Absolute Momentum: A Simple Rule-Based Strategy and Universal Trend-Following Overlay

- Gary Antonacci

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our free Academic Alpha Database!

Abstract:

There is a considerable body of research on relative strength price momentum but relatively little on absolute, time series momentum. In this paper, we explore the practical side of absolute momentum. We first explore its sole parameter – the formation, or look back, period. We then examine the reward, risk, and correlation characteristics of absolute momentum applied to stocks, bonds, and real assets. We finally apply absolute momentum to a 60-40 stock/bond portfolio and a simple risk parity portfolio. We show that absolute momentum can effectively identify regime change and add significant value as an easy to implement, rule-based approach with many potential uses as both a stand- alone program and trend following overlay.

Data Sources:

Not disclosed; 1973-2012.

Alpha Highlight:

Strategy Summary:

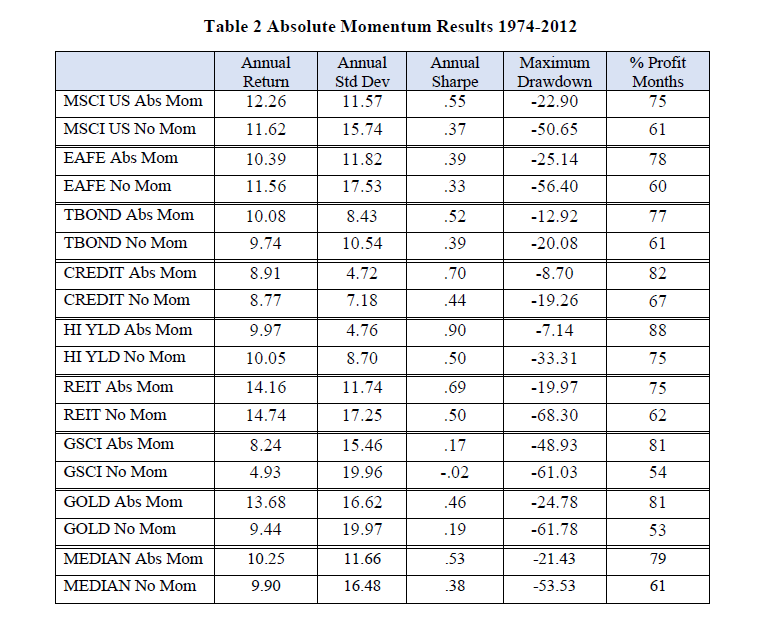

- Paper uses the following assets: MSCI US, MSCI EAFE, Barclays Capital Long U.S. Treasury, Intermediate U.S. Treasury, U.S. Credit, U.S. High Yield Corporate, U.S. Government & Credit, and U.S. Aggregate Bond indices, 90-day U.S. Treasury bills, FTSE NAREIT, S&P GSCI, and monthly gold returns

- Calculate the past 12-month momentum for each asset class using monthly excess returns, defined as the excess return above the Treasury Bill.

- If the asset momentum is positive, hold the asset for the next month. If the momentum is negative, switch into the 90-day U.S. Treasury Bill.

- Paper shows that adding this momentum overlay to a 60/40 portfolio adds significant value by reducing drawdowns.

- Paper also show this adds value when applied to a 5 asset portfolio (called the parity portfolio in the paper).

Commentary:

- Documents that adding a simple momentum overlay to each asset class adds significant value.

- Overall, is a valuable tool for any asset class.

- The strategy is highly related to the simple MA strategy.

- Empiritrage has a detailed report highlighting the comparison between this strategy and the MA strategy

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.