Protecting the Downside of Trend When It Is Not Your Friend

- Kun Yang, Edward Qian, and Bran Belton

- Journal of Portfolio Management

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

In Part 1 of this article, we reviewed the performance of using a more complex form of simple trend following (i.e. adding a channel breakout rule alongside a simple time-series momentum rule). The simple trend signal (S) used was based on the sign of the trailing 12-month return of the asset. The universe tested was robust. Assets included at least 60 liquid futures/forward contracts across international asset classes: 23 commodity futures, 13 equity index futures 11 sovereign bond futures, 19 developed and emerging markets FX forwards. The simple signal is enhanced (C) by entering a long(short) if the simple signal is positive and above the 200-day maximum (minimum). The long(short) exit occurs when the price trades below the 100-day minimum (maximum) or the simple signal is negative. Notably, two portfolio construction approaches were also tested: equal volatility (EV) and risk parity (RP). Implementation and trading costs were included in the analysis.

- What was the upside participation performance for the complex signal, the risk parity construction and the C+RP strategy?

- What was the downside participation performance for the complex signal, the risk parity construction and the C+RP strategy?

- Was there a net participation advantage to any of the enhancements to the simple trend strategy?

- Which portfolio construction method was superior?

What are the Academic Insights?

- The participation measure used was the positive mean net excess ret for the studied strategy relative to that of the benchmark strategy, S+EV in percentage terms: Relative to the benchmark positive return, the C+EV strategy captured 90%; the S+RP strategy achieved 101% of the positive benchmark return; and the C+RP strategy achieved 94%. During the top 5 extreme periods, when the benchmark strategy performed very well, mean net cumulative return = 34.89% , the 3 other portfolios achieved 84%-85% of that upside return.

- Relative to the benchmark negative return, the C+EV strategy captured 79%; the S+RP achieved 94% of the negative benchmark; and the C+RP strategy achieved 76%. During the 5 worst periods, when the benchmark portfolio suffered significant losses (mean net cumulative loss = -17.38%), the other 3 strategies captured 38%-70% of the downside. During the maximum drawdown period (-25.67%, Sep2009-Feb2012), the C+EV and C+RP achieved slightly positive returns.

- YES. All 3 of the strategies tested against the simple trend strategy achieved more of the benchmark’s upside return than it’s downside. The total participation advantage is the difference between the upside and downside participation measures: C+EV = 11%; S+RP=7%; and C+RP = 18%. That is, if the breakout/exit feature is added to the EV construction, the C+EV strategy achieves 90% of the positive benchmark return while achieving 79% of the benchmark negative return with a net total advantage of 11%. Basically, a penalty of 10% of the benchmark positive return is paid in order to achieve downside protection. The results for the RP construction used with a simple signal achieves 101% of the positive benchmark return while achieving 94% of the negative benchmark return with a total net advantage of 7%. This equates to a 0% penalty of the positive benchmark return to achieve downside protection. Finally, the C+RP strategy achieves 94% of the positive benchmark return while achieving 75% of the negative benchmark return with a net advantage of 18%, a penalty of 6% to capture downside protection.

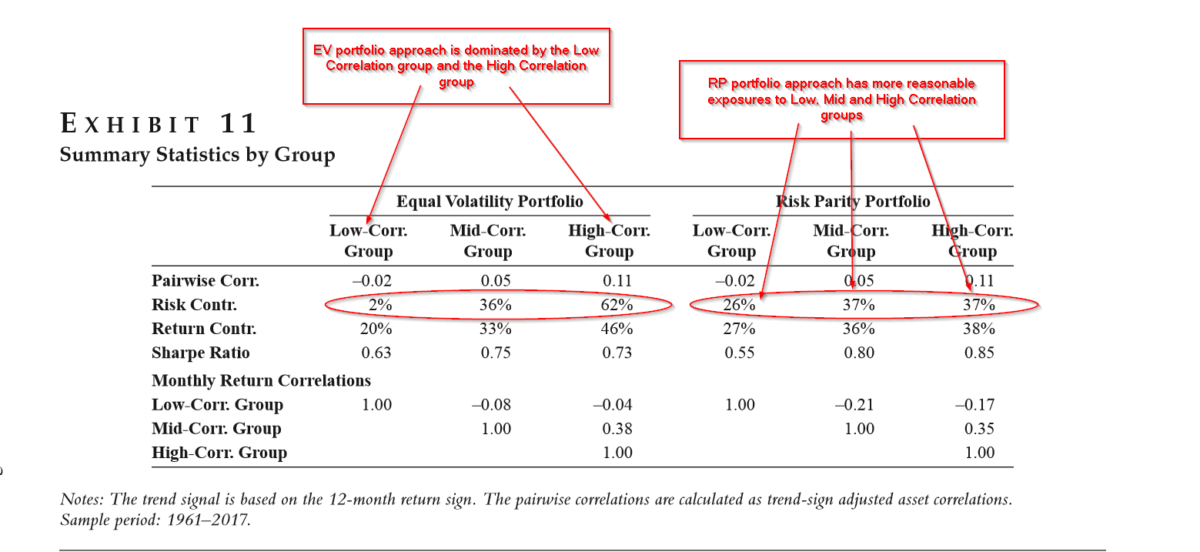

- RISK PARITY. RP provided superior diversification benefits by incorporating correlations among trends for the assets included in the study. This was true for the simple and enhanced or complex trend signals. Assets were classified into high, medium, and low correlation groups based on their average pairwise trend correlations at each month-end. As shown in Exhibit 11, the high correlation group dominates the EV approach, while the RP approach balances risk across all 3 groups of assets. The EV approach sizes the trending assets such that each position targets the same expected risk, but ignores the correlations between the trending assets. Low vol assets like bonds and currencies, tend to have larger weights than high vol assets such as commodities and equities. Thus, high vol assets are prevented from dominating overall portfolio volatility. However, without accounting for the correlations among the trends the targeting and controlling a constant portfolio risk becomes problematic and difficult to achieve. In contrast, the RP approach solves for the optimal weights that equalize the risk contribution of each asset to the portfolio using both volatility and correlation structure.

Why does it matter?

Using a simple equal-weight portfolio and a generic 12-month time series rule is an interesting technique for capturing the benefits of trend-following strategies. However, by volatility-weighing positions and adding a channel break-out component to the time-series, the results can be enhanced. “Both the Sharpe ratio and return correlation statistics justify the diversification benefit of the low-correlation trend groups, and hence explain the optimality of the RP approach relative to the EV approach.” While the subject of enhancing a simple trend signal is certainly important, the risk mitigation aspects of using an approach that optimally weights assets appears to be the linchpin to success and should be emphasized to investors and managers.

The most important chart from the paper

Source: Kun Yang, Edward Qian, and Bran Belton Protecting the Downside of Trend When It’s Not Your Friend, 2019 The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Simple trend-following strategies have been documented as cost-effective, transparent alternatives to the hedge-fund style managed futures strategies. Although largely capturing the returns of the managed futures industry, those simple strategies may periodically suffer significant losses due to oversimplified trend signals and underdiversified portfolio construction. In this article, the authors show that trend-following strategies with moderate sophistication and better diversification can significantly reduce the downside risk of simple trend-following strategies without sacrificing much upside potential. The authors therefore recommend that investors who seek the benefits of cost-effective trend-following strategies consider adding reasonable complexity to the strategies.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.