Opportunism as a Managerial Trait: Predicting Insider Trading Profits and Misconduct

- Ali and Hirshleifer

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category.

Abstract:

We show that opportunistic insider traders can be identified through the profitability of their trades prior to quarterly earnings announcements (QEAs), and that opportunistic trading is associated with various other kinds of managerial and firm misconduct. The subsequent buys and sells of opportunistic insiders (insiders with high past pre-QEA profits) are substantially more profitable than those of non-opportunistic insiders. A value-weighted trading strategy based on opportunistic trading earns 4-factor alphas of over 100 basis points per month, an effect that is much stronger than has been identified in past insider trading literature, and which is substantial and significant even on the short side. Firms with opportunistic insiders have higher levels of earnings management, restatements, SEC enforcement actions, shareholder litigation, options backdating, and excess executive compensation. These findings suggest that opportunism is a domain-general managerial or firm trait.

Alpha Highlight:

“Are the corporate insiders buying or selling?”

Many investors consider the answer to this question to be an important signal, since they believe insiders can have access to non-public information earlier than others. Thus, insider actions may reflect future prospects for a company. We’ve covered research on this topic before (see links below):

- Fundamental Investors Following Insider Fillings — Beware!

- A Unique Insider Trading Signal that Generates Alpha

However, not all insider behavior matters, only some of it. But which aspects? Insiders may trade for a variety of reasons. So how can investors distinguish the profitable signals from the noise?

Distinguish “Opportunistic Insiders:”

This paper defines a specific group of insiders as being notable in this regard. “Opportunistic insiders” are those who tend to buy before public revelations of good news, and sell before bad news. This paper hypothesizes that trades of such opportunistic insiders should be more profitable than those of non-opportunistic insiders.

To investigate this hypothesis, the authors first develop a measure of “opportunistic insider trading”:

- The paper hypothesizes that those insiders who profit heavily in their past Pre-Quarterly Earnings Announcement (pre-QEA) trades do indeed trade opportunistically.

- So at the beginning of each year, rank all insiders into quintiles based on profitability of their past pre-QEA trades; specifically, the pre-QEA means 21 trading days before the QEA ending 2 days before the QEA.

- The insiders in the highest quintile are defined as “opportunistic insiders.” They seem to have done the best historically.

Long/Short Strategies:

The authors examine the performance of a monthly long/short strategy that buys after an insider buys and shorts after an insider sells, for each of the five quintiles.

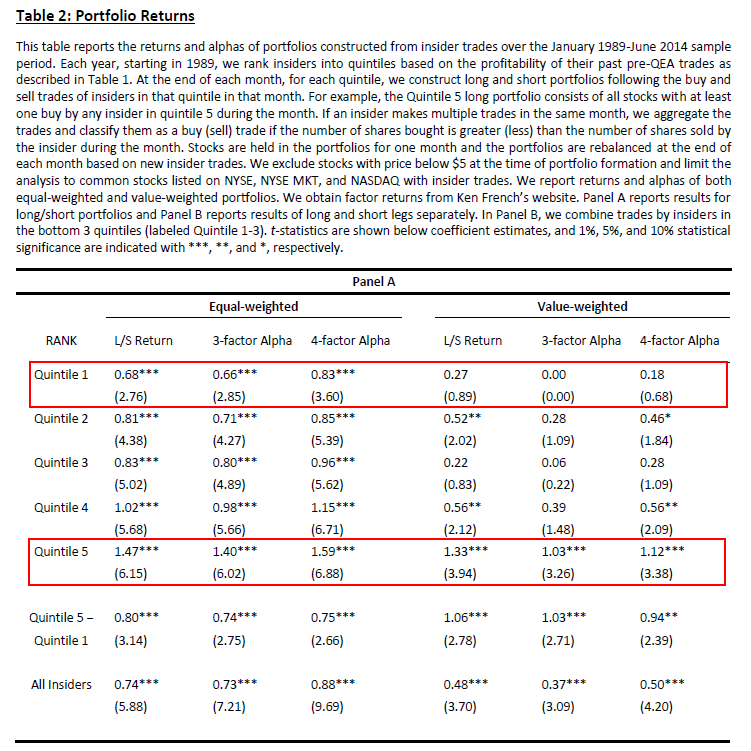

The below table shows the results of the long/short portfolios constructed from insider trades from 1989 to 2014. The results show that “opportunistic insiders,” in quintile 5, earn higher profits on their subsequent trades than other insiders from quintiles 1~4.

- For example: the long-short strategy constructed using trades of insiders from quintile 1 generates an insignificant value-weighted 4-factor alpha of 0.18% per month, whereas the same strategy constructed using trades of opportunistic insiders (from quintile 5) generates a significant alpha of 1.12% per month. The difference between top and bottom quintile portfolio alphas is 0.94% per month.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Takeaways:

Don’t look at insider actions in a vacuum; consider the track record of the insider, and focus on those who, historically, have been opportunistic. Past profitability of pre-QEA trading is a powerful way to distinguish opportunistic from non-opportunistic insiders. And it seem that pre-QEA profitability is a strong predictor of future performance.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.