Do Independent Director Departures Predict Future Bad Events?

- Rüdiger Fahlenbrach, Angie Low, and René M. Stulz

- The Review of Financial Studies

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

- What are the general circumstances associated with independent director departures?

- Is it possible to identify situations whereby the departure is unexpected and not due to retirements, director outside commitments or firings by the firm?

- Are the unexpected or surprise departures followed by negative stock market return performance?

- Are the unexpected departures followed by adverse events at the same firm?

- Are the subsequent negative returns and events the cause of the surprise departure?

What are the Academic Insights?

- The probability that an independent director will resign is increased under a number of general circumstances, to include: if the director is 70 years or older or exhibited attendance problems; if work commitments changed, such as being appointed to other boards or not appointed to key subcommittees of the board; if the firm exhibited poor accounting and/or stock price performance; if the firm is larger; or the CEO left in the prior year.

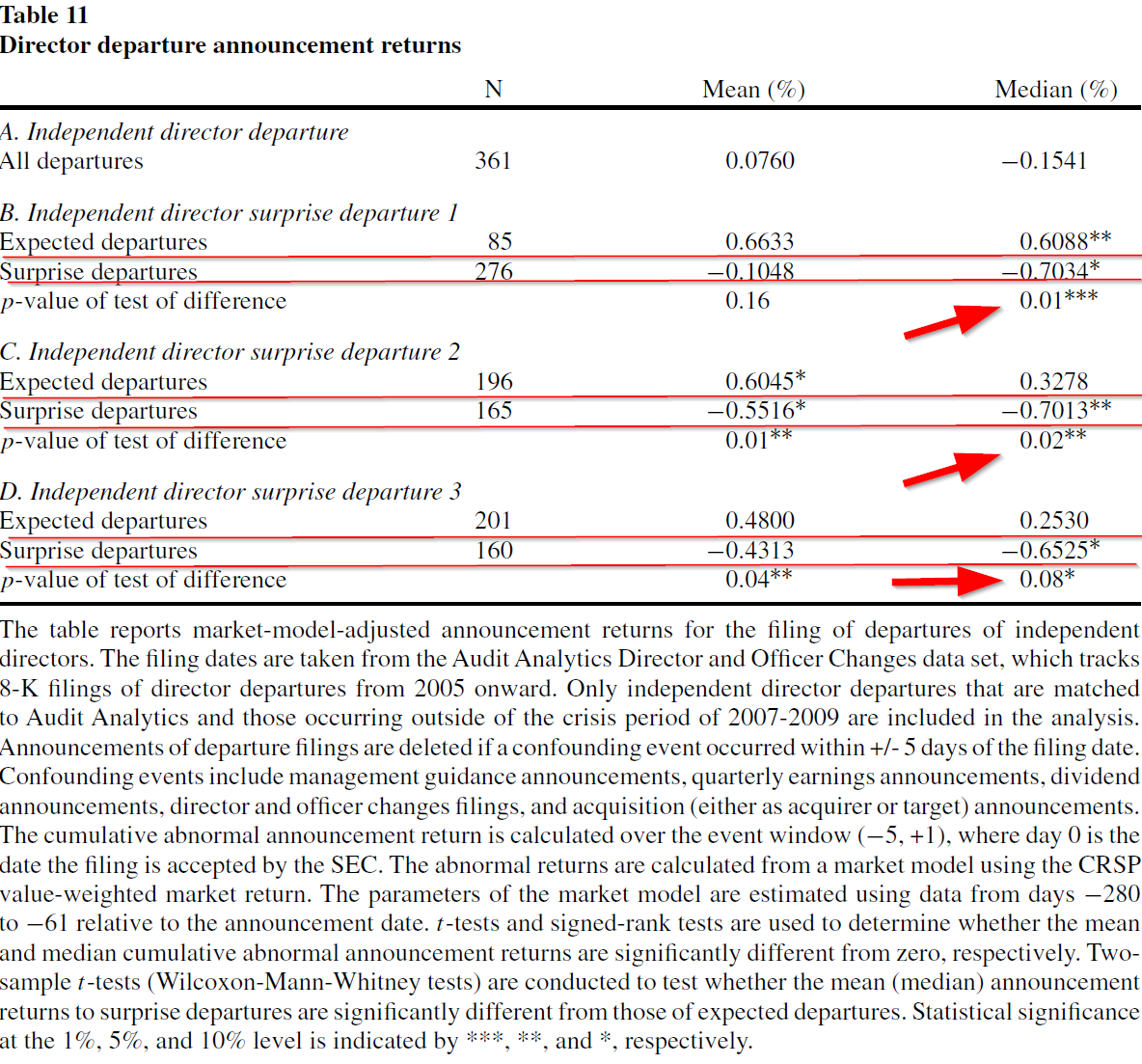

- YES. The market appears to infer bad news associated with independent director departures that are unexpected. The authors construct three versions of instrumental variables that capture the departures of directors not motivated by circumstances of age, work commitments, poor attendance, firings, or poor firm performance over the past one year.

- YES. The average announcement day return for the three surprise departure measures was -.7034%, -.7013%, -.6525%, respectively. For the subsequent twelve months, the monthly return performance for firms with unexpected departures underperforms those with expected departures by about 45bps, if value-weighted and 14bps if equally-weighted. Firms with expected director departures only, do not underperform.

- YES. Over the twelve months subsequent to an unexpected director departure, there is a higher and economically significant increase in the probability of a future negative event. For example, the probability of an earnings restatement increases by 25.5% following a surprise departure. For shareholder lawsuits alleging financial fraud, the probability increased by 23.8% after a surprise departure. The combination of a surprise director departure and M&A announcement events produced returns 1.7% lower than without prior surprise departures. There was no increase in the probability of any of the same negative events for firms experiencing expected departures.

- YES. Causality tests conducted in this study are consistent with the idea that directors resign as they anticipate the publication of bad news or the occurrence of negative events.

Why does it matter?

The majority of research on board structure is focused on the demand side of the market for independent directors. Theoretical treatments of the topic emphasize the costs and benefits of independent directors. They conclude independent directors may have weaker incentives to perform and will rely on CEOs for information and opinions. The empirical literature on the topic primarily focuses on the makeup and characteristics of the average board.

In contrast, this study explores the supply side of the director labor market and the impact of unexpected director departures on operating performance and return performance of those firms. The authors point to the need to study the impact of compensation policy for independent directors, including their equity holdings, grants and other financial incentives to offset their propensity to resign to avoid reputational loss.

The most important chart from the paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Following surprise independent director departures, affected firms have worse stock and operating performance, are more likely to restate earnings, face shareholder litigation, suffer from an extreme negative return event, and make worse mergers and acquisitions. The announcement returns to surprise director departures are negative, suggesting that the market infers bad news from surprise departures.We use exogenous variation in independent director departures triggered by director deaths to test whether surprise independent director departures cause these negative outcomes or whether an anticipation of negative outcomes is responsible for the surprise director departure. Our evidence is more consistent with the latter.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.