A few years ago, the profitability “quality” factor was originally proposed by Robert Novy-Marx. Here is a snippet from the abstract of the paper:

Profitability, measured by gross profits-to-assets, has roughly the same power as book-to-market predicting the cross-section of average returns. Profitable firms generate significantly higher returns than unprofitable firms, despite having significantly higher valuation ratios. Controlling for profitability also dramatically increases the performance of value strategies, especially among the largest, most liquid stocks.

Rhetorical question: Who doesn’t want to buy “profitable” companies? Since that paper, many fund families have added the “quality” factor to their arsenal of mutual funds and ETFs to sell. Fama and French have even added a “quality factor” to their five-factor model.

So if quality is already well-established, how does this new paper, “The Trend in Firm Profitability and the Cross Section of Stock Returns,” add to the conversation?

As opposed to simply examining the cross-sectional profitability of the firm, this paper examines the cross-sectional trend in profitability. So if we are standing at 12/31 and wanted to form a portfolio of the top 10% of firms, this paper ranks on the past trend in profitability (as opposed to the firm’s current profitability).

The portfolio construction and results

The paper first creates the profitability variable similar to Novy-Marx, which is defined as the quarterly gross profits equals the quarterly sales minus the quarterly COGS scaled by total assets. The paper determines the trend of the profits through a regression (page 13 of the paper) that accounts for seasonality.

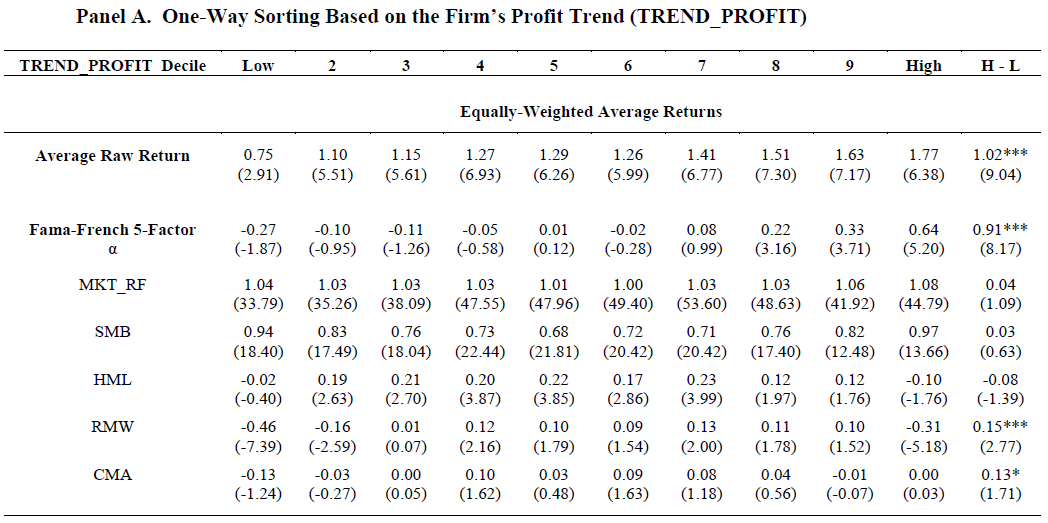

The paper first splits the universe of stocks into deciles based on how firms rank on their profit trend variable. The results are shown in Table 3 of the paper.

Panel A of Table 3 (shown below) highlights the results to equal-weighted portfolios sorted on the profit trend variable. Examining both the raw and the FF 5-factor alpha, there is a strong and significant effect (T-stats of 8 and above) whereby the firms with higher profit trends have higher future returns compared to stocks with lower profit trends (as shown when examining the High minus Low portfolio). It should be noted that the returns are not as large when value-weighting the portfolio, highlighting that this effect is more prominent in smaller stocks (Panel A of Table 3).

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

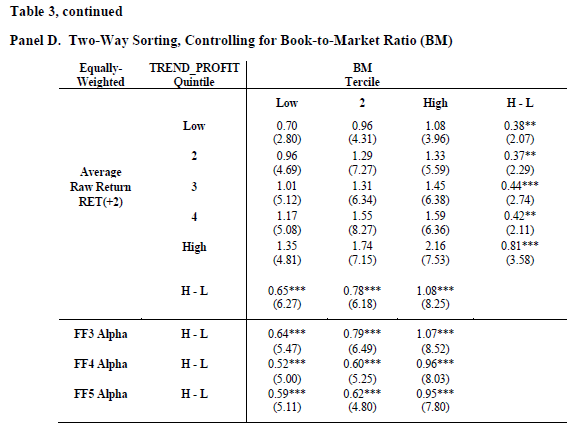

Next, the paper examines the question of how the profit trend variable interacts with other factors by creating double sort portfolios. This is Shown in Panels B through E of Table 3 in the paper. The variables examined are Profits (Panel B), Size (Panel C), Book/Market (Panel D), and Momentum (Panel E). Below is Panel D of Table 3, where the portfolio is first sorted on B/M (Low are Growth firms and High are Value firms) and then on the profit trend variable. Within the three B/M terciles, the profit trend is predictive of future returns (examining the H-L portfolio).

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

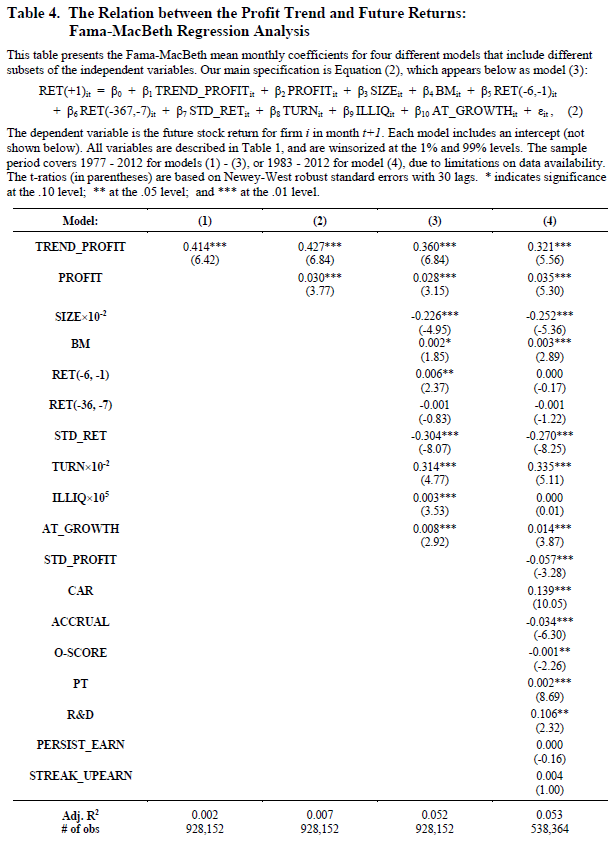

Next, the paper runs the results through a ton of robustness tests. I will simply highlight Table 4 (below), where the paper uses a Fama-MacBeth regression. As can bee seen in column 4, even after accounting for 17 known variables with return predictability, the profit trend variable is still significant.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

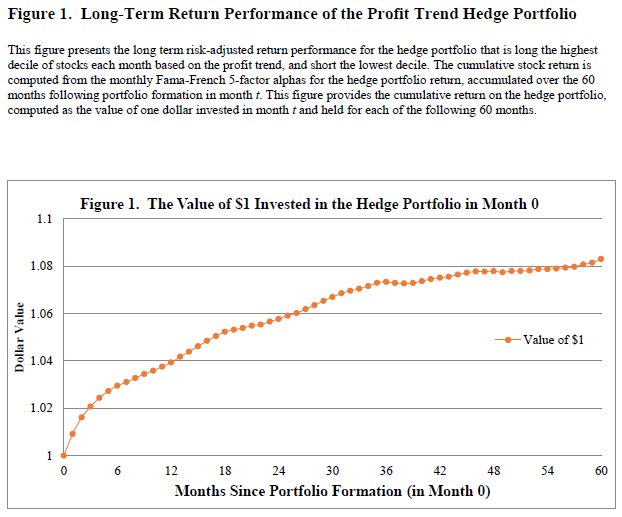

Last, the authors attempt to explain the results. Are investors investing in riskier stocks or are behavioral errors being made? The paper examines the long-run returns to the L/S portfolio and graphs the cumulative returns in Figure 1 (below). Figure 1 highlights that there is a steady upward slope (positive returns) over the first 2 years, and the returns flatten out thereafter. This implies investors may be under-reacting to news about the firm. Since there is no regression a few years out, the authors conclude there is no over-reaction.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

So what are we to make of these results?

It appears that investors are under-reacting to news! Specifically, investors are under-reacting to the past profit trend of each firm. Within Value and Momentum stocks (Panels D and E of Table 3), firms with higher past profit trend have higher returns than firms with lower past profit trends. In our Quantititive Value process, we already have a form of this idea baked into the quality score. In a recent post, we also examined the momentum of fundamentals, which is related to the idea in this paper.

Big idea — investors appear to under-react to the trend of the profits!

The Trend in Firm Profitability and the Cross Section of Stock Returns

- Ferhat Akbas, Chao Jiang, and Paul D. Koch

- A version of the paper can be found here.

Abstract:

This study shows that the recent trajectory of a firm’s profits predicts future profitability and stock returns. The predictive information contained in the trend of profitability is not subsumed by the level of profitability, earnings momentum, or other well-known determinants of stock returns. The profit trend also predicts the earnings surprise one quarter later, and analyst forecast errors over the following twelve months, suggesting that sophisticated investors underreact to the information in the profit trend. On the other hand, we find no evidence of investor overreaction, and our results cannot be explained by well-known risk factors.

About the Author: Jack Vogel, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.