Following the global financial crisis of 2008-2009, tightened capital standards made loans to middle-market companies unattractive for banks, shutting out most small- and middle-size companies from the bank market. In addition, the 2010 enactment of the Dodd-Frank Act made it increasingly expensive for small banks to operate, cutting off their supply of loans to small and mid-size companies—and small and mid-size banks were significant lenders to this market. Private credit rushed to fill the gap that the banking industry was no longer able to fill because of the distress of their balance sheets.

Another reason for the explosive growth is that corporations have found benefits in private lending that are sufficient to offset their higher yields. Those benefits include:

- Speed of execution.

- No mandated public disclosure of proprietary information.

- Less ongoing disclosure requirements required for fundraising in the public market.

- Avoiding the time-consuming and expensive process of obtaining a rating from one or more of the rating agencies.

- The ability to customize the loan structure to meet the needs of the borrowing company, offering management greater flexibility.

- A borrower facing financial difficulties will find it is easier in a private debt transaction for management to do a workout with only one or a few lenders compared to many lenders in a public bond offering.

Risk and Return Data

Cliffwater has been a leader in alternatives for 20 years through its proprietary research, indexes, and investment solutions. In 2015, they launched the Cliffwater Direct Lending Index (CDLI)—an index of private middle market loans. Created to measure private loan performance and better understand its investment characteristics, the CDLI was reconstructed back to 2004. It was the first published index tracking the direct lending market. As of November 2024, it covered about 17,300 directly originated middle market loan holdings totaling about $393 billion.

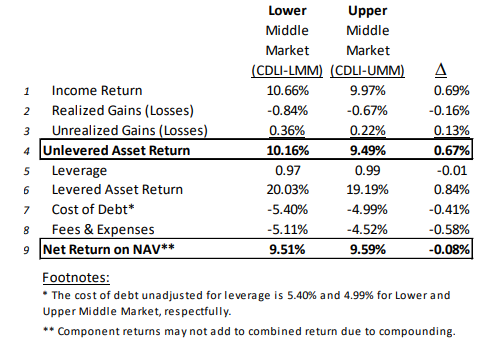

To better serve investors, in December, Cliffwater introduced two new indices that differentiate performance between two submarkets of the CDLI: the Cliffwater Lower Middle Market (LMM) and Upper Middle Market (UMM) Indices. The UMM is defined as private loan collateral with borrower size greater than $100 million of EBITDA. The LMM is defined as private loan collateral with borrower size less than $30 million of EBITDA. The two indices enable investors to answer questions related to the impact of borrower size on return and risk. The table below compares the five-year returns ending September 30, 2024, for the newly created LMM and UMM Indices.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

As should be expected, loans in the LMM carried a higher rate of interest (10.66% versus 9.97%). However, the higher cost of debt associated with the leveraging of assets (5.40% versus 4.99%), the somewhat higher realized losses (0.84% versus 0.67%), and the higher fees and expenses (5.11% versus 4.52%) negatively impacted returns of the LMM relative to the UMM. The LMM index did benefit from slightly higher unrealized gains (0.36% versus 0.22%). The net result, after credit losses, borrowing costs, fees, and expenses, was that despite the riskier nature of the credits, the LMM produced a slightly lower annualized return (9.51% versus 9.59%) than the UMM.

The conclusion that investors can draw is that, on average, the structuring of loan assets by lenders in the Business Development Companies (rows 5 and 6) that provide the direct private loans reversed the LMM yield advantage due to higher financing costs (row 7) and higher fee loads (row 8) when compared to the UMM lenders. The net result shows a small advantage, on average, to UMM lenders (row 9).

Cliffwater’s analysis of the data also provided the following insights:

- The income advantage to LMM loans relative to UMM loans was persistent over time, though spreads are regime dependent—shrinking (widening) during periods of economic strength (weakness).

- Non-accrual rates were consistently 2% higher for the LMM compared to the UMM, suggesting that credit loss differences will likely persist and give greater advantage to the UMM in the future.

- Recovery rates were consistently lower for the LMM (35%) when compared to the UMM (55%).

- Unrealized gains (losses) were highly correlated across borrower size cohorts, suggesting valuation firms and processes are very similar.

- Payment-in-Kind (PIK) was more pronounced in the UMM (8% of total income) compared to the LMM (4% of total income).

Investor Takeaways

Given the similar net returns that UMM and LMM loans have delivered, allocators should consider diversifying across borrower size cohorts. Since LLM loans are somewhat riskier, careful due diligence should be performed in terms of a lender’s credit loss history, fees/expenses, and use of leverage. Cliffwater’s Corporate Lending Fund (CCLFX), an interval fund, provides investors with exposure to both UMM and LMM loans across dozens of private lenders with attractive fees and expenses (exclusive of borrowing costs) of just 1.58% (versus UMM average fee of 4.52%), with the fee being on net – not gross – assets. Its relatively low expenses, broad diversification, and strong credit culture, are why it is the vehicle I use to gain exposure to the asset class.

Larry Swedroe is the author or co-author of 18 books on investing, including his latest Enrich Your Future.

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.