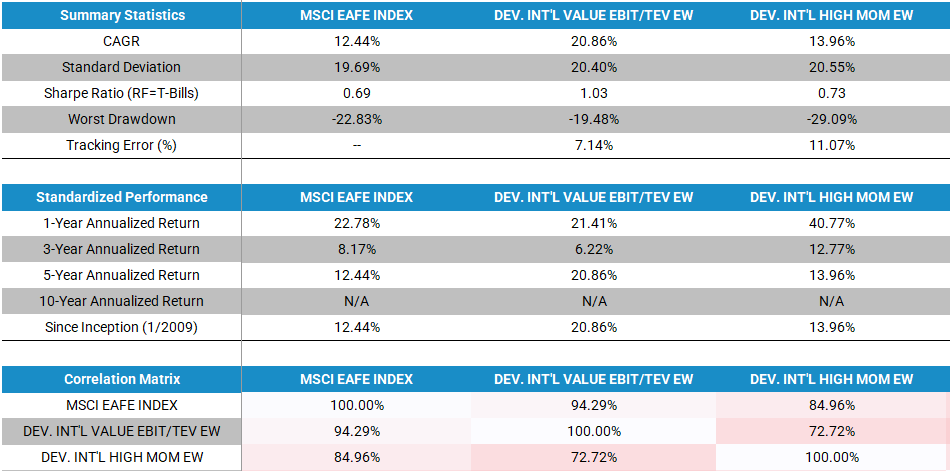

Below we perform the same exercise against the MSCI EAFE index. All returns are gross of any fees or transaction costs. Our value portfolios here are equal-weighted.

1/1/2000-12/31/2004 developed international markets:

In both markets, we find the following results:

- Momentum investing performed better than the market.

- Momentum investing did not perform as well as Value investing.

- Value and Momentum investing had very low correlations over this time period!

Let’s move on to the next valuation peak–12/31/2008.

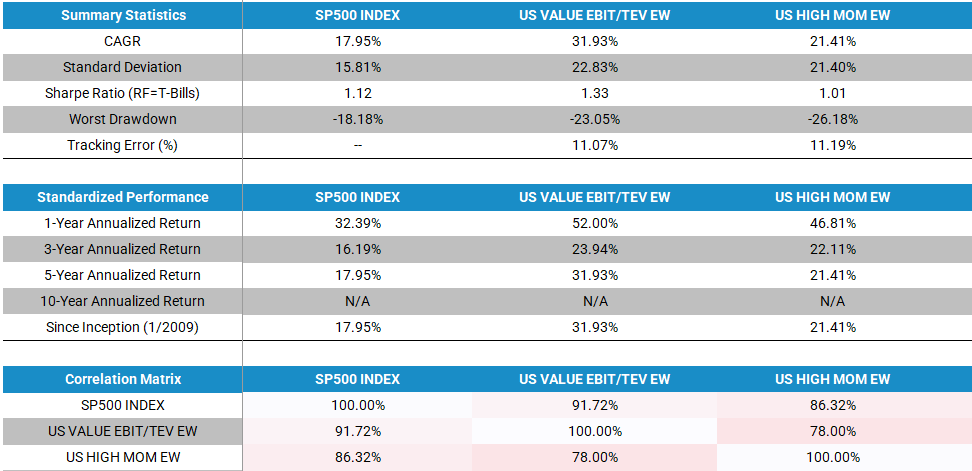

Momentum Investing from 1/1/2009-12/31/2013

We perform the same analysis over a new five-year stretch.

1/1/2009-12/31/2013 U.S. market:

1/1/2009-12/31/2013 developed international markets:

In both markets, we find the following results:

- Momentum investing performed better than the market.

- Momentum investing did not perform as well as Value investing.

- Value and Momentum investing had lower correlations than Momentum and the market portfolio.

Conclusions on Momentum Investing and Valuation Peaks

With the caveat that no one can predict the future, this article outlines how Momentum Investing did after the prior two valuation peaks.

As shown above, the five years after valuation peaks were decent times to be a Momentum investor. These results also highlight the portfolio benefits of combining Value and Momentum investing as seen through the low correlations between Value and Momentum portfolios.

References[+]

| ↑1 | Of course, nothing is guaranteed in the future |

|---|---|

| ↑2 | Below is where one can find this data on our website:

https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-200x64.png 200w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-400x129.png 400w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-600x193.png 600w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-800x258.png 800w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-1200x387.png 1200w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-1536x495.png 1536w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4.png 1645w" sizes="(max-width: 1645px) 100vw, 1645px" /> https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-200x64.png 200w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-400x129.png 400w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-600x193.png 600w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-800x258.png 800w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-1200x387.png 1200w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4-1536x495.png 1536w, https://alphaarchitect.com/wp-content/uploads/2021/12/value.five_.year_.stretch.4.png 1645w" sizes="(max-width: 1645px) 100vw, 1645px" /> |

About the Author: Jack Vogel, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.