Go Before the Whistle Blows: An Empirical Analysis of Director Turnover and Financial Fraud

- Yanmin Gao, Jeong-Bon Kim, Desmond Tsang, Haibin Wu

- Review of Accounting Studies

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

- Is the rate of turnover for outside directors unusually high either before fraud is discovered by the firm, or during its commission?

- Are there regularities in the characteristics of outside directors who depart during the period in which the financial fraud is committed?

- Are there regularities in board governance variables related to the turnover of outside directors for fraud firms?

- Is the severity of the fraud related to higher turnover rates for outside directors of fraud firms?

What are the Academic Insights?

- YES. The unexpected turnover of outside directors from fraud firms matched to a control sample of non-fraud firms was higher for fraud firms at 19.49% compared to 12.31% for the control group. Firms were matched on industry, firm size, and the period over which the fraud occurred. Results were also controlled for other firm characteristics including director and board governance characteristics.

- YES. Female outside directors are found to be more likely to leave fraud firms. The results reported are consistent with other research that finds women are more risk-averse, more vigilant about ethical issues and exhibit greater efforts toward monitoring as board members when compared to male directors. In addition, directors holding relatively more of the firm’s shares are also more likely to depart. This result is consistent with previous research establishing that constituents with higher financial stakes are more likely to leave fraud firms because they are better informed about fraud activities. It also appears that they are not likely to enforce punitive measures on management as a result of their dominant position. The results presented here are more consistent with the notion that these types of outside directors have larger reputational concerns and therefore choose to resign instead.

- WEAK or NONE. There is weak evidence that the size of the board, the number of board meetings held, and the level of financial expertise of outside directors is positively related to the turnover ratio for fraud firms. There was no evidence of a significant relationship for other governance variables including size of the board, the degree of board independence, the number of board meetings, the size of the audit committee, and the proportion of financial experts on the audit committee.

- YES. Turnover of outside directors varies positively with the severity of the fraud. Especially notable are cases where the fraud involves either fabricated business activities, or issues of problematic disclosures, or there are relatively larger monetary settlements.

Why does it matter?

This research matters because it is one of the first to study the behavior of outside directors during the period that the fraud was committed and before the public disclosure of that fraud. In contrast, the prevailing literature on this topic to date has focused on board behavior subsequent to the public disclosure of fraudulent activity. Surprisingly, the authors report that a significant proportion of outside directors choose to resign rather than attempt to mitigate or correct the fraudulent activity. As the authors put it–at least some of them choose to “vote with their feet.” The implications for policy and regulators reinforces the notion that the mere presence of a board of directors, long believed to be the watchdog for financial reporting and ethical practices, is unlikely to provide fully effective monitoring and oversight. This research suggests that at least a proportion of directors would rather walk away rather than face full-on the demands of remediating firm irregularities and possibly suffer reputational loss.

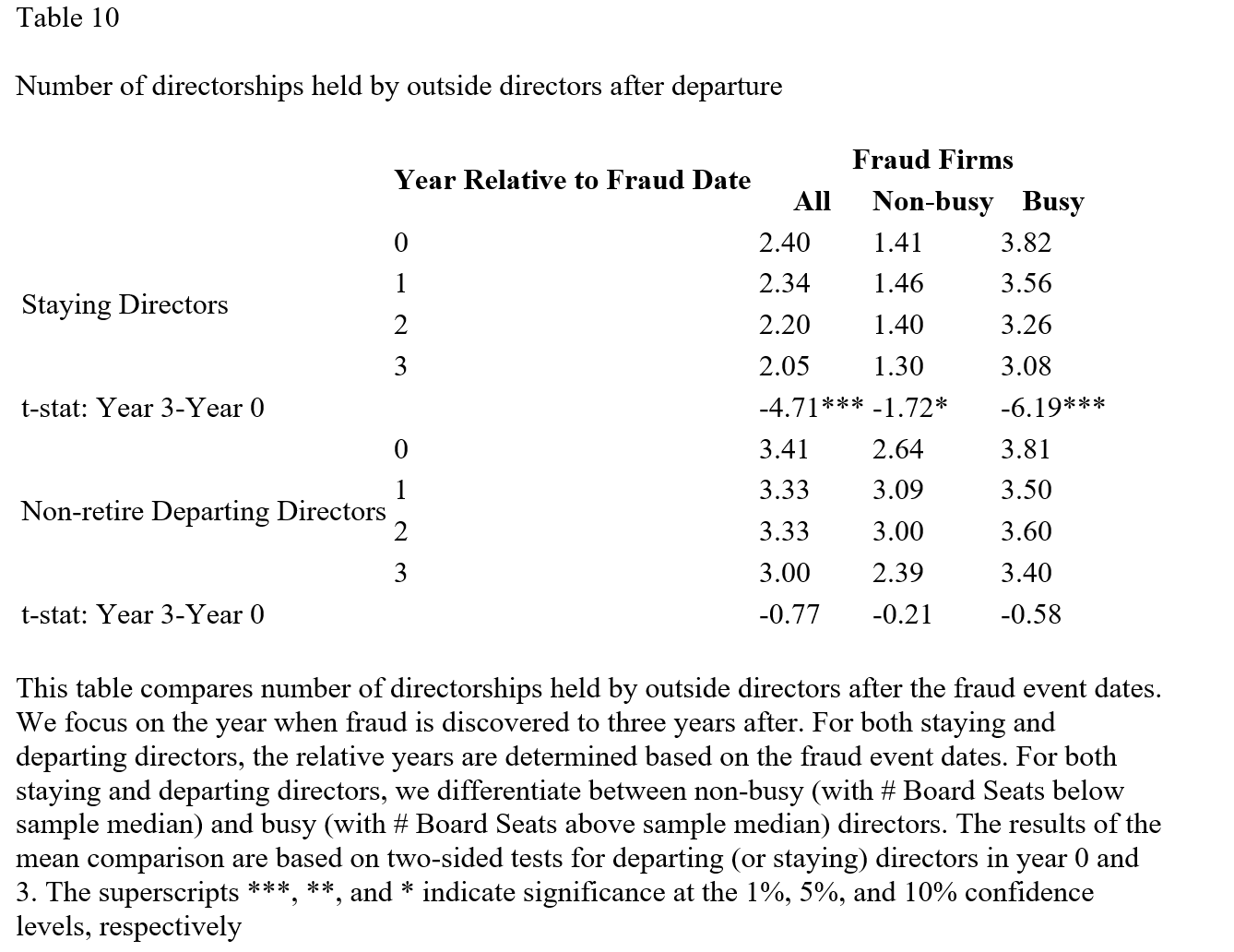

The most important chart from the paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

This study investigates whether outside directors are aware of financial fraud. Our analysis focuses on the abnormal turnover of these directors during the fraud committing period, before fraud is discovered and before lawsuits are filed. Our empirical analysis shows that, during the fraud committing period, outside directors in fraud firms exhibit an abnormal level of turnover. Examining the characteristics of outside directors and boards at these fraud firms, we find strong evidence that female directors, directors who have greater stock ownership in the firm, and directors with multiple directorships at other firms are more likely to depart fraud firms. We also find some evidence that board size, number of meetings, and fraction of financial experts are related to abnormal turnover in fraud firms during the fraud committing period. We show that abnormal director turnover is significantly higher for fraud that is considered more egregious (i.e., involving fictitious transactions and disclosure problems). Lastly, directors are more likely to depart fraud firms with more serious fraud, as proxied by higher ex-post settlement amounts and longer fraud duration.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.