The opportunity to pursue a 1042 exchange sale can place business owners in a dilemma. The word means “a situation in which a difficult choice has to be made between two undesirable alternatives.” Look up the definition of dilemma and you might see a reference to Scylla and Charybdis − promontories that mark the troubled waters in the Strait of Messina.(1)

Strait of Messina

Homer tells us that Odysseus encountered these mythical sea monsters and opted to pass by Scylla, preferring to lose only a few of his sailors to the monster, rather than risk losing his entire ship in the whirlpool of Charybdis.

‘Is there no way,’ said I, ‘of escaping Charybdis, and at the same time keeping Scylla off when she is trying to harm my men?’(2)

This particular Greek dilemma is what came to mind when I first encountered an ESOP. I observed that business owners who sold shares to an ESOP seemed, like Odysseus, to find themselves between a rock and a hard place. They could elect to pursue a 1042 exchange and bypass the Scylla of capital gains taxes, but in doing so they had to roll their sale proceeds into qualified replacement property. That path would likely lead to the Charybdis of Floating Rate Notes. These special ESOP bonds are the predominant 1042 exchange asset in the marketplace, a fact that belies their relative shortcomings as an investment asset.

Just how unattractive floating rate notes are, and why they became the default 1042 rollover strategy among financial advisors, is the subject of this article. However, unlike Odysseus, business owners seeking to implement 1042 exchanges have more affordable and transparent paths to navigate between a rock and a hard place. (You can read about one of them here).

Why does our quantitative research-focused firm, Alpha Architect, have insights into this relatively obscure corner of the investment universe?

Our navigation around these investment shoals started in 2013 with a simple question posed by one of our family office clients: What are the most effective 1042 exchange investments? Thus began our research into the most efficient strategies for capturing the after-tax value of a 1042 exchange. The outcome was surprising: We thought we’d seen every investment security under the sun. What we uncovered through our preliminary work proved puzzling to us and unsatisfactory to our client. Floating rate notes that are created for ESOPs have very long maturities, yet pay only miniscule coupons. We’ve examined the prospectuses for many of these specialized floating rate notes, and they all have yields that on their face produce relatively unattractive investor economics.(3)

Let’s look at the recent JP Morgan ESOP note,(4) issued a few days before we published this article. Upon issuance, this ESOP bond paid a floating coupon tied to LIBOR that yielded just 26 basis points. That’s about 1/4%!(5) Just as important, under current tax rates for top earners, interest from corporate bonds is taxed at a 40.8% rate. Therefore, QRP investors who purchase these bonds likely will enjoy an after tax yield of just 0.1539%, or less! That hardly seems an appropriate starting return for a 30-40 year investment horizon. By comparison, a non-QRP investor could purchase a risk-free 30-year US Treasury bond yielding 2.95% before taxes, more than a 10-fold increase in current yield over the JPMorgan paper.(6)

‘1042 Exchange’ Feature More Important than Yield

Why, one might ask, are FRN coupons so low? Who would buy such an instrument?

Readers of this article are not the only ones asking those questions. A structured products investor interviewed in the May 15, 2017, edition of Structured Product Daily—a Wall Street capital markets newsletter—said he did not like the coupon and the length of these notes, referring to the JPMorgan notes due May 20, 2052. ‘…this one makes absolutely no sense to me,’ he said. ‘Why would you want to hold something like that for 40 years and take a 40 bps haircut?’ (Read the article here.)

As it turns out, only business owners who sell their stock to an ESOP would buy them. That is because sellers who elect 1042 exchanges, like Odysseus, find themselves between a rock and a hard place. The IRS’ definitional constraints on QRP, combined with the functional needs of the purchaser, create investment criteria that are relatively narrow. The investment banks that hawk floating rate notes understand this dynamic and capitalize on this unusual client need when they structure such securities. They price ESOP bonds at a level that balances the often scant supply of floating rate notes with the demands of time-sensitive 1042 QRP purchasers.(7) But just because bankers are good at their jobs doesn’t mean investors have to settle for purchasing these bonds. We believe that business owners who invest in this 1042 QRP asset class face not only low yields, but also opaque fees, relatively high taxes and potentially significant constraints on the ability to realize their tax objectives.(8) These can all be avoided through more attractive 1042 exchange strategies, such as passive blue-chip equity alternatives. Here is a simple outline of our 1042 solution, for example.

Why Are ESOP Bonds Considered a Structured Product?

Readers might well wonder why an ESOP bond is referred to as a structured product in the trade journals. Weren’t structured products, like CMBS, CDOs and CLOs, blamed for precipitating and exacerbating the 2008 financial crises? We believe ESOP floating rate notes are considered structured products because, unlike conventional corporate bonds, these securities are designed to facilitate the highly customized risk-return objectives of the 1042 QRP investor.

Take for instance the assumption that 1042 exchange investors are more concerned with satisfying the IRS’s requirements for Qualified Replacement Property, which these bonds do, than with obtaining a market yield. All the yield in the world won’t help a purchaser if the IRS disqualifies the 1042 exchange, an outcome made possible by the fact that the purchaser must produce a notarized statement of purchase contemporaneously with his investment that identifies his securities and certifies their Code compliance. Or consider the unusually long maturity of these bond, designed to maximize the period of capital gains tax deferral in the 1042 exchange. Then there is the floating rate coupon and repayment option, which are features designed to isolate market fluctuations in interest rates and thus stabilize the bond’s value. The structure of these terms, which constitute economic trade-offs that are embedded in the ESOP bonds, is designed to attract QRP investors and enables the issuers to pay comparatively low interest rates. As capital markets veterans, we think of that low coupon as Wall Street’s way of helping itself and its corporate clients to a healthy share of the business owner’s tax-advantaged economics over time.

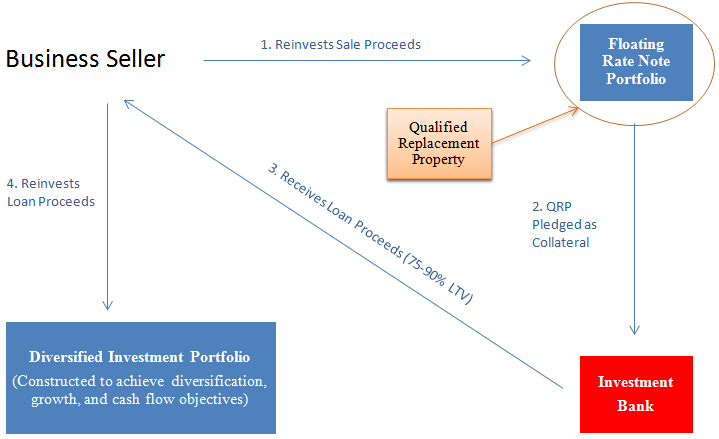

Nevertheless, many financial advisors counsel business owners to look past the bonds’ low yields in order to see the bigger opportunity to monetize their QRP investment. In monetization, the bonds are purchased by the selling shareholder as qualified replacement property and subsequently pledged back to the investment bank as collateral for a loan. The lending broker then lends the selling shareholder typically less than 90% of the value(9) of the investor’s FRN portfolio. Having thus “monetized” the qualified replacement property through this loan transaction, the selling shareholder is then free to invest the loan proceeds as desired.

The whole series of transactions typically looks like the following:

We feel this strategy introduces substantial complexity and often does not sit well with many investors. Consider that monetization of ESOP bonds tees up additional potential fee streams for the investment banks that sell floating rate notes.(10) The QRP purchaser who pays those fees may gain some flexibility, but at what cost? This financial detour adds complexity and fee-drag to an already low-yielding and tax inefficient 1042 exchange strategy. We can understand why investors might be frustrated by this situation.

Over-reliance on Floating Rate Notes a ‘Red Flag’

For these and other reasons we think that over-reliance on floating rate notes by ESOP formation advisors and their clients is a bad idea, and that there are better ways to complete a 1042 exchange. We are not alone in that view. The National Center for Employee Ownership (NCEO), perhaps the nation’s most widely respected source for unbiased information and research on ESOPs, recently published an article titled Red Flags in ESOP Transactions,(11) in which the authors call attention to the ‘Inappropriate Use of Floating Rate Notes’:

Floating rate notes (also called ESOP Notes) are long-term non-callable bonds often used as qualified replacement property for sellers selling to an ESOP. They allow the seller to meet the rules for tax deferrals under an ESOP. The issues with these notes are beyond the scope of this article, but they do not make sense for all sellers. Make sure you get advice from someone not selling the notes before proceeding…

At Alpha Architect, we believe that business owners electing 1042 exchanges should steer clear of sea monsters, whirlpools, rocks and other hard places. Instead, we urge investors to bear in mind the FACTS (Fees, Access, Complexity, Taxes and Search) when making an investment decision. Our experience suggests that the vast majority of taxable investors should focus on strategies with low costs, high liquidity, simple investment processes, high tax-efficiency, and limited due diligence requirements. For 1042 QRP, these would include passive solutions, especially passive equity strategies, which can be customized to maximize the benefits of the tax-deferral opportunity inherent in 1042 exchanges.

Our Firm is Technology-Enabled, but Investor-Oriented

Have questions? Reach out. We’ve spent quite a few years thinking about ways to help investors succeed, and we are always open to having a discussion and helping readers out. In fact, our firm mission is to empower investors through education. So help us accomplish our mission.

If you are interested in learning more about our 1042 exchange solutions, contact us (ask for Doug) and we will collaborate to build a win-win solution.

References[+]

| ↑1 | As a sailor and former naval officer, I made several memorable passages between these famous landmarks in the strait between Sicily and the ‘toe’ of Italy. |

|---|---|

| ↑2 | The Odyssey (Book XII), by Homer, written in 800 B.C.E |

| ↑3 | For example, our recent review of seven floating rate note prospectuses found online from issuers such as 3M, General Electric, Colgate Palmolive and UPS, revealed coupons at spreads under LIBOR that range from minus 25 bps to minus 35 bps. |

| ↑4 | Floating Rate Notes issued by JPMorgan Chase Financial Co LLC, due May 20, 2052 |

| ↑5 | The notes will pay interest at a rate of LIBOR multiplied by 0.66 minus 40 basis points. With LIBOR at 0.999% at the time of publishing, that coupon yield is calculated at 26 basis points. |

| ↑6 | Source: https://finance.yahoo.com/bonds accessed on June 5, 2017. |

| ↑7 | Purchasers of 1042 qualified replacement property are in a delicate position. They must identify and purchase the QRP within 12 months of receiving their sale proceeds from the ESOP trust. Without making an extraordinary effort themselves, for which they are unlikely to be qualified, the purchasers are unlikely to feel confident in selecting QRP securities on their own. They are therefore reliant on their experts to guide them. |

| ↑8 | Imagine your disappointment if, having intended to pass the wealth from the sale of your business to the next generation, you awoke in old age to learn that the ESOP bond you purchased for your qualified replacement property had been called for redemption by the issuer, or that you had outlived its maturity date. Don’t place yourself in the position of having to bet against your own longevity. Your choice of qualified replacement property should not require that you suffer an early demise in order to fulfill your estate planning goals! |

| ↑9 | Financial institutions lend against floating rate notes at a specified loan-to-value ratio (i.e., collateralization rate). The standard LTV rate is 90%. However, during the recent financial crisis, many lenders instituted all-in loan-to-value ratios that are lower, often in the 75% range. This is accomplished by specifying other required forms of liquid investor collateral to supplement the floating rate notes being provided. |

| ↑10 | The fees associated with floating rate note strategies might encompass (1) financing the ESOP transaction, (2) underwriting the FRN issuance, (3) selling the FRN to the investor as QRP, (4) lending to the investor against the FRN portfolio, (5) actively managing the investor’s wealth that stems from the QRP loan proceeds, and even (6) custodying and hypothecating the investors’ wealth management assets that are held in margin. The bank may even require the QRP investor to pledge his ESOP bonds to help collateralize the ESOP loan to the company whose stock he is selling. |

| ↑11 | Article accessed on May 9, 2017, at http://www.nceo.org/articles/red-flags-esop-transactions. |

About the Author: Doug Pugliese

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.