What Free Lunch? The Costs of Overdiversification

- Shawn McKay, Robert Shapiro, Ric Thomas

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category.

What are the research questions?

- How diversified are pension funds?

- At what level of diversification do their holdings converge toward indexation?

- What are the key challenges?

What are the Academic Insights?

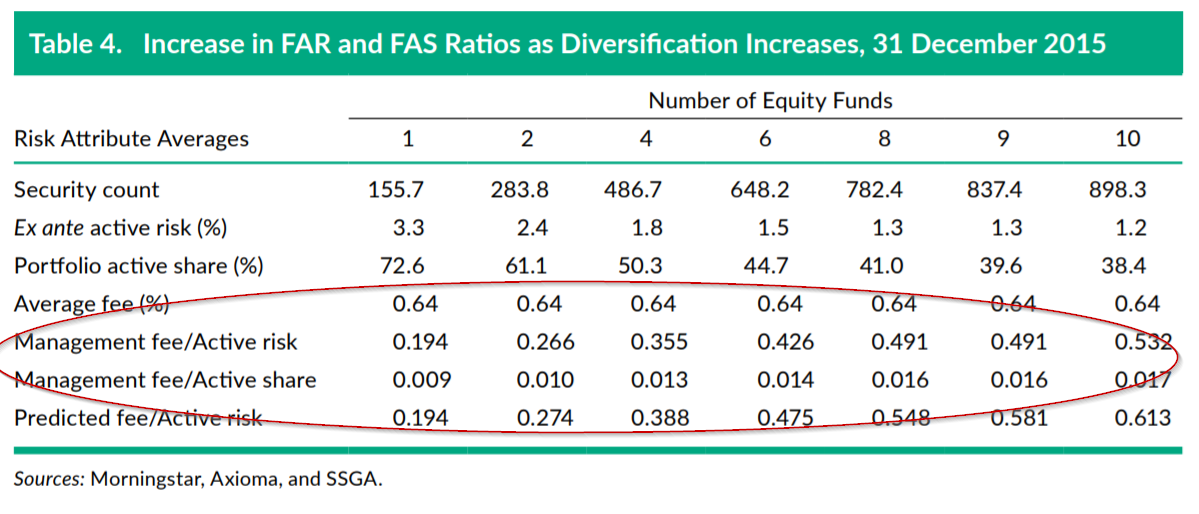

- On average, large DB plans use 75 external funds ( inclusive of all asset classes). When focusing the analysis on equities, the authors find that the funds allocated, on average, to 17 funds. Hence, they seem to favor manager diversification and use dozens of external strategies to diversify active risk.

- The authors find that as we move toward 10 fund managers (aka portfolios, aka strategies), it becomes exceedingly difficult to a create a blend with active risk greater than 2%, suggesting that even if pension funds are determined to maintain high levels of active risk, it becomes practically impossible to do so. Similarly active share and stock specific risk decline.

- However, the decline in active risk, active share and stock specific risk is not accompanied by a corresponding decline in fees. This leads to less productive fee ratios per active risk. Specifically, based on the empirical analysis performed, fees rise from 19 bs to 53 bps per unit of active risk, as we move from 1 to 10 equally weighted strategies.

Why does it matter?

The authors show that diversification among active managers can be unhealthy because of the following:

- active risk (active share and stock specific risk) declines

- the required excess return forecasting ability needs to increase exponentially

- fees will rise with the same level of active risk

The authors suggest a simple framework where it is possible to target a given fee ratio to determine the number of optimal managers. Plans that move in the direction of simplification are likely to reduce both the explicit and the implicit expenses at the total fund level.

The Most Important Chart from the Paper:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Institutional investors, charged with outperforming a policy benchmark, often allocate to external active managers in order to hit their return objective. The challenge is to do so without overdiversifying the plan. Hiring too many managers can significantly reduce active risk, leaving the plan with high fees and limited ability to outperform a policy benchmark. We review the number of external investment strategies held by the largest US public and corporate pension funds. Our analysis shows that most large pension funds are overdiversified, allowing us to suggest a simpler framework for moving forward.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.