Economic theory suggests that companies neglecting to manage their environmental, social and governance (ESG) exposures could be subject to greater risk than their more ESG-focused counterparts. The argument is that companies with high sustainability scores have better risk management and better compliance standards. But do better ESG practices boost valuations? The stronger controls lead to fewer extreme events such as environmental disasters, fraud, corruption and litigation, and the risk of consumer boycotts (and their negative consequences). The result is a reduction in tail risk in high-scoring firms relative to the lowest-scoring firms. The reduction in risks leads to higher valuations.

It follows, then, that improving ESG scores can lead to higher valuations, leading to capital gains in the short term for investors. The idea is similar to the concept of fundamental momentum in equities. In his 2015 study “Fundamentally, Momentum is Fundamental Momentum,” Robert Novy-Marx demonstrated that stocks that have recently announced strong earnings tend to outperform going forward. The theory has led to researchers examining the relationship between ESG scores, valuations and returns.

Madelyn Antoncic, Geert Bekaert, Richard Rothenberg and Miquel Noguer, authors of the 2020 study “Sustainable Investment – Exploring the Linkage Between Alpha, ESG, and SDG’s,” found that firms with positive momentum in their MSCI ESG ratings outperformed their risk-adjusted (for factor exposure) benchmark. And George Serafeim, author of the 2020 study “Public Sentiment and the Price of Corporate Sustainability,” found that the market valuation premium of firms with better ESG performance had increased steadily over the prior 15 years. Given that there are hundreds of ESG variables—more than 630 in Refinitiv only—a more intriguing question is: Can we identify which key variables play the most important role in improving valuations?

New Evidence

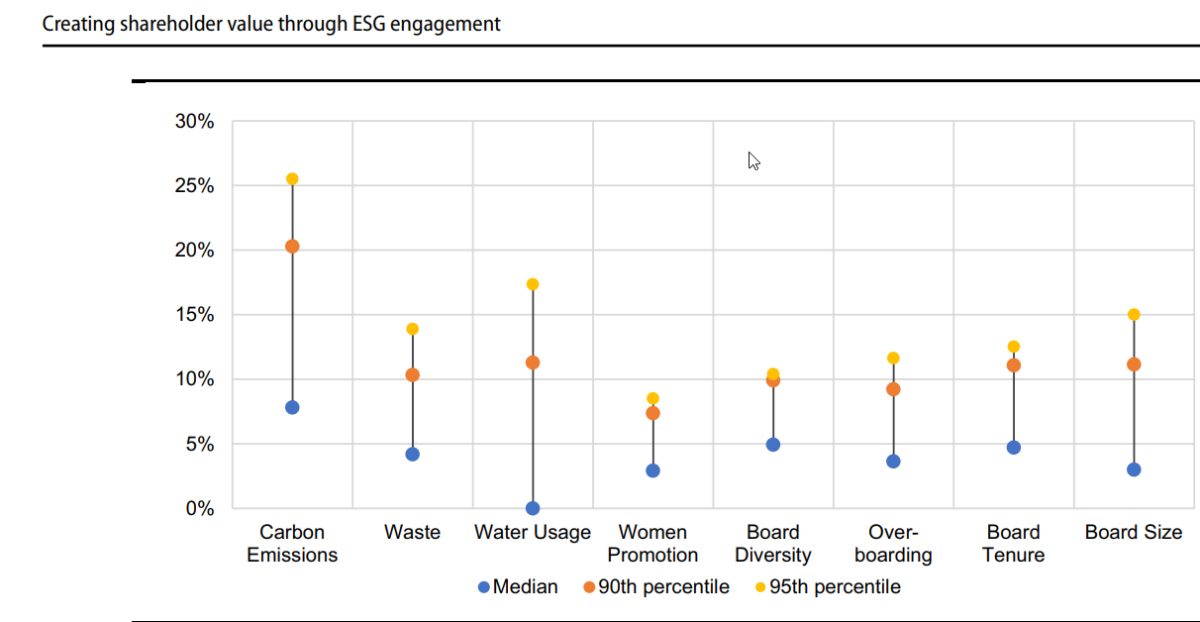

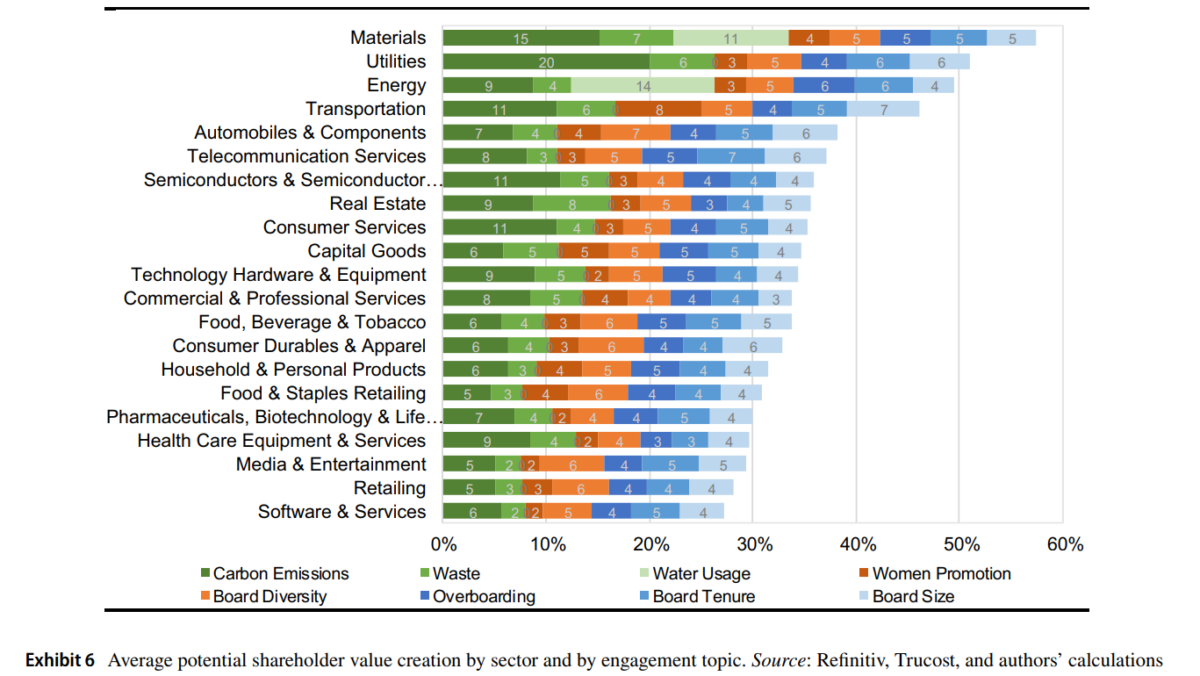

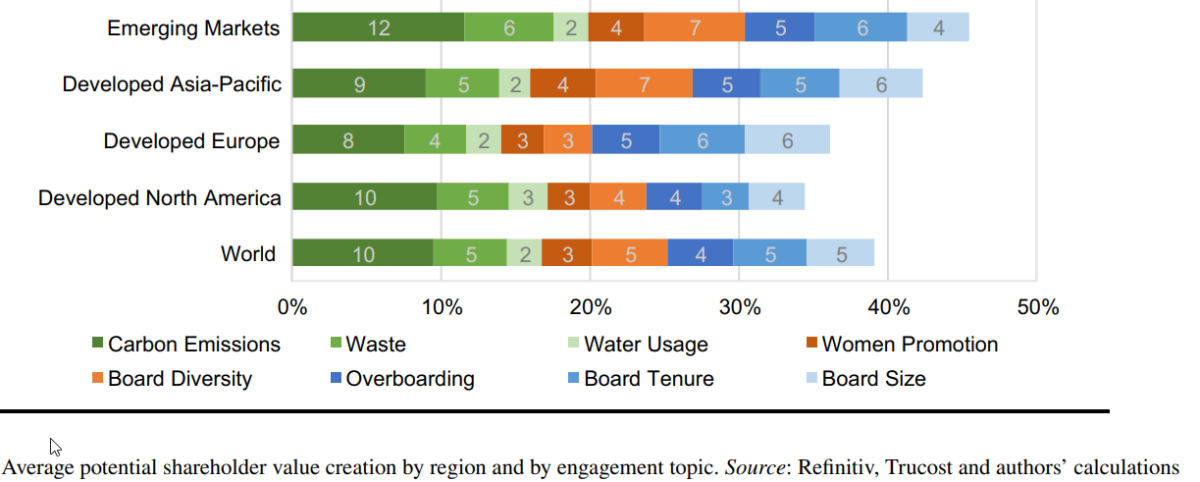

Benoît Mercereau, Lionel Melin and Maria Margarita Lugo, authors of the study “Creating Shareholder Value Through ESG Engagement,” published in the December 2022 issue of the Journal of Asset Management, examined how eight key E, S and G variables influenced firm valuation. The eight key ESG variables met three criteria: high corporate materiality, high market relevance and high data availability. The authors explained: “The variables cover the biggest E, S, and G themes: carbon emissions, waste generation, and water usage for ‘E’; board gender diversity and women promotion for ‘S’; and board size, tenure, and overboarding for ‘G’.”

Their data sample included firms in the MSCI All Country World Index (MSCI ACWI). Their ESG data was from Refinitiv, though they used S&P Trucost carbon emissions data to supplement Refinitiv’s. They considered numerical variables only “as they are more precise than qualitative variables and are better suited for econometric modeling”, and only 20% of Refinitiv ESG variables are numerical. They used the Sustainability Accounting Standards Board (SASB) Materiality Map as a guide to corporate materiality.

To estimate what drives firm valuations, they used two measures: price to 12-month forward earnings (P/E) ratio; and price-to-book (P/B). Their estimation period covered 2012-20, with 2012 being the first year Trucost data was available. Following is a summary of their findings:

- All eight ESG variables were statistically significant and economically meaningful. For example, cutting carbon emissions from a sector’s bottom to its top decile raised shareholder value by 17%, while improving board diversity from bottom to top decile raised shareholder value by 7% on average.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

- The impact on valuations varied across sectors—cutting emissions 10% raised firm value more in carbon-intensive sectors than in other sectors, and markets valued water usage only in the few industries where water is material (i.e., materials and energy).

- Emissions increasingly hurt equity valuation, especially in carbon-intensive sectors—carbon emissions hurt valuation twice as much in the last five years as in the previous five.

- Enhancing ESG could unlock significant shareholder value. For example, by achieving 90th percentile scores, valuations could be improved by 8% for cutting carbon emissions and by 3% for improving women’s promotion or board diversity. Firms adopting top decile practices across all eight variables could boost their equity valuation by 35% on average—with more than half of this gain (21.5%) stemming from improving the two most relevant ESG issues (which depended on the sector). Improving two ESG variables could unlock over 30% of shareholder value in over 20% of stocks, and over 15% of shareholder value in 75% of stocks.

- Potential gains from improving ESG were highest in emerging markets.

Investor Takeaways

The research we have reviewed demonstrates that firms with improving ESG scores earn higher valuations, leading to capital gains in the short term for investors. And it seems likely that Mercereau, Melin and Lugo’s estimates are even conservative over the medium term because, as Sam Adams and I demonstrated in our book “Your Essential Guide to Sustainable Investing,” the research—including studies such as “ESG Investing: From Sin Stocks to Smart Beta” and “Foundations of ESG Investing: How ESG Affects Equity Valuation, Risk, and Performance”—has found that higher ESG-scoring companies are more profitable: As scores improve, earnings could rise as well as valuations. Mercereau, Melin and Lugo also pointed out which ESG metrics have the largest impact on valuations, helping corporations (and investors) identify which issues are the most important for them to focus on from a valuation perspective.

A further important insight concerns the likelihood that an ESG influence on share prices will affect corporate behavior. If ESG-compliant companies enjoy higher share prices and a lower cost of capital, they will be incentivized to improve their ESG ratings. Thus, a focus on sustainable investing can cause companies to behave in a more positive manner—a desirable result from all perspectives. The bottom line is that sustainable investors are not only investing according to their values, but their cash flows are driving firms to become better corporate citizens.

Finally, investors buying highly rated ESG stocks have been driving valuations higher, which in the long term dampens future expected returns. The conflicting outcomes—higher returns in the short term (resulting from rising valuations) but lower future expected returns (as a result of the higher valuations)—is an important insight and helps explain some of the conflicting findings in the literature on the returns to green versus brown stocks. Investors who wish to invest sustainably should have reasonable expectations, including a willingness to accept lower long-run returns.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this document. LSR-22-432

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.