Have you been Ameritraded?

Millions of years’ worth of evolution have sharpened our brains to survive in the scam jungle of present day. Would you like a free car? How about a free mortgage? Act now and get a free kidney transplant! In our personal lives, our survival instincts kick in whenever we hear of a deal that sounds too good to be true. If it looks like a cobra, acts like a cobra, and sounds like a cobra, it’s probably a cobra. Even if we are wrong and the cobra is actually a stick on the ground, it was better to rely on our survival instincts and assume the worst.

Unfortunately, if you are a TD Ameritrade Advisor and purchased Vanguard ETFs on TD’s platform, you basically picked up the cobra, thinking it was a free stick. This week, you just took a cobra to the face.

TD Ameritrade recently announced that Vanguard, PowerShares, State Street, and others will no longer trade commission free on their Advisor platform (rumor is that this won’t happen until early 2018). Instead, they will carry a standard trading cost of $6.95 per trade. For small accounts and millennials looking to get started, those fees will bite (allocating a $1k into a model with seven Vanguard ETFs will now generate almost $49 in commissions, or a 4.9% sales load – see Kitces link below). Advisors who have cultivated a business on low cost (free) trading and small account sizes (new, future investors) have to revamp their allocation decisions and shoehorn new ETFs into their models, marketing materials, investment planning tools, and the like. Michael Kitces has a great video on the overall impact of this decision and what this means here.

But don’t worry…if you or your Advisor has recently been #Ameritraded, there are things you can do to ensure this never happens again. All advisors (and their clients) should focus on three key aspects of a trading platform:

- How does your trading platform make money?

- How can I accommodate small investors and build a meaningful relationship?

- And most importantly, what platform provides best-execution to my clients from a fiduciary perspective?

How does my platform get paid?

A professor of mine once said the following:

If you aren’t paying for the product…you are the product.

Like any other business, brokerage platforms are in the business of making money. In finance, trading securities has quickly become a commoditized business. Selling a share of Apple via Schwab, TD, or Vanguard has the same end result. You are buying a bushel of corn or a gallon of gasoline. In this context, platforms need to differentiate their services. Interactive Brokers is the low-cost leader, Fidelity is the higher-touch advisor-friendly platform, TD Ameritrade is (was) the Advisor-centric tech-integrated platform, etc.

The point here isn’t to advocate for one broker over another; however, all advisors should ask themselves how their platform is getting paid and what they need from their broker/custodian. If you can trade commission-free ETFs on a beautiful platform, with integrated reporting and client onboarding, all at no cost…you are probably in a less stable business model.

What this means is that the plain vanilla model for a broker to make money (charge commissions on trades placed) is replaced with deals like the following:

- Enter into agreement with an ETF provider. ETF Provider pays “listing fees” and offsets platform costs.

- Enter into Payment for Order Flow agreement with high-frequency trading firms (disclosed on SEC Form 606. Examples: TD Ameritrade, Schwab)

- Promote proprietary products (e.g., Schwab ETFs on Schwab platform) and use broker platform as a “gateway” to other products

Not that any of these arrangements are necessarily bad (more on that later), but it is certainly less stable and more opaque when your platform depends on a mosaic of relationships as opposed to a simple, clear business model. By attaching to “free,” or “flat fee” platforms, advisors should acknowledge that they take on additional risk by doing so.

Free stuff ain’t free.

So flat fee brokers and commission-free ETFs aren’t “free:” How can I serve small investors?

In this platform-centric world, the advisor now needs to ascertain how on earth they can service smaller clients (future big clients) and cultivate meaningful relationships. This need is where the allure of the commission-free ETF platform came to fruition:

Great! I can advise an account with $5,000, process $100 monthly deposits, and everything is free to the client!

We now know that you either have to turn them away (bad), charge them high trading fees (not good), or leverage platforms that can change their agreements on a dime (“Ameritraded”).

We feel your pain and share in your desire to help the little guy/gal. I can’t tell you how many Alpha Architect blog readers reach out to us with the following:

“Love the content, love the education, want to be a part of the team and work for free, and I want to invest my $1,000 in life savings.”

We love these guys and gals because we were all broke finance students at some point and our mission to empower investors via education is being fulfilled.

But I would contend that advisors facing similar client prospects start with the following rules of thumb:

- You do NOT need to manage someone’s money to build a relationship with them.

- If a client doesn’t have 6 (preferably 12) months of emergency savings somewhere, don’t put them in the stock market (shocker).

- Understand the business investments you are making and compare that to the fees you could pay on a platform.

Point #1: You do NOT need to manage someone’s money to build a relationship

We often hear advisors lament:

I really want to help this kid, but she only has a net worth of $10k and $50k in students loans. I put her in a 60/40 portfolio and charge 1%.

Some advisors with smaller practices fear that if they don’t push prospects into managed accounts immediately, they will lose them. And while they try and help this client as best they can, they are now in danger of getting Ameritraded (you can only support clients like this with subsidized platforms).

Building lifelong relationships with someone is a platform agnostic exercise and doesn’t require an immediate “close.” If you do right by your prospects, help them, and are transparent, the client will eventually come around and want your support. Trust is earned.

Now, this approach does not mean advisors can’t run a business with small clients. Charge a flat fee for a financial planning meeting, explore a newsletter that future clients can read, learn, and pay a small amount for, etc. There are a million ways to develop a viable business model that does not depend on someone else’s platform for success. Those that figure out viable models in this context will be the winners of the RIA game down the road.

Point #2: If a prospect lacks the emergency savings necessary…don’t put them in the market

If you have a millennial prospect with less than six to twelve months emergency savings…should they be invested in the market at all? I am a strong “no” on this point, but others may differ. Most advisors try to do the right thing; however, a minority does encourage investing so early that any downturn can have serious financial repercussions for those just starting out. At some level, maintaining a kitty for beer money, food, and rent is arguably more important than investing — the idea of being Warren Buffett is cool, but paying your rent next month is also “cool”.

Point #3: Understand the business investments you are making and compare that to the fees you could pay on a platform.

We observe countless advisors making expensive, low ROI investments in “relationship-building activities,” yet they bristle at paying trading fees or waiving management fees for small clients. One advisor we know hosts countless breakfasts and lunches, costing several thousands of dollars a year, and achieves minimal new business as a result. I would challenge advisors to crunch numbers as to what the best investment is to make. For some, ditching the paid lunches in exchange for reducing a management fee to offset trading costs could be the way to go. Not a definite per se, but running some analysis on what does/doesn’t add value is probably a worthy exercise.

But let’s say you’ve found a small client that is ready for your services and you’re trying to find a viable solution for them. Now you’re faced with trading costs. Even if you are running a passive strategy with low turnover, the client’s account will incur transaction costs. This is where it gets complicated. Let’s dig in…

Thinking About Best-Execution for small clients when evaluating brokerage platforms?

Now that we understand how our platform(s) get paid and how we can serve small investors effectively, we must now take the giant leap onto a platform that suits our needs. “Best execution” as defined by the SEC and FINRA implies some degree of latitude between trading cost and qualitative factors (e.g., customer service, the responsiveness of trading desk, etc.). For managed accounts, we recommend providing the cheapest, lowest all-in trading cost to the client (and not just for big clients!). Everyone must choose a platform that makes the most sense for their business, but I find this approach is the simplest, most transparent, and most justifiable approach to regulators. If it takes us a little more time to onboard someone, or if the client portal is a little wonky, that is fine by us, so long as the client is saving money and keeping more of their wealth.

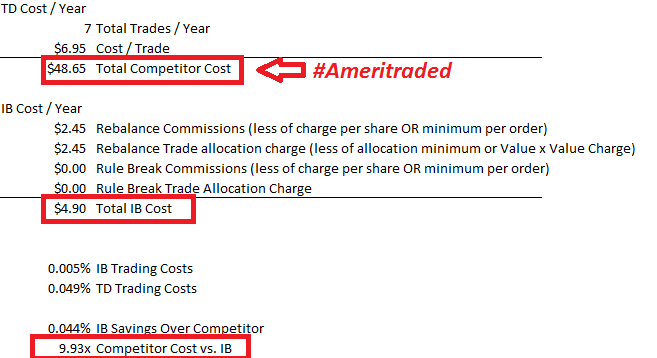

With this in mind, let’s compare a simple buy and hold portfolio traded at TD ($6.95/trade) with the low-cost leader, Interactive Brokers (IB) (1/3 of one penny per share, 35 cent minimum plus 35 cent trade allocation charge).(1)

Assumptions:

- 7 ETFs

- Rebalance 1x a year

- 10% style drift at rebalance

- $100,000 account(2)

Source: Alpha Architect

Look at the red boxes.

Running this portfolio at IB costs $4.90 a year, all-in. Running the same portfolio at TD costs almost 10x more at $48.65 / year. We are talking half a basis point versus 5 basis points, but on a strict cost basis, TD is ~10x more expensive. And in a world where advisors complain about the SPY’s management versus VOO’s asset management fee, well, 4.5bps might matter. Of course, the critical piece is that the account minimum is $100,000 for this math to work out at IB.

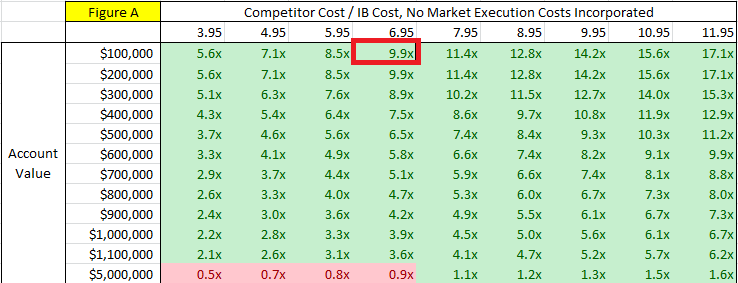

Now, let’s do a sensitivity analysis with the same portfolio. In the table below, the vertical axis is a client’s account value and the horizontal axis is a variety of “flat fee” platforms commission charges. In our previous example, Fidelity charged $6.95/trade and we assessed a $100k account. The 9.9x figure in the red box represents the multiple of TD costs/IB (10x). Note that, “No market execution costs incorporated” refers to bid/ask spreads, market impact, payment for order flow, etc. So the tables below deal with straight up commission costs.

Zooming out to the entire table, green cells = IB is cheaper. Red Cells = IB is more expensive.

Source: Interactive Brokers and Alpha Architect

As you can see, using a low-cost broker is a whole lotta green…

Now, this analysis isn’t earth-shattering. IB is known for being low-cost, and TD is known for having a killer platform, hence the price difference. I do think it is worthwhile, however, to highlight the multiple on savings between options.(3)

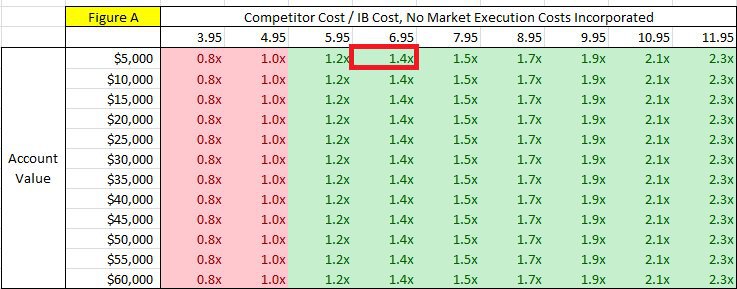

Now, let’s look at the same analysis, but assume we have small accounts with someone just getting started. IB charges a minimum monthly fee of $3 a month for investors age 25 and under. Let’s run the same analysis, but let’s just change the client account size to below $100k to trigger the minimum account charge of $3/month for young investors at IB.

Source: Interactive Brokers and Alpha Architect

As you can see, IB still “wins” until the commission rate hits $4.95 (tie). The only loss is when the flat trade platform charges less than $4.95 a trade.

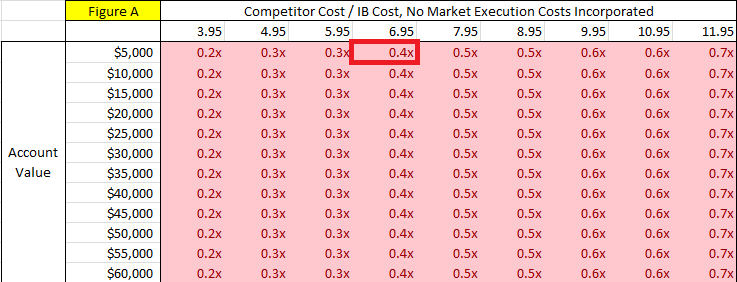

OK., fine, but what happens when the investor is older than 25 AND has a small account? The IB flat fee jumps to $10/month minimum, and thus, gets crushed by the TD player.

Source: Interactive Brokers and Alpha Architect

Not looking good for IB. Clearly, if you are over 25 years old and have less than $100k, IB does not want your business and a client would be better off at a fixed commission broker (assuming commission costs were the primary decision point).

So where does this analysis leave us?

As an advisor, you can choose a flat rate/trade platform, but be outgunned on cost for young investors and anyone with more than $100k. You can go with a low-cost leader (e.g., IB) and provide hands down best execution above $100k and below $100k for young investors, OR, you can maintain commission-free ETF portfolios, but run the risk of getting #Ameritraded whenever a service agreement changes between the broker and the asset manager. In our view, if you are going for long-term client relationships and want to provide the lowest cost over the long term, we think a low-cost leader is a good bet.

But this is all small dollars, right?

As we mentioned earlier, we are talking a handful of bps here. Who cares? Why bother? The answer is simple: demonstrating attention to detail matters. We know plenty of high net worth types that still pack a lunch, buy their gas at Costco, and drive beat-up cars. Clients appreciate those that demonstrate they fight for every penny, regardless of how small. Conversely, clients can also appreciate a transparent conversation about why you choose a particular platform and what that platform does:

You may be paying more for trades, but look at features X, Y, and Z that provide A, B, and C benefit.

Wrapping up: Choose for the long haul

Choosing an investment platform is a serious decision. There are strengths and weaknesses of each that extend well beyond the initial growth phase of an advisory practice. Changing custodians is a total nightmare. Managing a multi-custodian business platform is expensive and complex. The current broker/custodian environment doesn’t make life easy! And as TD Ameritrade demonstrated, a platform’s objectives may not align with your own. There are a myriad of items to consider that we didn’t cover here (how your orders get executed, payment for order flow, exchange rebates, and the like), but we hope it’s a good foundation to spark some internal discussions and debate.

Note: We receive no compensation of any kind from any broker or custodian.

References[+]

| ↑1 | Each platform targets a particular segment. But when it comes to explicit costs, there is a clear leader: Interactive Brokers (“IB”). We are ardent Interactive Brokers fans simply because we know exactly how they get paid and are willing to dig into the weeds on their systems (IB is not plug and play!). The firm charges extremely low fees and they are super transparent. No payment for order flow, no hidden charges, an ability to capture exchange rebates for clients, etc. Game over. And when the regulators inspect the books and want a justification for why IB is best for clients, it’s a no-brainer (more on that below). That said, there are certainly limitations to their model: customer service is weak relative to TD and Schwab, the user interface is wonky (but getting better), and they charge fee minimums on clients that are too expensive to serve (e.g., any account below $100k for investors over 25 years old gets hit with a $10 min charge per month.) |

|---|---|

| ↑2 | below this IB would charge $10/month |

| ↑3 | Note: for really large accounts, I would argue that IB is still a better deal given payment for order rebates, scale rebates, and other charges, but that is a different post for a different day. |

About the Author: Pat Cleary

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.