Day of the Week and the Cross-Section of Returns

- Justin Birru

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category.

Abstract:

This paper documents a new empirical fact. Long-short anomaly returns are strongly related to the day of the week. Anomalies for which the speculative leg is the short (long) leg experience the highest (lowest) strategy returns on Monday. The exact opposite pattern is observed on Fridays. The effects are large; Monday (Friday) alone accounts for over 100% of monthly returns for all anomalies examined for which the short (long) leg is the speculative leg. Consistent with a mispricing explanation, the pattern is fully driven by the speculative leg of the strategy. The observed patterns are consistent with the abundance of evidence in the psychology literature documenting that mood increases from Thursday to Friday and decreases on Monday.

Alpha Highlight:

Evidence from psychology suggests that “mood” can influence decision-making. For example, Wright and Bower (1992) find that forecasts are influenced by mood — good moods generate more optimist forecasts than bad moods. Researchers have found that mood, or sentiment, can influence financial decision making. For example, a negative emotional state has been found to induce irrational financial market behavior (Read: The Financial Costs of Sadness), and unpleasant weather affects our mood and leads to slower market reactions (DeHaan, Madsen and Piotroski, 2015).

This paper looks at how mood might be related to weekly trading patterns. The author first cites the psychological literature, which finds a mood pattern across day of the week:

- Mood increases from Thursday to Friday

- Mood decreases on Monday.

Anyone who has ever had a job understands this relationship. Mondays are a general drag, whereas Thursdays and Friday are more exciting because the weekend is closer!

But can mood affect weekly stock returns?

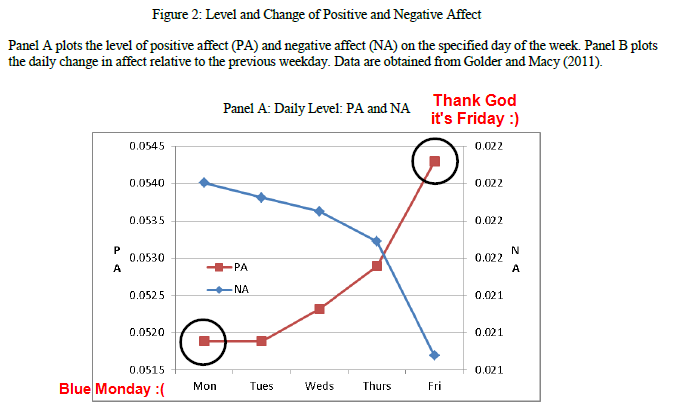

To address this question, the author first plots mood across the week using data from Golder and Macy (2011). The chart below highlights that positive feelings increase throughout the week and negative feelings decrease throughout the week. Clearly, people’s moods are affected by the day of the week.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

This paper finds two simple examples that support the idea that mood might affect financial markets:

- VIX shows an 2.16% average daily increase on Monday, and an -0.7% average daily decrease on Friday…thus, decreasing sentiment is associated with increases in VIX.

- The average returns on one-year Treasuries are nearly 4 times higher on Monday than on Fridays: Poor sentiment induces “flight to safety.”

Birru hypothesizes that sentiment-driven stock anomalies should exhibit return variation across days of the week in accordance with moods.

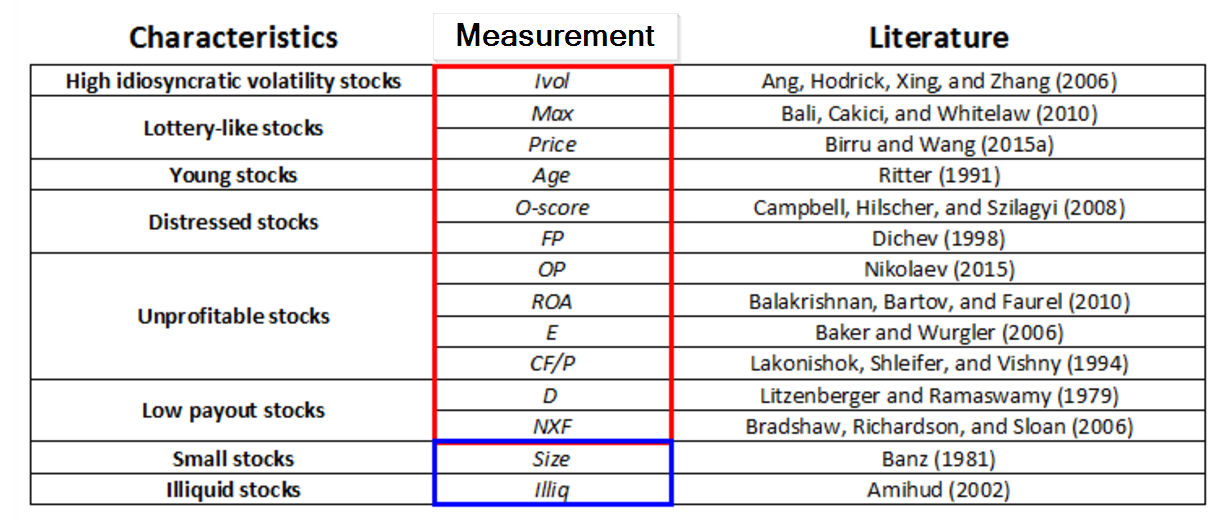

To test this hypothesis, he examines 14 long/short anomaly variables that are likely to be affected by investors’ mood changes. The sentiment-based abnormal returns should be attribute to the speculative leg, which is assumed to be the short leg of the long/short portfolio (in all cases except illiquidity and size (the short leg is the large-cap leg, which is less “speculative”)). For example, when looking at “age,” where the long leg is old stocks and the short leg is young stocks, it is assumed by the author that younger stocks are more affected by sentiment than old stocks.

Here are the anomalies examined (red = short leg is speculative; blue = long leg is speculative):

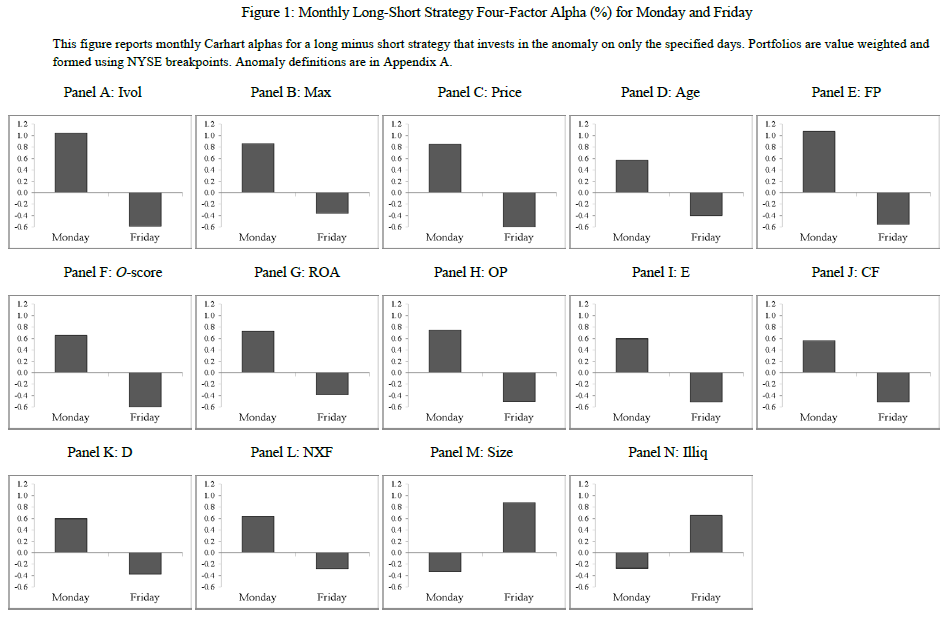

The below figure compares the monthly 4-factor alphas for the long-short anomalies on Monday and

Friday. We can see there’s a strong, predictable variation in the cross-section of returns across separate days of the week.

The results strongly support the “mood-driven” hypothesis:

- All anomalies, except size and illiquidity, have high returns on Monday. –> short leg is the speculative leg

- By contrast, size and illiquidity anomalies have high returns on Fridays. –> long leg is the speculative leg

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

This paper shows that this return pattern is robust to different sub-sample periods, and is not explained by other factors that could also explain this empirical pattern: 1) macroeconomic news releases, 2) firm-specific news releases, or 3) institutional trading.

Conclusion:

Mood swings across the week will affect the returns of speculative stocks. Specifically, L/S anomalous portfolios for which the speculative leg is the short (long) leg experience the highest (lowest) strategy returns on Monday. The exact opposite pattern is observed on Fridays.

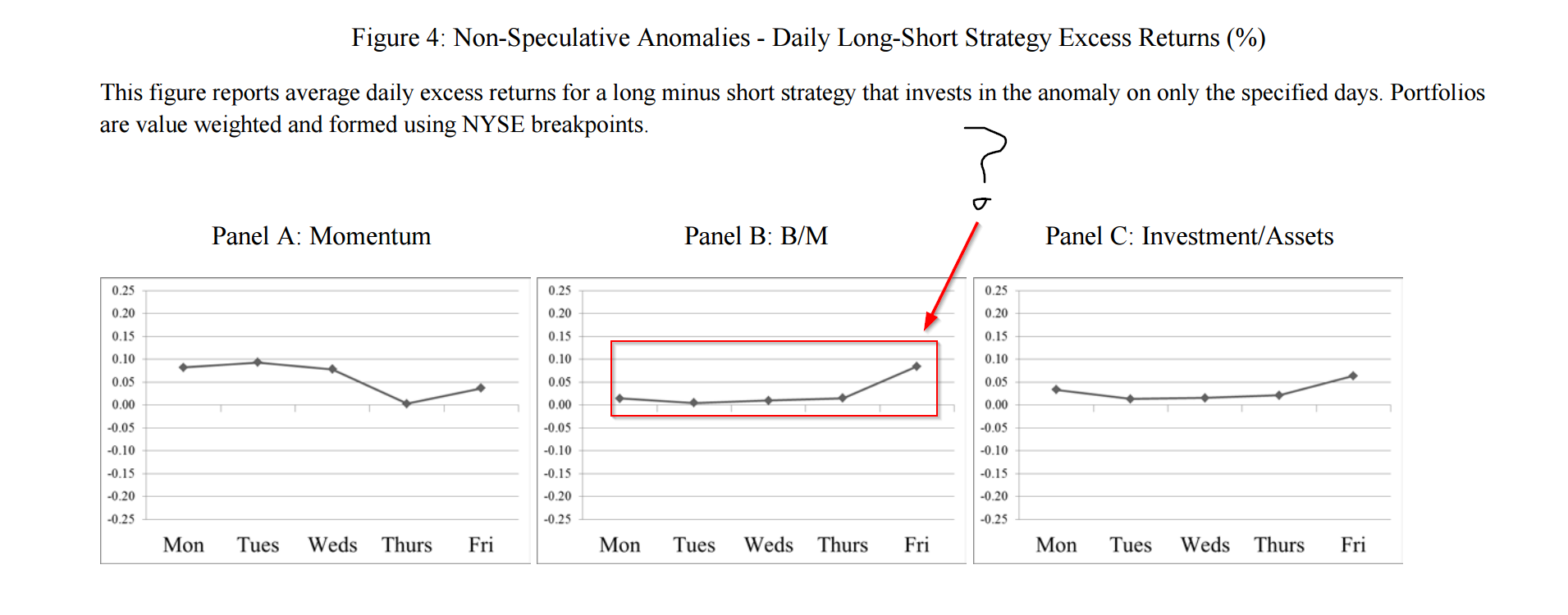

One aspect I really can’t understand is why “value” is not considered a “sentiment” driven anomaly. I would expect that the short leg (the expensive growth stocks) would be related to mood and speculation more than the long leg — the author doesn’t find this. The relationship is fairly flat, with a upward move on Friday. Weird.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

This paper is also related to a new Journal of Finance article called, “Return Seasonalities.” The finance literature is really getting hot and heavy on seasonality effects that move beyond January. About time…

Sounds like a job for a systematic approach!

When investing in financial markets, always ask yourself if you are Trying Too Hard? Behavioral bias is everywhere…

Editor’s note:

The author reached out with some feedback regarding our comment on “why “value” is not considered a “sentiment” driven anomaly.”

From Prof. Birru:

There is an explanation for this finding – which I briefly discuss in my paper, and is discussed in more detail in “Investor Sentiment and the Cross-Section of Returns” by Baker and Wurgler (2006). They similarly find that the B/M anomaly does not exhibit returns that are correlated with sentiment. In other words, they do not find evidence that growth stocks are more speculative than value stocks. It is intuitive to think that growth stocks are speculative stocks, but Baker and Wurgler (2006) point out that value stocks are also speculative because value stocks (high B/M) include some firms that are distressed, and distressed firms are particularly speculative. They argue that because both growth stocks and value stocks are speculative, both groups of stocks will have a similar sensitivity to sentiment, and therefore the return difference between growth and value stocks will not be sensitive to sentiment. The lack of a relationship between the B/M anomaly and day of the week is consistent with their interpretation and with their empirical findings.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.