Financial crime is often treated as a matter of enforcement. People break rules, courts prosecute, and regulators respond. But in reality, financial crime can also reflect financial pressure. Some individuals face weak balance sheets, poor debt management and limited savings, and stronger incentives to misuse money placed in their trust. This paper introduces a new perspective: financial literacy is not just about better household decisions. In fact, it may also reduce the likelihood that individuals commit financial crimes.

Financial literacy and financial crime: A regression discontinuity approach

- Paul G. Freed, John Hackney

- Journal of Financial Economics, 2026

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

Financial literacy reduces financial crime

The paper finds that mandatory high school financial education in Virginia significantly reduces the probability of being charged with a financial crime. Using a regression discontinuity design around the class-cohort cutoff, the authors estimate a decline of roughly 32% to 37% relative to the mean. The effect persists for at least six years after the treatment.

The effect is concentrated in embezzlement

The reduction is strongest for embezzlement, the type of financial crime most closely associated with financial stress and misuse of entrusted funds. The paper does not find comparable effects for fraud, forgery, or counterfeiting. This suggests that financial literacy changes behavior most when financial pressure is a key motive.

Financial literacy does not reduce all crime

The authors find no meaningful effect on violent crime, drug-related crime, vandalism, or other non-financial crimes. This is important because it shows that the course is not simply reducing criminal behavior broadly. The effect appears specific to financially motivated misconduct.

Low-income areas benefit the most

The reduction in financial crime is concentrated among individuals living in low-income neighborhoods. Treated individuals in these areas experience a 42% to 48% decline in the likelihood of committing financial crime relative to those in higher-income areas. This supports the idea that financial constraints are central to the mechanism.

Financial education improves balance sheets

Using Census survey data, the paper shows that treated individuals reduce reliance on credit card debt, increase investment, and are more likely to maintain savings accounts. These changes point to stronger personal finances. Better financial habits may reduce the need or temptation to misuse funds.

Treated defendants appear less financially distressed

Among individuals who are eventually charged with financial crime, those exposed to financial literacy education are less likely to rely on public defenders or self-representation. This suggests that the intervention reduces the share of financially distressed individuals among financial crime defendants. The evidence reinforces the financial-constraints channel.

The results are not driven by avoidance or migration

The authors test whether treated individuals simply become better at hiding crimes, move out of Virginia, or select into different jobs or schools. They find little evidence for these alternative explanations. Suspicious Activity Reports and police incident data also decline, suggesting actual financial crime falls rather than merely becoming harder to detect.

Practical Applications for Investment Advisors

Treat financial literacy as risk prevention

Financial education does more than improve budgeting or investing. It can reduce downstream risks linked to financial stress, poor debt management, and weak household balance sheets.

Focus on financially constrained households

The strongest effects appear among individuals in low-income areas. Educational interventions may be especially valuable for clients or communities facing liquidity pressure, limited savings, or high-cost debt.

Connect education to behavior, not just knowledge

The paper shows that financial literacy affects real decisions: credit card use, savings, and investment behavior. Advisors should emphasize practical implementation rather than abstract financial concepts alone.

Recognize broader social benefits

Financial literacy may create positive spillovers beyond the individual. Better household financial management can reduce harm to employers, small businesses, and communities exposed to financial misconduct.

How to Explain This to Clients

“Financial literacy is often described as a way to help people budget, save, and invest. But this paper shows it may do something even broader. When people understand credit, saving, and basic financial planning, they may be less likely to end up under severe financial pressure. That matters because some financial crimes, especially embezzlement, often arise when people face money problems they feel they cannot share. So financial education is not just about building wealth. It can also reduce harmful financial behavior.”

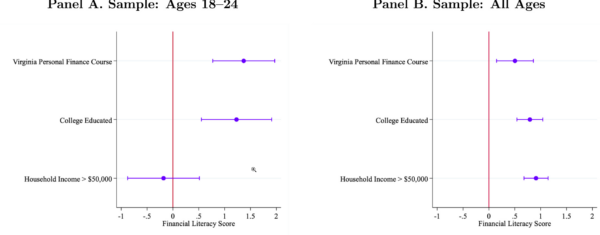

The Most Important Chart from the Paper

This figure illustrates the relative predictive power of taking the high school financial literacy course on tested financial literacy metrics for different age groups. The sample data is from the FINRA National Financial Capability Study (NFCS) surveys.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

This study investigates how financial literacy shapes the propensity of individuals to commit financial crime. Using state-level administrative data on criminal charges linked to comprehensive public records , we exploit a policy-based discontinuity in grade level assignment based on individual birth dates that exogenously requires certain high school cohorts to attend a financial literacy course. Our estimates suggest that exposure to the course reduces the propensity to commit financial crime by 37%. The reduction is driven by declines in embezzlement and is stronger for low-income individuals. Additional evidence suggests that the reductions are primarily explained by improvements in household balance sheets.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.