“If you’re not willing to react with equanimity to a market price decline of 50 percent two or three times a century, you’re not fit to be a common shareholder and you deserve the mediocre result you are going to get.”

That was Charlie Munger, speaking to the BBC in 2009 in the depths of the financial crisis. His point was simple: if you’re going to buy and hold equities, you have to be prepared for gut-wrenching drawdowns. They’re not rare accidents. They’re part of the deal.

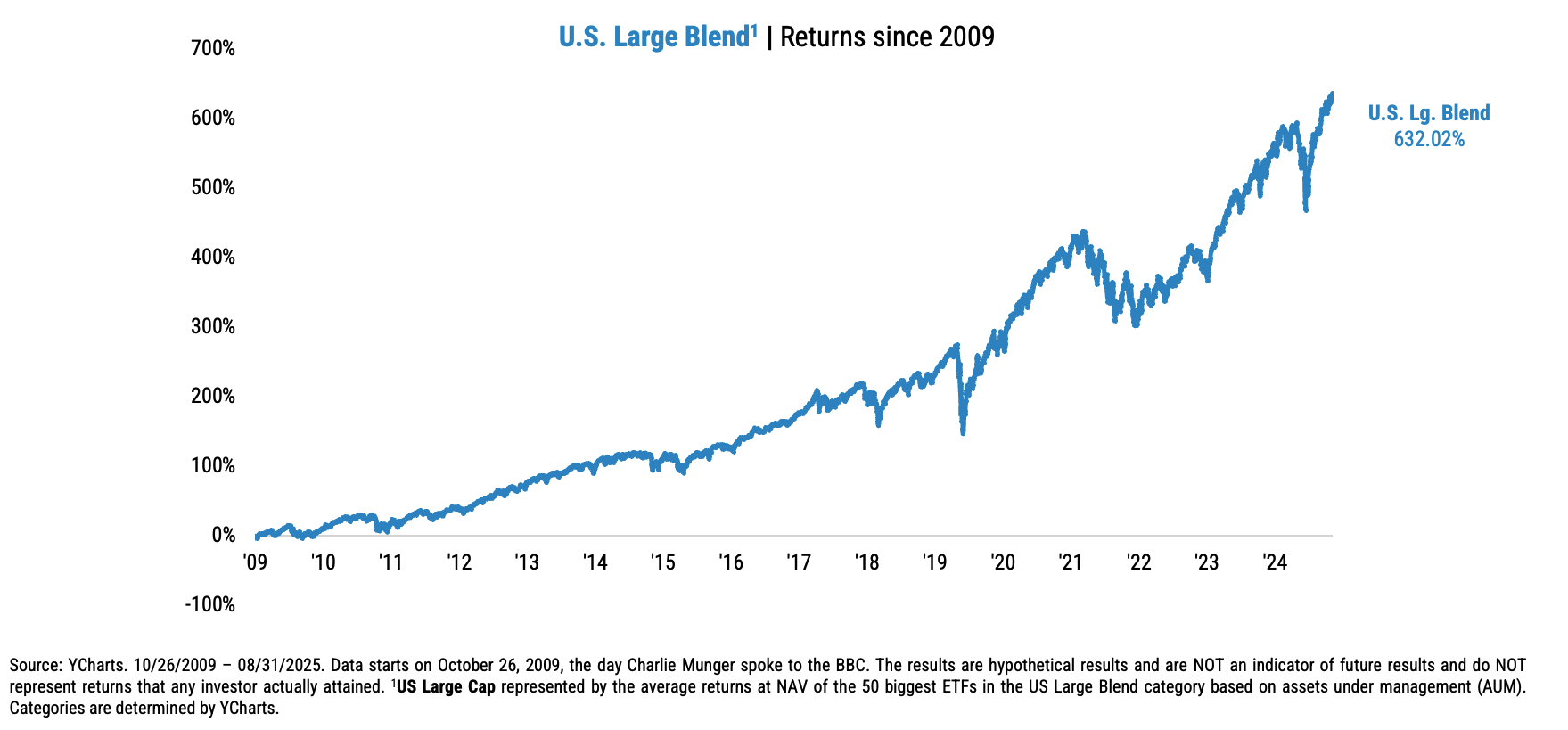

Since Munger first made that remark, the market has surged, more than tripling while experiencing only two relatively short bear markets in 2020 and 2022. Each of those quickly recovered. Investors who followed Munger’s stoic advice largely did well by holding, or even buying more, during the selloffs.

Today, phrases like “HODL” and “buy the dip” have become rallying cries for equity investors. But is this mindset always correct? Could there come a time when buying dips or holding at all costs turns out to be a mistake?

To dig deeper, let’s look at insights from Michael Mauboussin and Dan Callahan’s recent paper, Drawdowns & Recoveries: Base Rates for Bottoms and Bounces, and consider what the evidence tells us about the nature of drawdowns and recoveries.

Before beginning, if you’d rather watch the video version of this blog, make sure to subscribe to our YouTube channel! There you will find tons of more educational resources for your enjoyment. Watch here:

Big Drawdowns Are the Price of Admission

Charlie Munger was clear: if you’re a long-term equity investor, severe drawdowns are inevitable. And he’s right. The likelihood of a 50%+ decline is not just possible — it’s almost guaranteed at some point over an investing lifetime.

If you’re a stock picker, the odds get worse. Hendrik Bessembinder’s landmark study, Do Stocks Outperform Treasury Bills?, looked at over 28,000 companies from 1926 to 2024, and his findings are sobering:

- About 60% of stocks underperformed cash over their lifespan.

- Roughly 40% matched cash returns, but with more volatility.

- Just 2% of stocks accounted for 90% of the aggregate wealth creation in the market.

And the most common result for a stock? A 100% loss.

This is why Vanguard founder Jack Bogle was so adamant about indexing. “Don’t look for the needle in the haystack. Just buy the haystack.” By holding the market, investors effectively guarantee they’ll capture those rare 2% of stocks that drive long-term returns, even if the majority go to zero.

The Challenge of Holding Winners

Even if you identify one of those rare winners, holding on is far from easy. The Bessembinder data shows that six companies — Apple, Microsoft, NVIDIA, Alphabet, Amazon, and ExxonMobil — generated nearly 22% of net market wealth creation. But each of these stocks, at some point, experienced an average drawdown of around 80%.

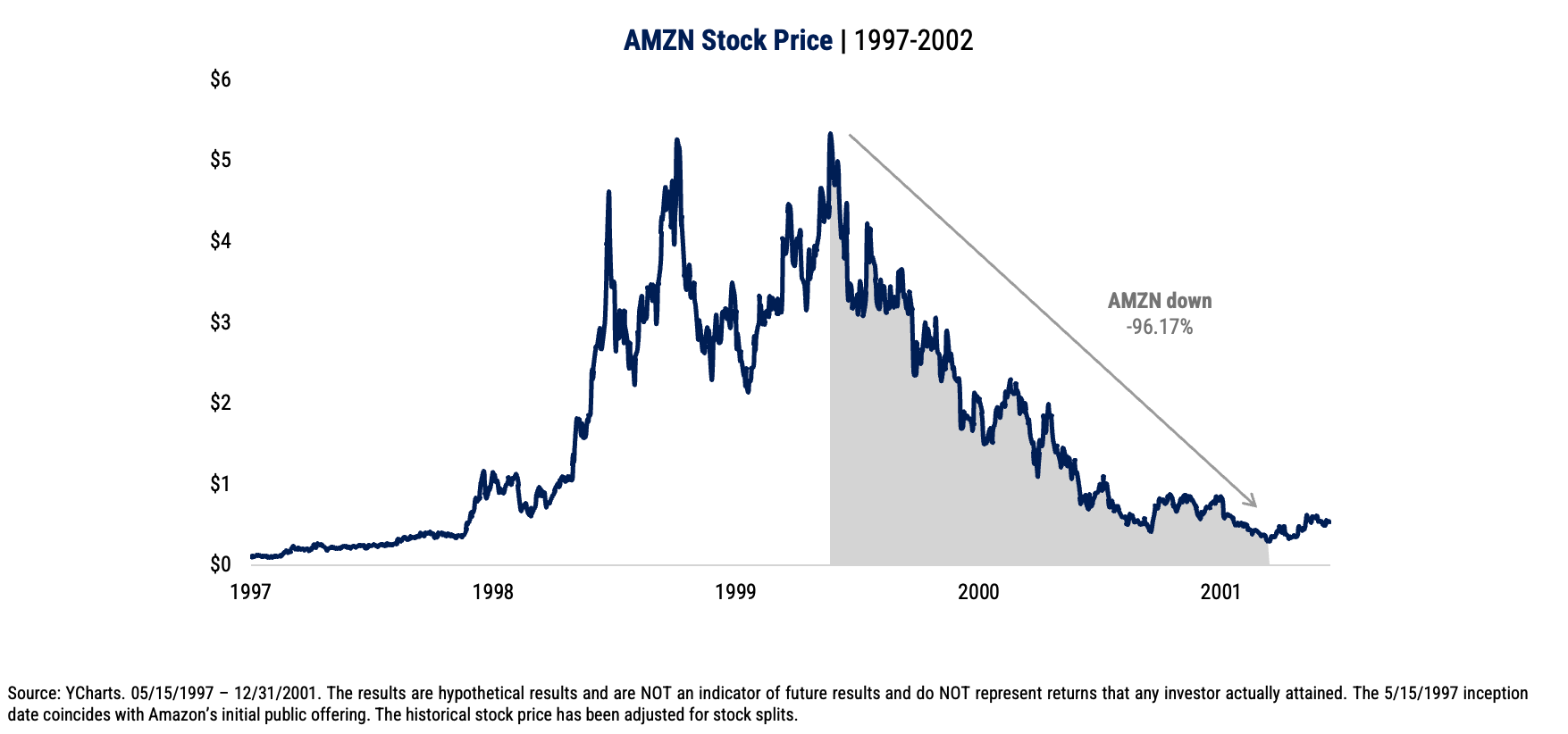

Amazon alone lost more than 95% of its value during the dot-com crash. Imagine watching your investment collapse like that in real time. Would you have had the fortitude to hold on, let alone buy more?

This brings us to an important finding: winning stocks are extremely difficult to hold through their inevitable collapses. In practice, hindsight makes it look easy, but living through the drawdowns is another story.

Lottery Ticket Dynamics

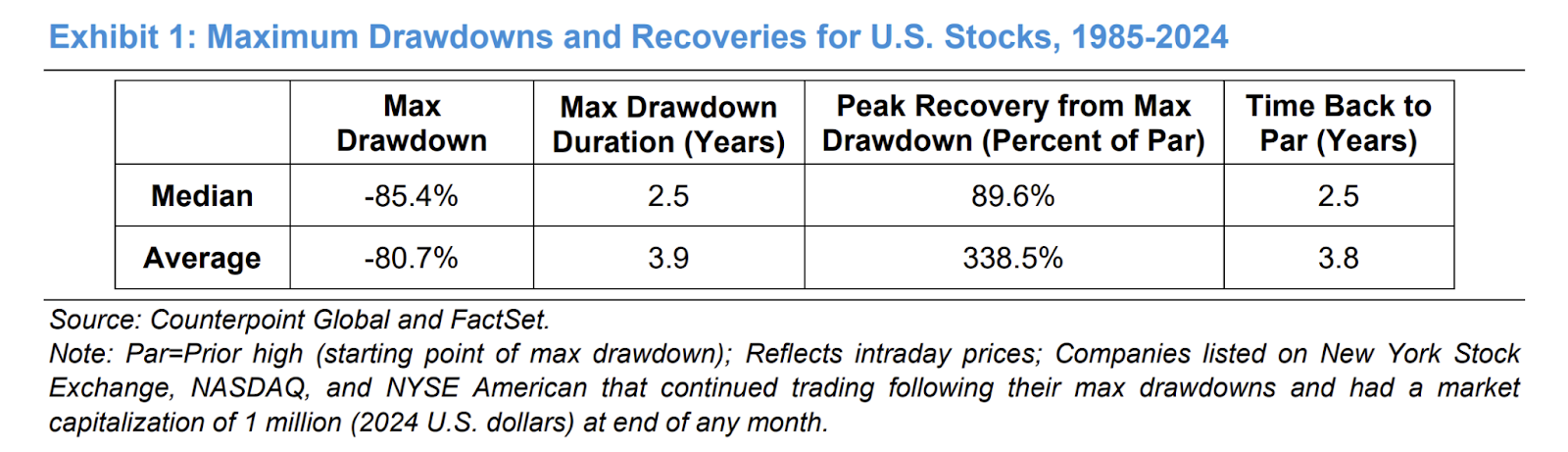

The Mauboussin-Callahan paper adds more perspective. From 1985–2024, the average drawdown of U.S. listed stocks was about 80.7%. The median drawdown was even worse, at 85.4%.

The median stock never fully recovers from its maximum loss. By contrast, the average stock appears to recover spectacularly, with peak gains of more than 300%. That gap exists because averages are driven by the extreme outliers: the handful of stocks that recover from devastating losses and then go on to soar.

The takeaway is stark: most stocks behave like lottery tickets. The median outcome is disappointing, while the occasional outlier drives the averages. For stock pickers, the odds are stacked heavily against them.

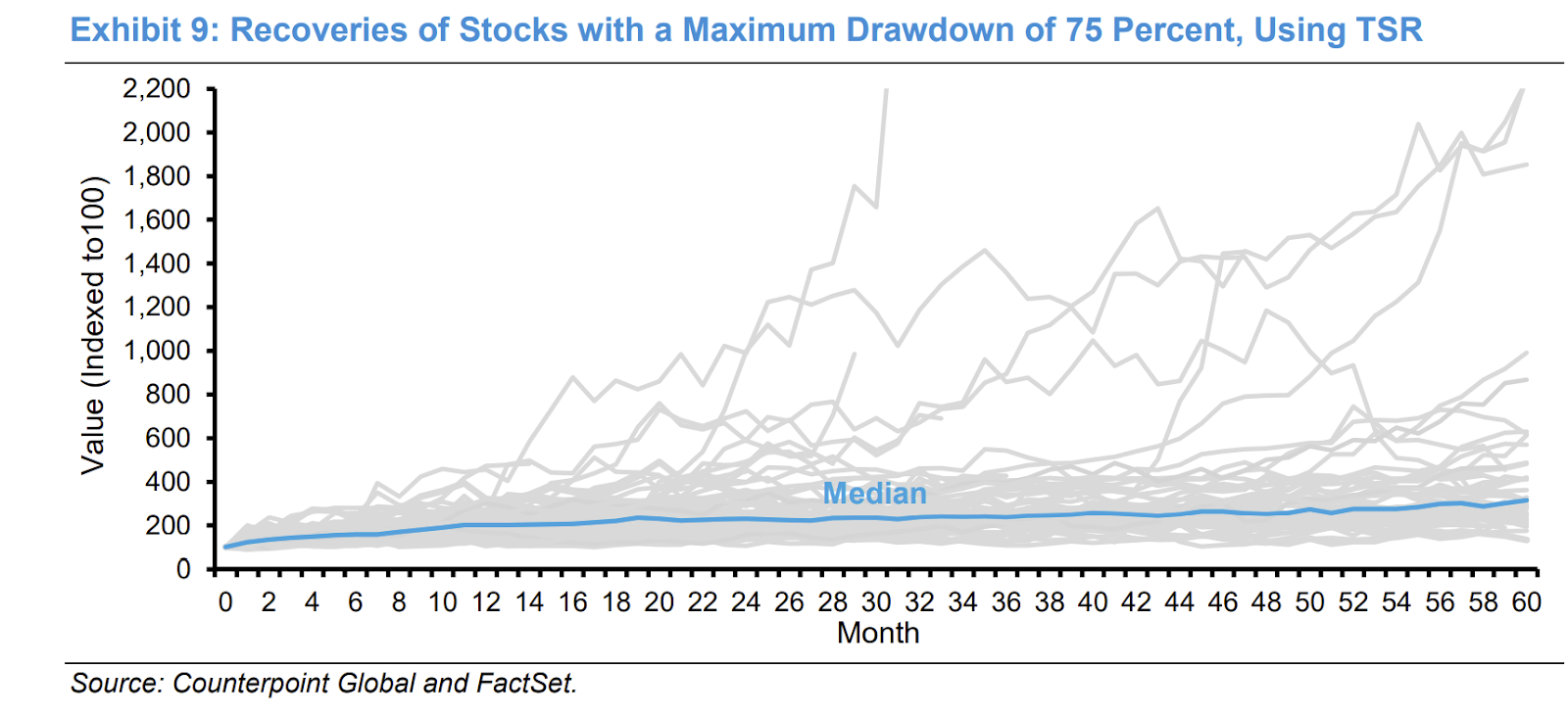

Notice, for example, in exhibit 9 that while the median stock recovers some after a drawdown of 75%, the outliers go on to have massive returns.

What Can Investors Do?

If most stocks never recover and only a handful deliver extraordinary returns, what’s the path forward? The evidence suggests several ways to stack the odds in your favor.

1. Diversify broadly.

The more stocks you hold, the better your chance of capturing the few that truly matter. At the extreme, indexing ensures you own all of them.

Now, full transparency here: We are in favor of portfolio concentration. So how does one strike a balance between diversification and factor concentration? If you’re interested in our answer, I wrote about this very topic here.

2. Use momentum as a filter.

Momentum strategies seek to own stocks that are performing well and avoid those that are collapsing. Research shows that the deeper a stock falls from its peak, the lower its probability of ever recovering. Avoiding big losers is often more important than finding big winners.

3. Focus on quality.

Sharp price declines can signal financial distress. Companies with stronger fundamentals — profitability, stability, and balance sheet health — have a better chance of avoiding terminal declines. For value investors, this means distinguishing between “cheap junk” and genuine bargains.

4. Rebalance frequently.

Rebalancing refreshes your portfolio and prevents it from getting anchored to outdated information. By acting on new signals, investors can avoid staying too long in deteriorating positions. We talked about the benefits of frequent rebalancing here.

The Bigger Picture

In conclusion, while “HODLing “can be an okay strategy at the index level, it could prove detrimental at the individual stock level. That is because median stock never actually recoups losses, while the market as a whole usually does.

On the other hand, when buying the dip, make sure there is a fundamental reason to believe that there is a reason to believe that there will be a turnaround, especially if the stocks has fallen a good amount.

Spoiler alert: According to the paper “Academic research shows that fundamental turnarounds are hard and rare”. Historically, about half of stocks do not experience any turnaround whatsoever.

In the end, investing is a game of survival. Avoiding permanent capital impairment matters more than chasing lottery-like winners. As Munger suggested, the ability to stomach deep drawdowns is part of the price of admission. But with the right portfolio design, investors can improve their odds of not just surviving the ride, but as my boss Wes Gray often says, “compounding your face off” over time.

Sources:

Bessembinder, Hendrik (Hank), Do Stocks Outperform Treasury Bills? (May 28, 2018). Journal of Financial Economics (JFE)

Mauboussin, Michael. Callahan, Dan. Drawdowns & Recoveries: Base Rates for Bottoms and Bounces. (May 21, 2025). Morgan Stanley Counterpoint Global Insights.

About the Author: Jose Ordonez

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.