One of the recurring themes we see in our research is the concept of “no pain; no gain.” Or as Corey Hoffstein says, “No pain, no premium.” Cliff Asness may put it best when he says that some strategies require that you hold on to them “like grim death.”

Bottom line: nothing is easy in financial markets.

Pain is viewed slightly differently for academic economists versus the rest of us. For academic economists, pain is typically tied to some notion of “fundamental risk” that is priced in a market equilibrium with rational participants trying to maximize their expected lifetime consumption subject to some concave utility function. In other words, a fantasy land, but still probably useful. For others, the pain of investing is rooted in some sort of problem stemming from irrational market participants. This pain manifests itself as career risk, regret, loss aversion, and so forth. These forms of pain are tougher to model, but they also represent investment “pain” to many.

What we find in this analysis is the following:

- Trend-following “works” in the sense that one has historically been able to capture a vast majority of the upside in a stock market, while simultaneously minimizing the threat of monster drawdowns.

- Trend-following is fraught with behavioral challenges. The strategy can deviate wildly from buy-and-hold benchmarks and so-called whipsaws are commonplace.

- The behavioral challenges associated with trend-following are so severe that it is recommended that many investors should avoid trend-following strategies.

Welcome to the realities of equity trend-following. An open secret that is simple, but not easy (sound familiar?).

A PDF version of this is available here.

Data Details

Before we dive into the results it is important to understand some basics related to our data source, assumptions, and methodologies deployed.

We analyze the total return equity index series from Global Financial Data (GFD) for countries with the longest track record of monthly returns in the GDF database. The analysis runs from 1/1/1927 to 5/31/2019 and reflect total returns and are gross of any fees.(1) All returns are in USD.

The countries analyzed include the following:

- AUSSIE = Australia ASX Accumulation Index-All Ordinaries

- BRUSSELS = Brussels All-Share Return Index (w/GFD extension)

- CANADA = Canada S&P/TSX-300 Total Return Index

- FRANCE = France CAC All-Tradable Total Return Index

- GERMANY = Germany CDAX Total Return Index (w/GFD extension)

- JAPAN = Japan Topix Total Return Index

- US = S&P 500 Total Return Index (w/GFD extension)

- UK = UK FTSE All-Share Return Index (w/GFD extension)

- _TREND = Robust Trend following rules applied (50% 12-month SMA and 50% 12-month Time Series Momentum). Details here. Cash proceeds are assumed to earn the Treasury Bill rate.

Additional details are available in the Appendix(2)

Why is Trend-Following Interesting?

To begin, we’ll start with the standard issue analytics: summary statistics, an invested growth chart, and the drawdown profile. We compare the buy and hold strategy (e.g. AUSSIE) against trend-followed results (e.g., AUSSIE_TREND). We also include the total return series for Treasury Bills and 7-10 Year Treasury Bonds as a point of reference throughout.

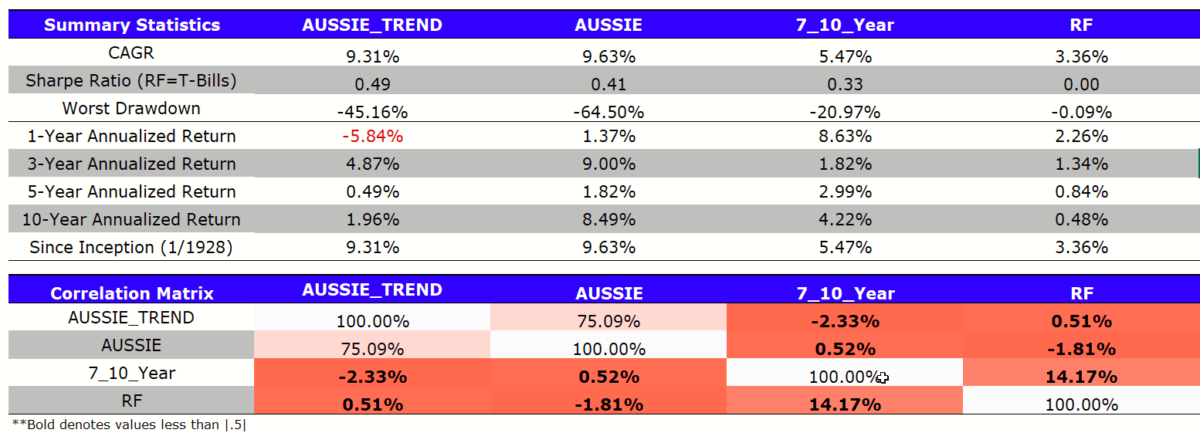

Australia

Summary stats:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

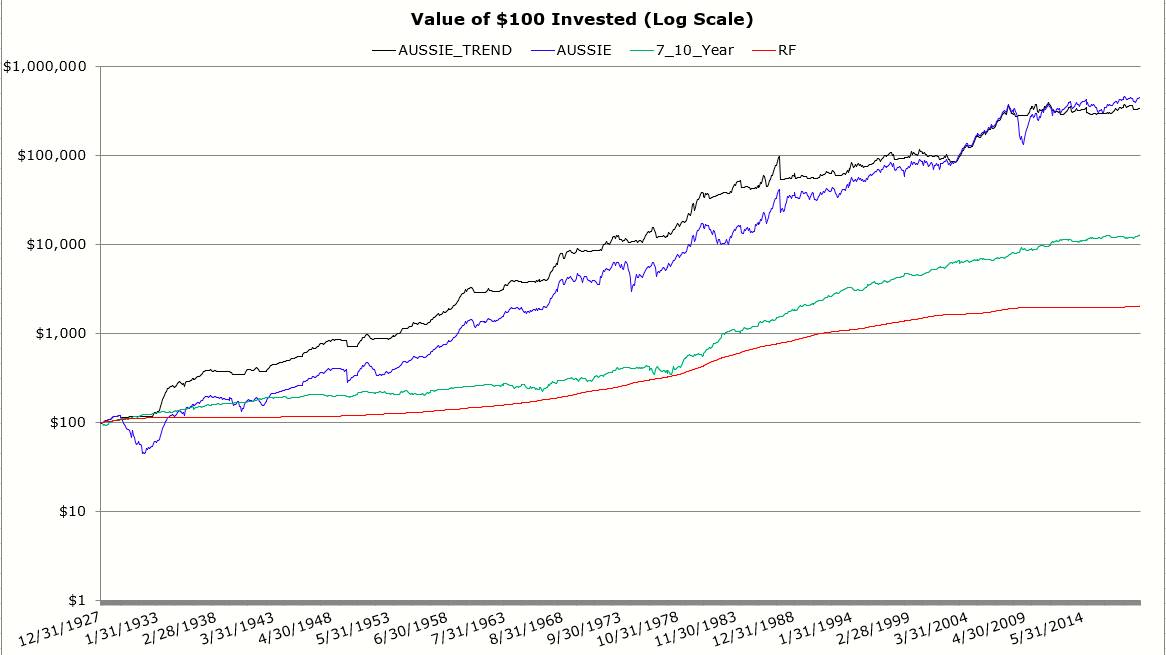

Invested growth:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

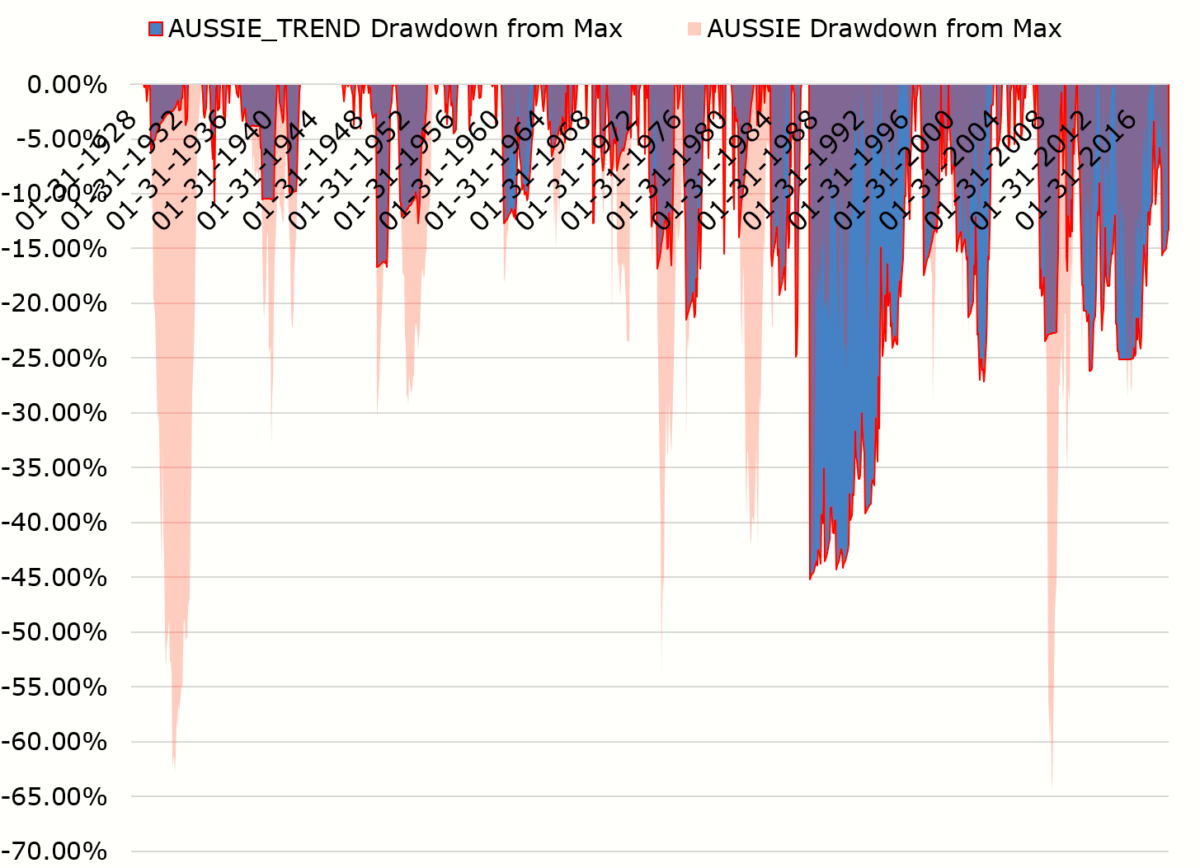

Drawdowns:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Summary:

- Similar returns with a less severe drawdown profile.

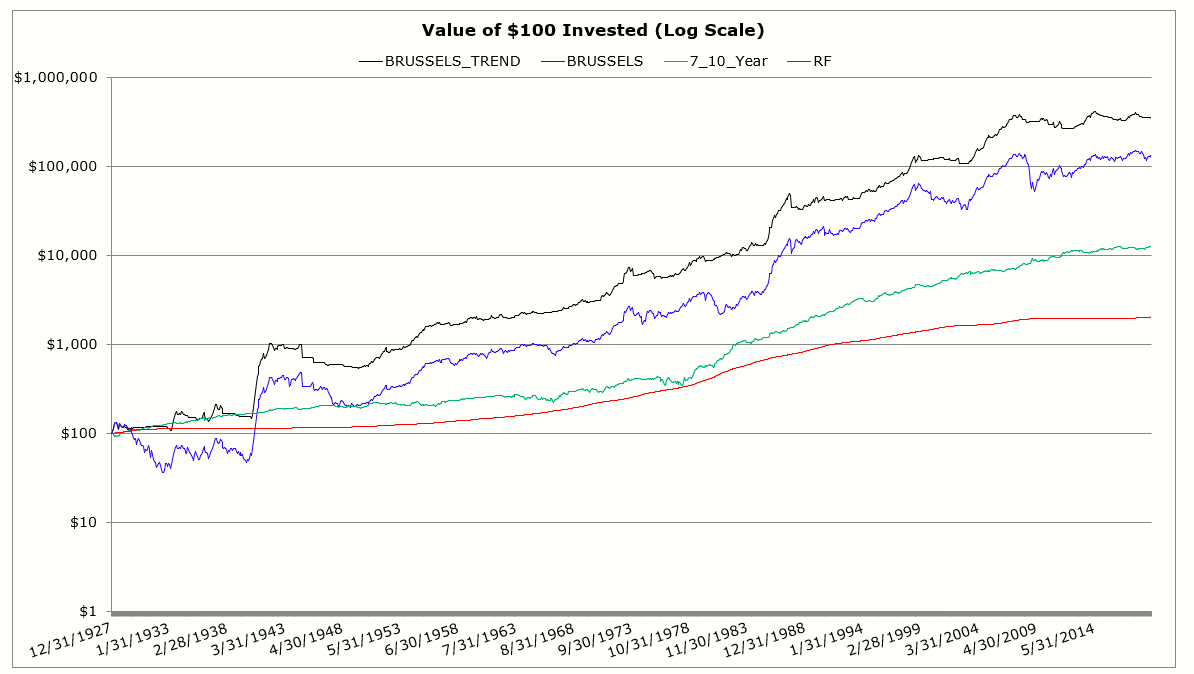

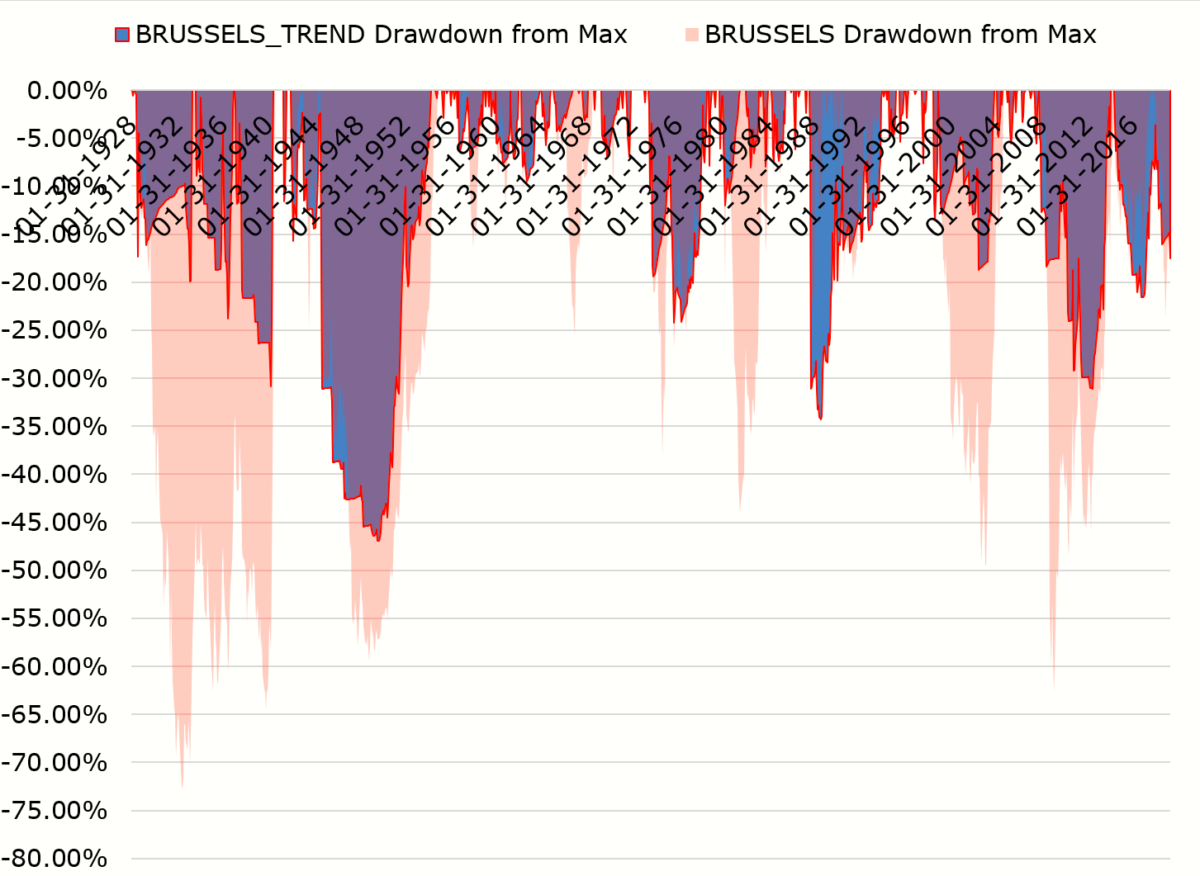

Brussels

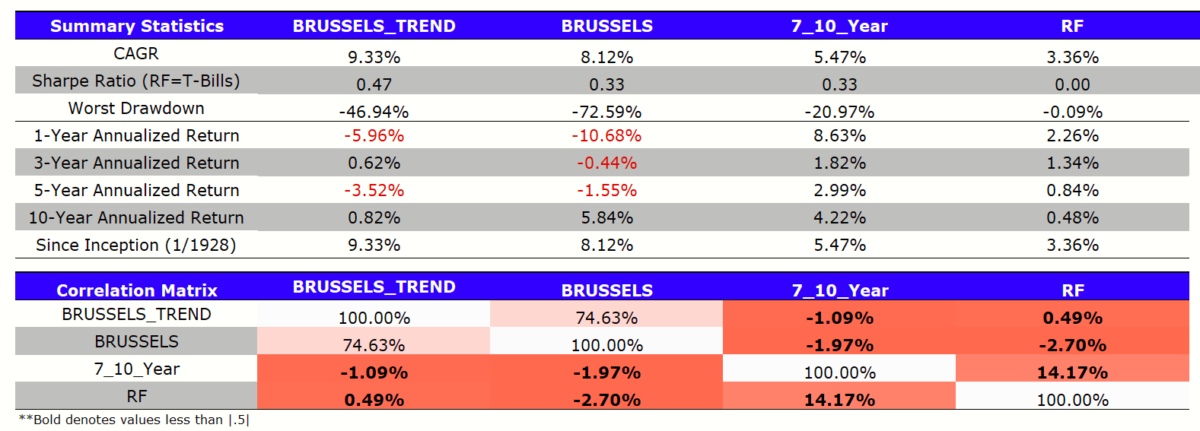

Summary stats:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Invested growth:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Drawdowns:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Summary:

- Similar returns with a less severe drawdown profile.

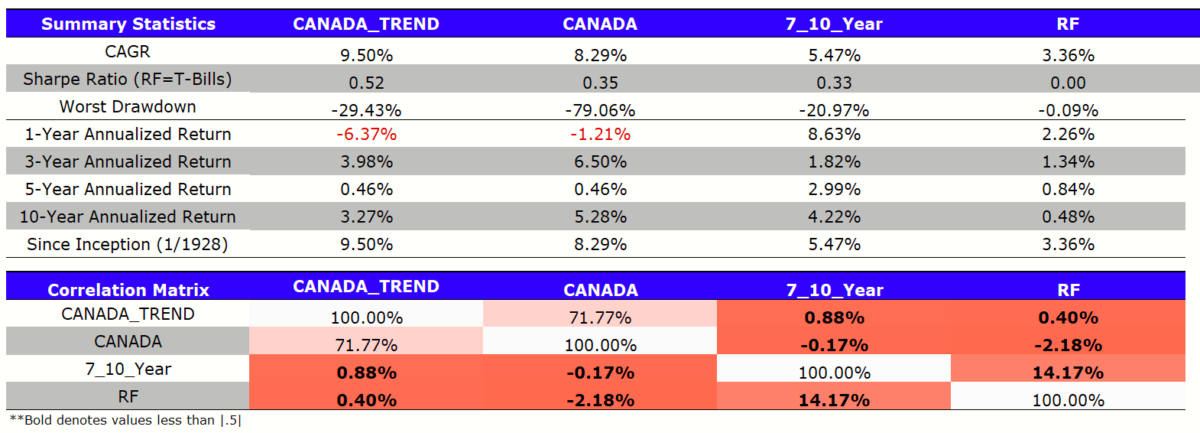

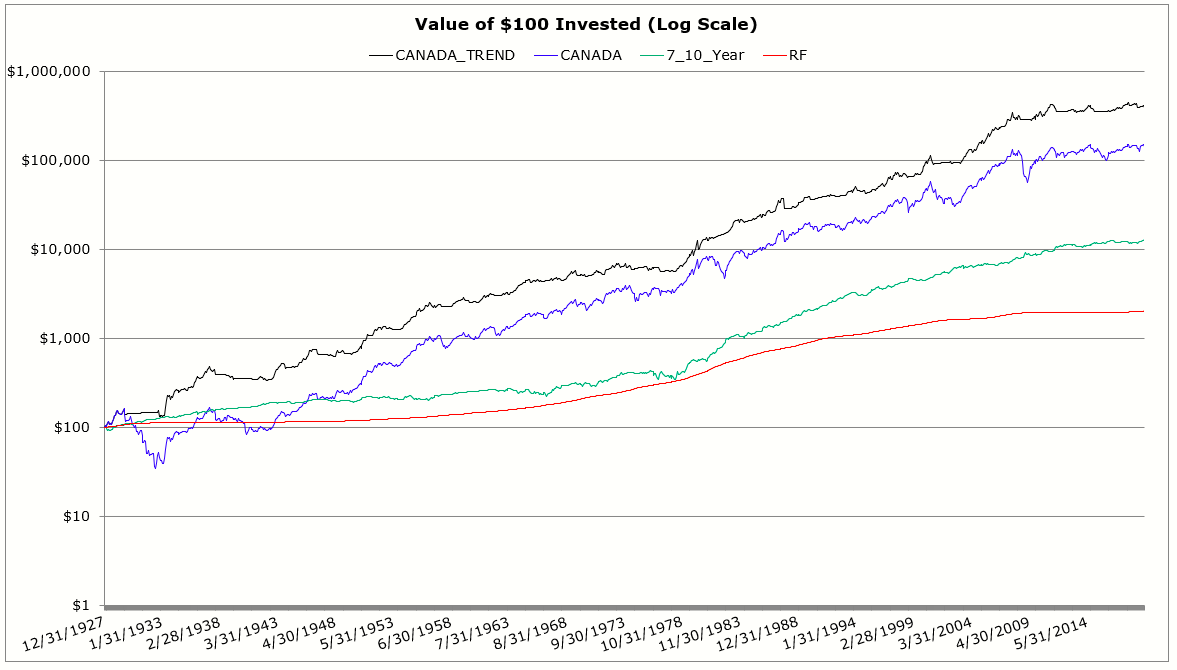

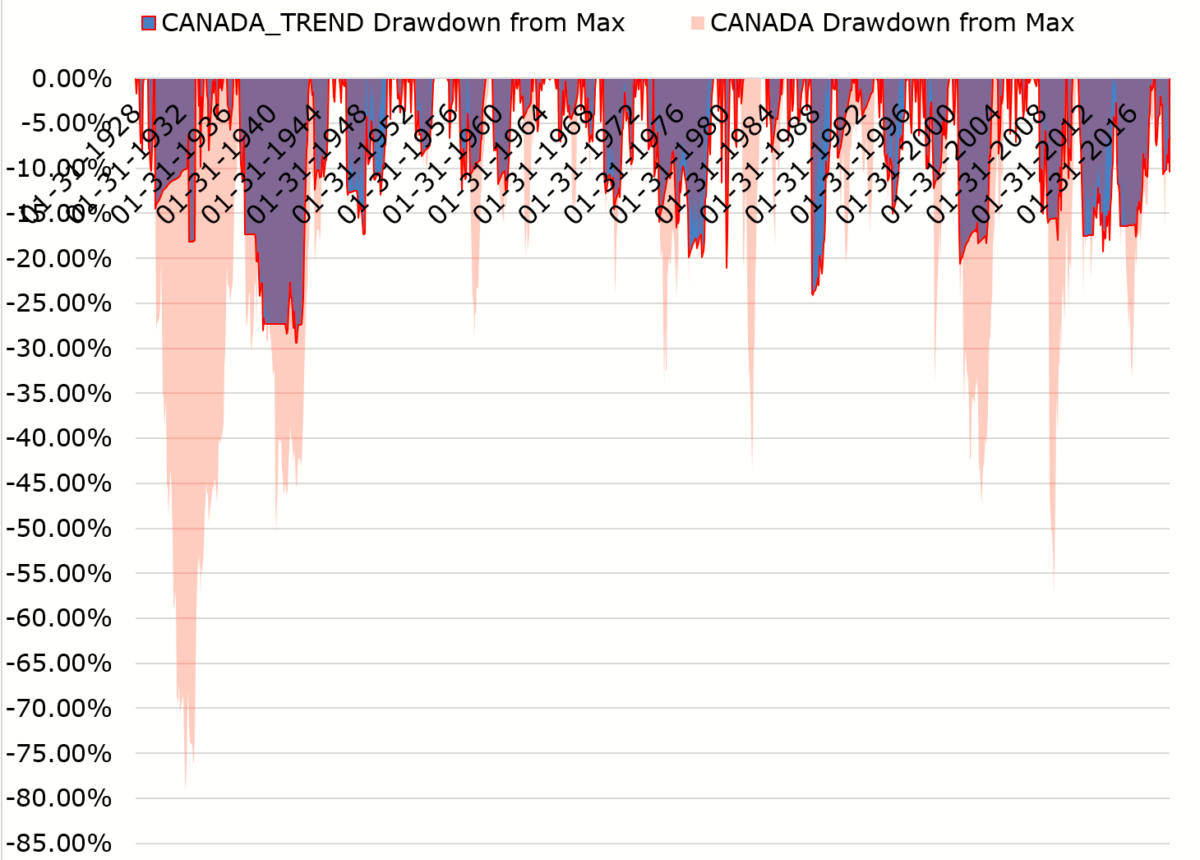

Canada

Summary stats:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Invested growth:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Drawdowns:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Summary:

- Similar returns with a less severe drawdown profile.

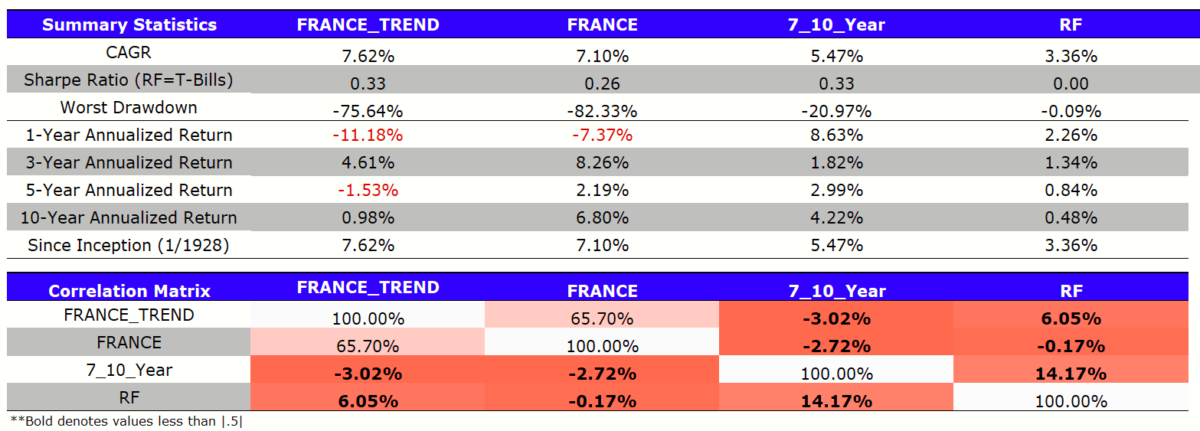

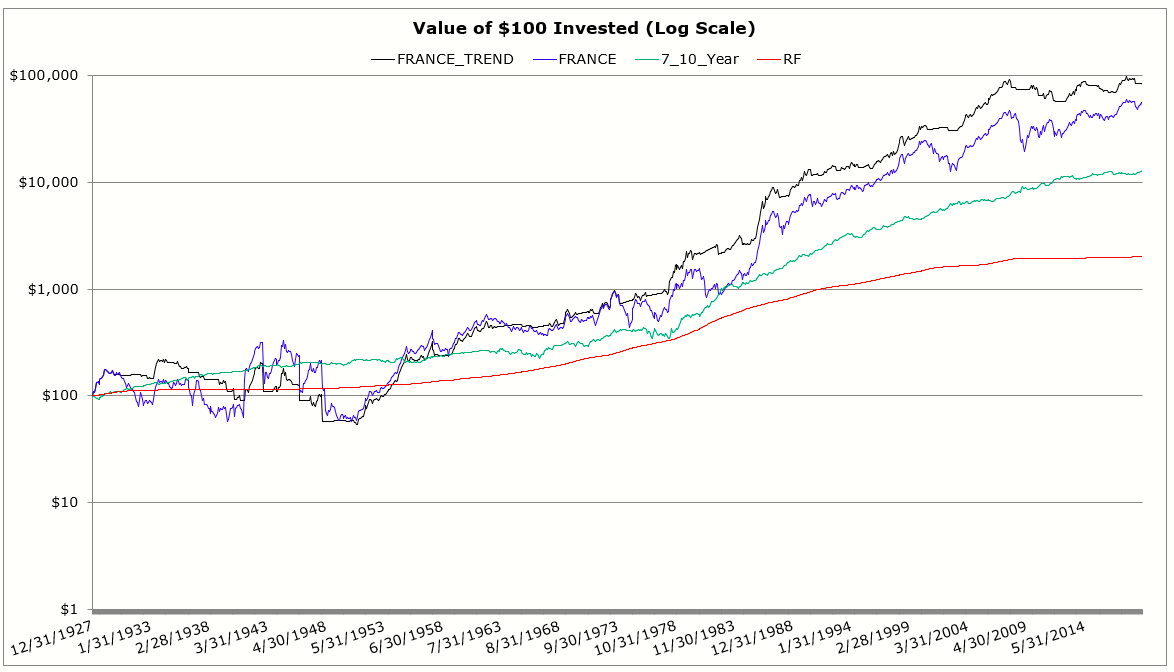

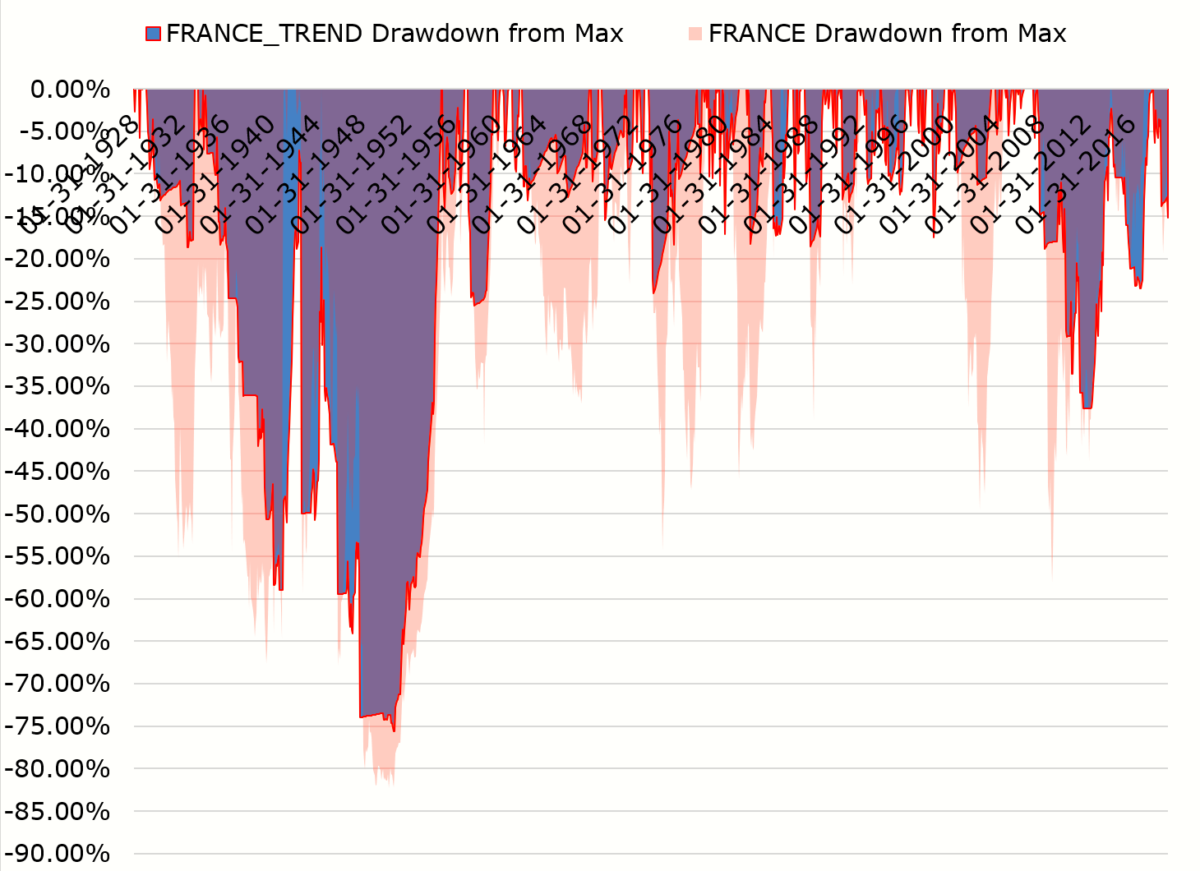

France

Summary stats:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Invested growth:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Drawdowns:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Summary:

- Similar returns with a similar drawdown profile.

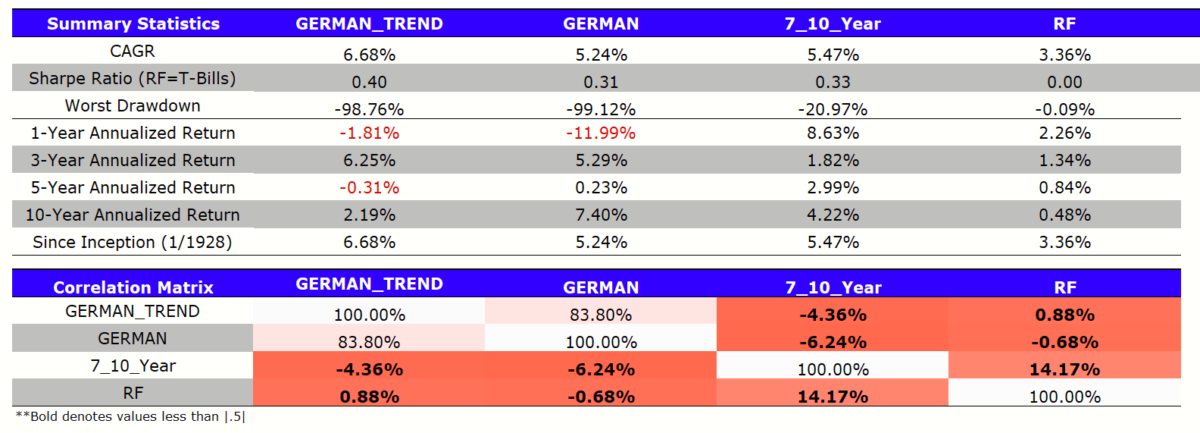

Germany

Summary stats:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

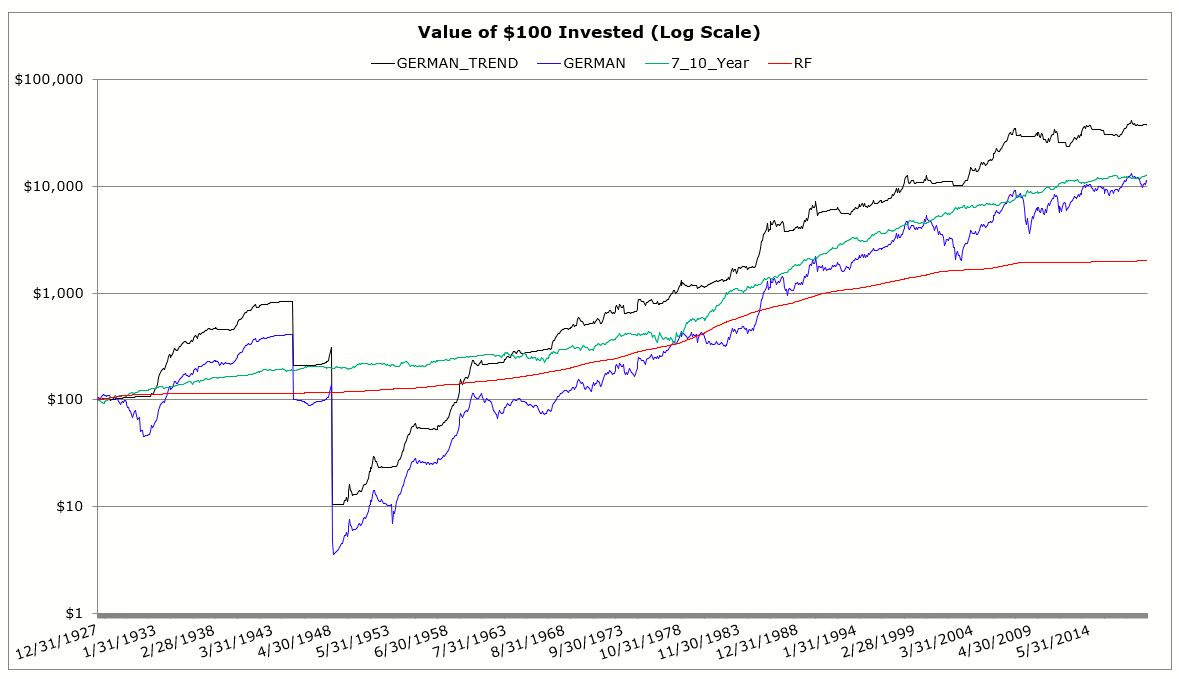

Invested growth:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

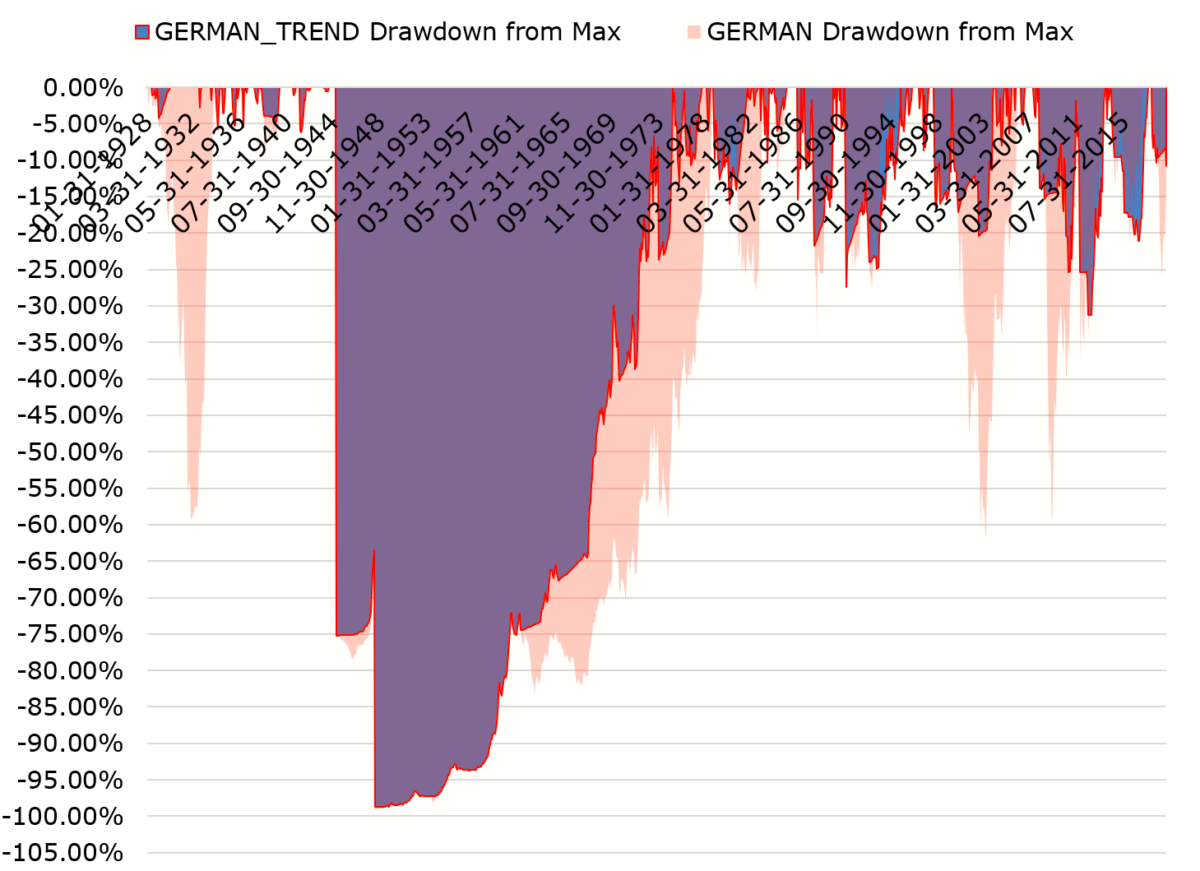

Drawdowns:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Summary:

- Similar returns with a similar drawdown profile.

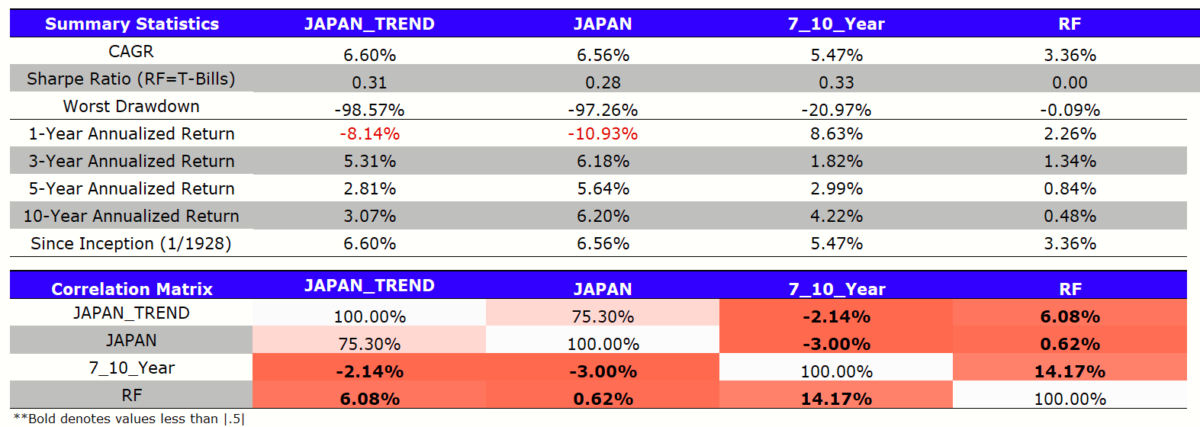

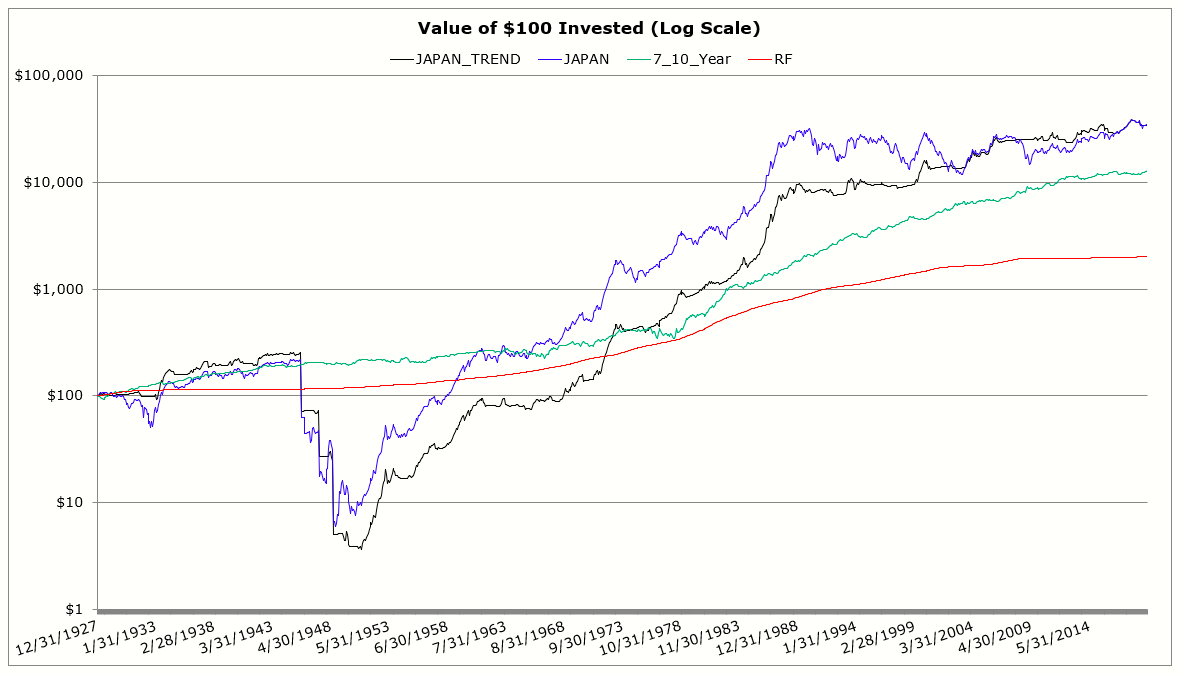

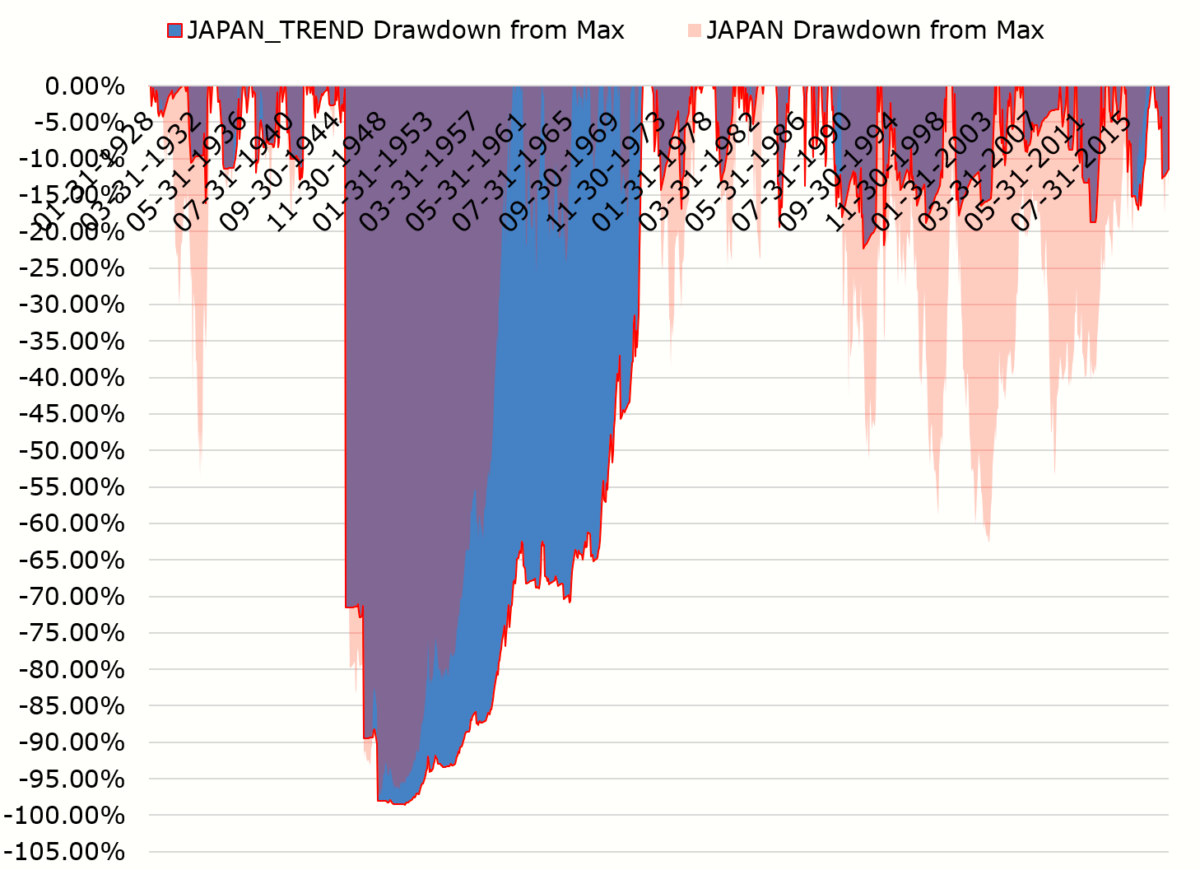

Japan

Summary stats:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Invested growth:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Drawdowns:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Summary:

- Similar returns with a similar drawdown profile.

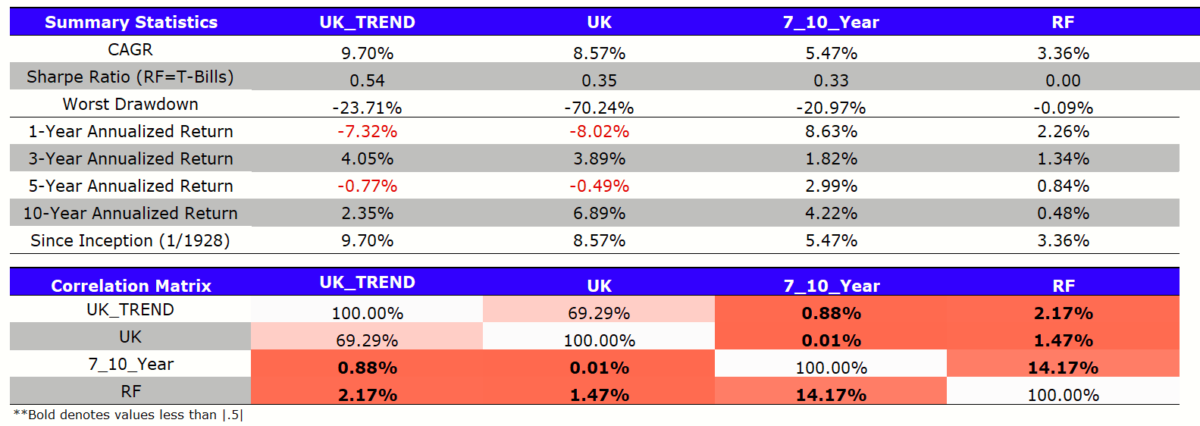

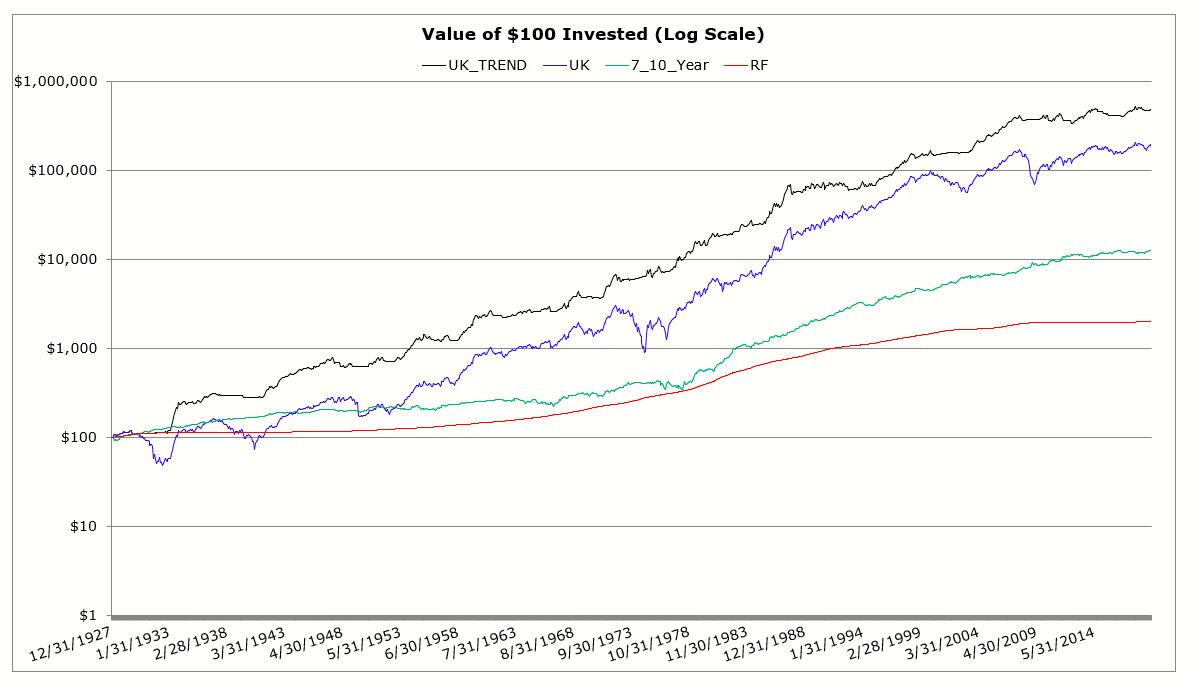

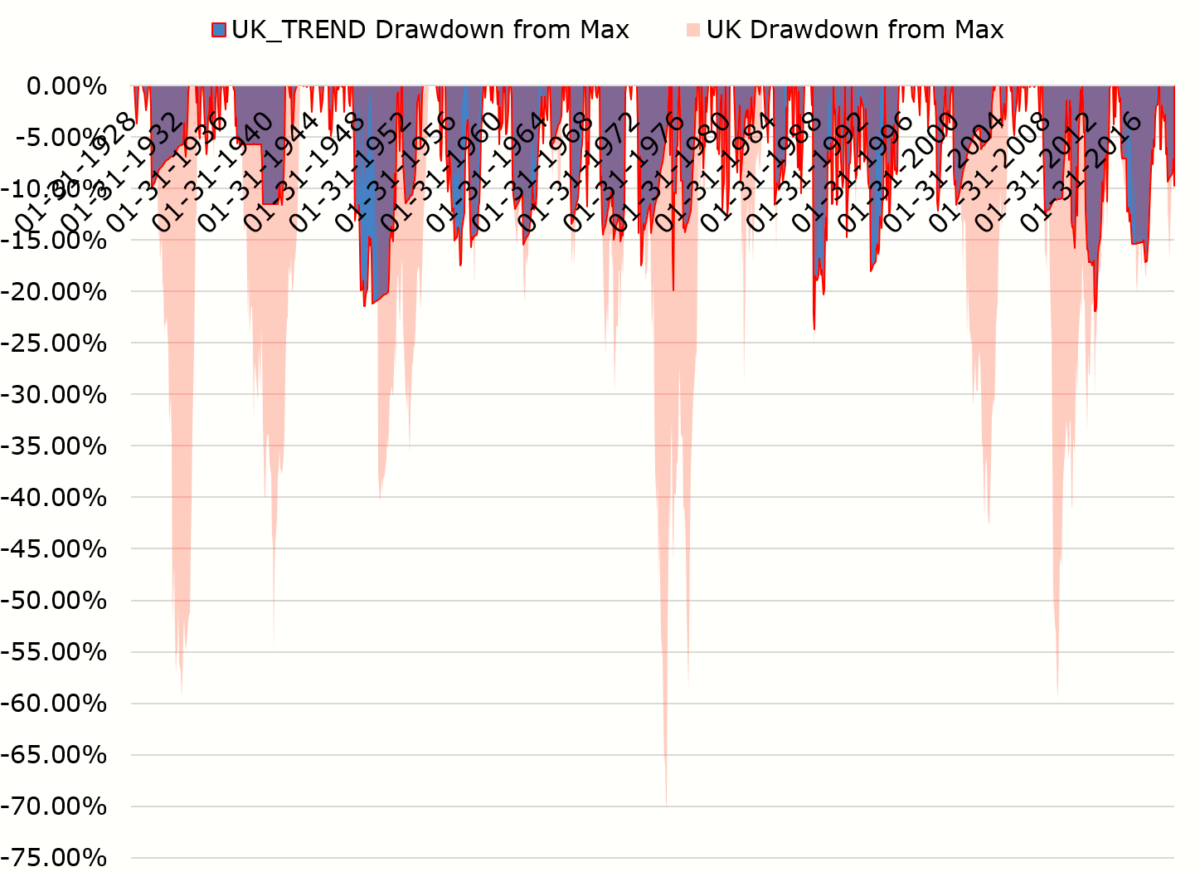

UK

Summary stats:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Invested growth:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Drawdowns:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Summary:

- Similar returns with a less severe drawdown profile.

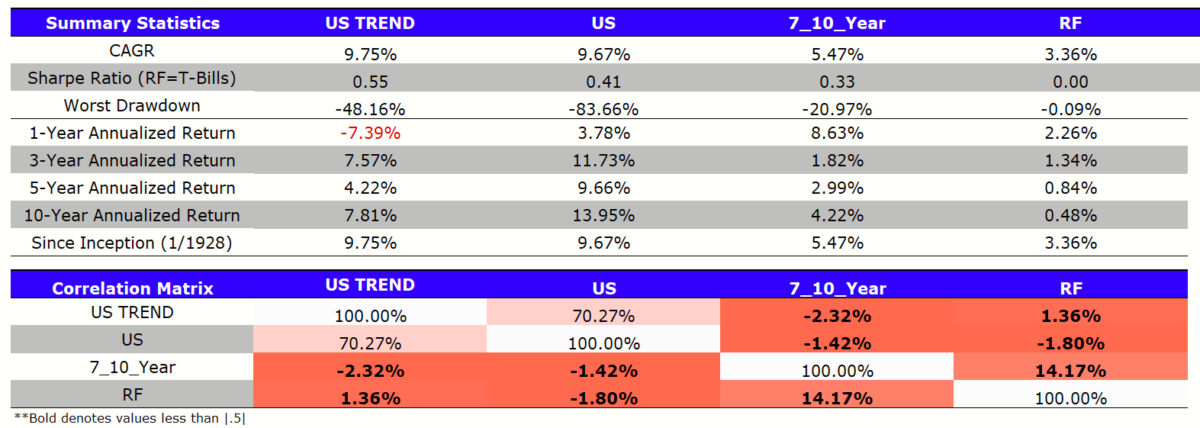

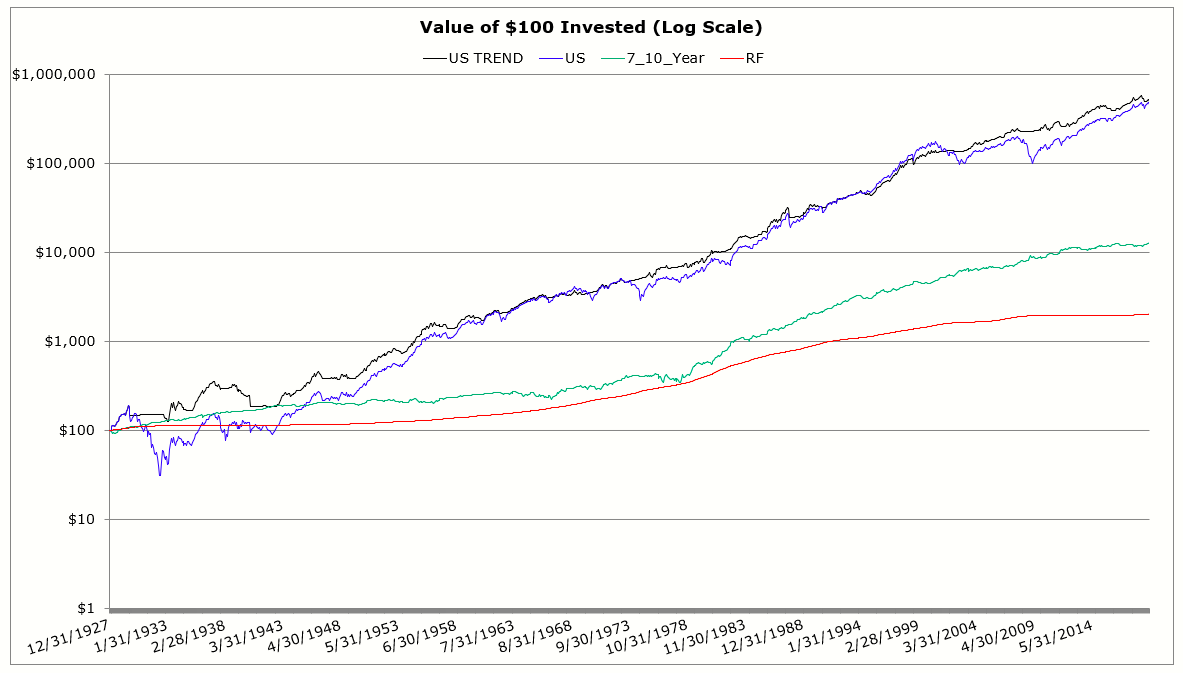

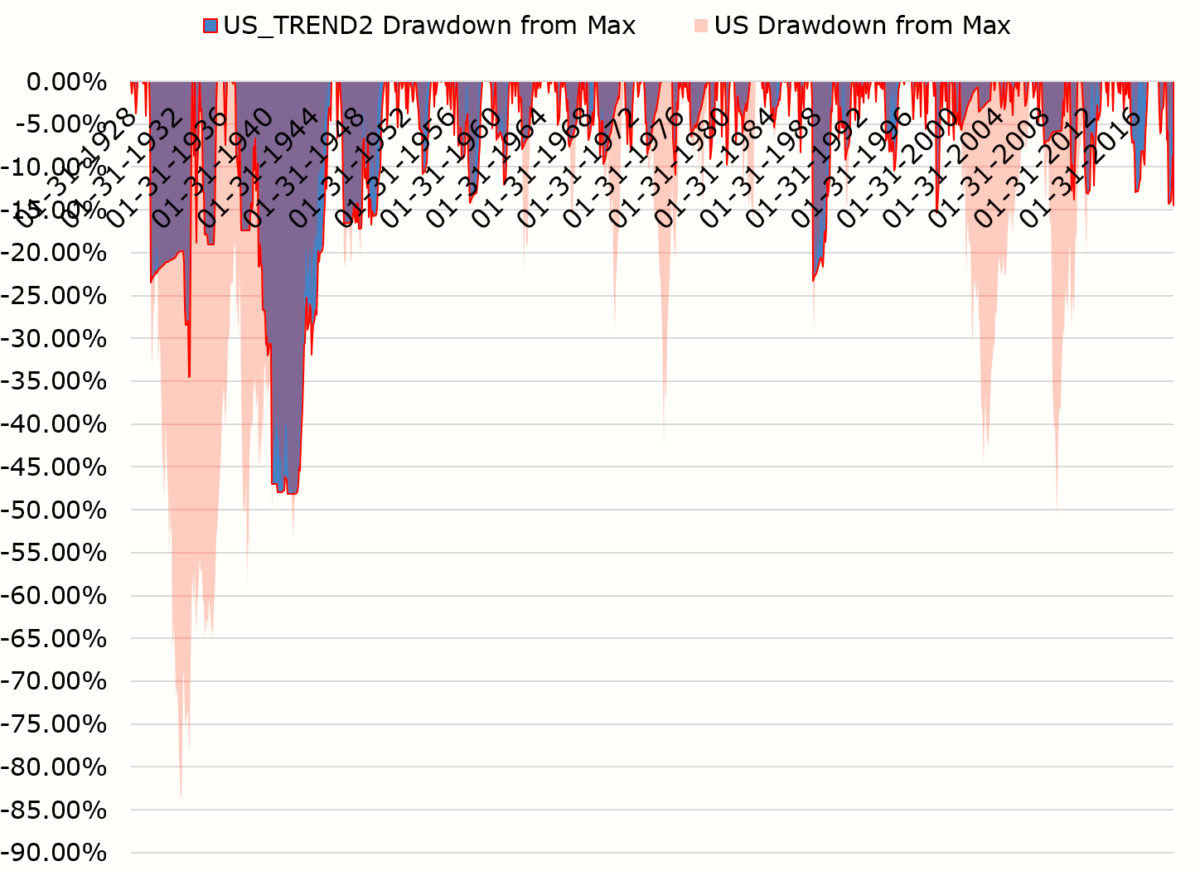

US

Summary stats:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Invested growth:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Drawdowns:

Summary:

- Similar returns with a less severe drawdown profile.

Why is Trend-Following Challenging?

The analysis above might be compelling for an investor focused on participating in meaningful stock market upside potential while minimizing the impact of epic drawdowns.(3) Let’s assume for a moment that one believed these results will hold out of sample in roughly the same manner.

The next question, while seemingly trivial, is arguably the most critical to an investor’s success: Can you stick with the strategy?

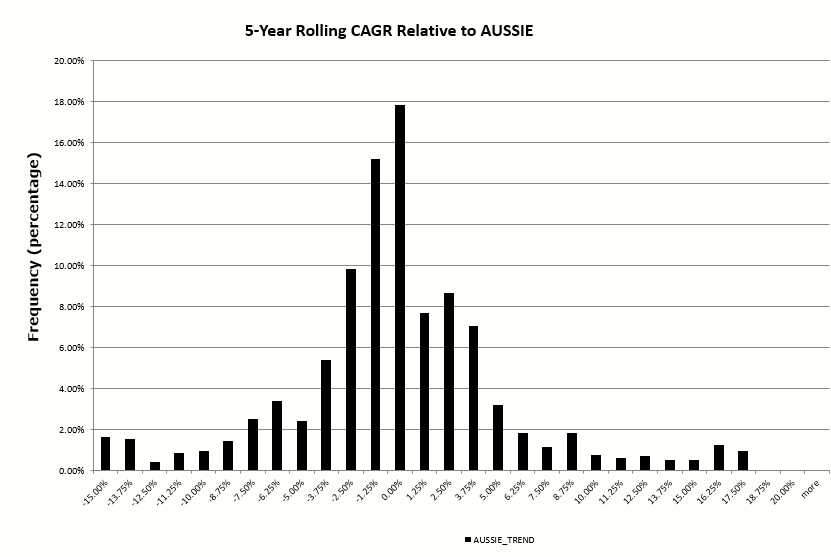

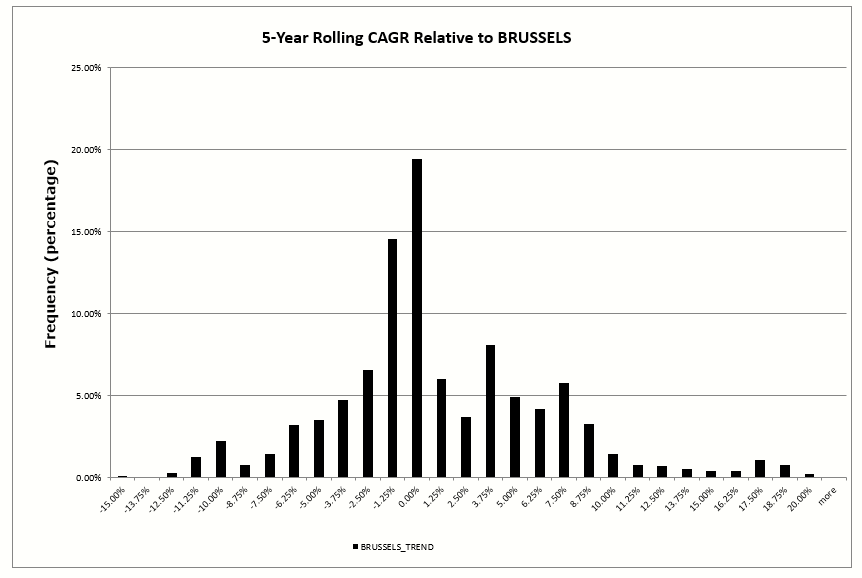

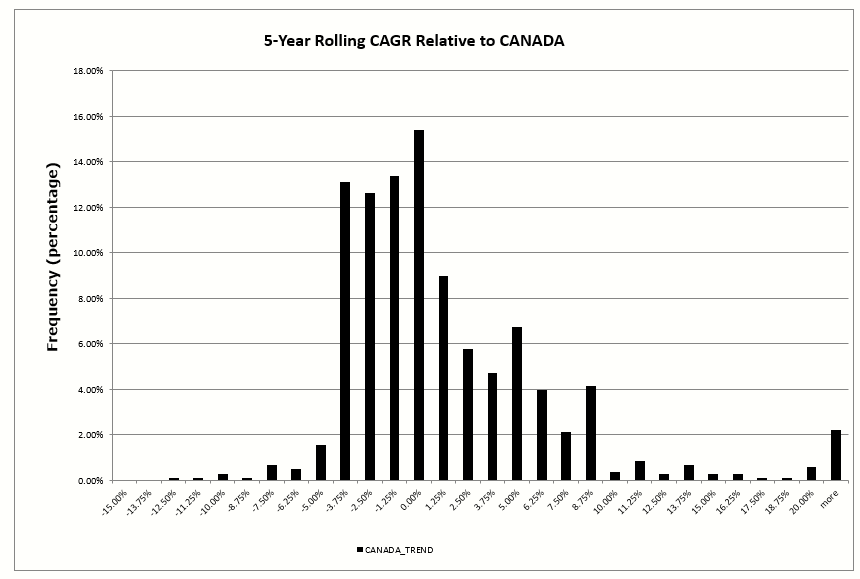

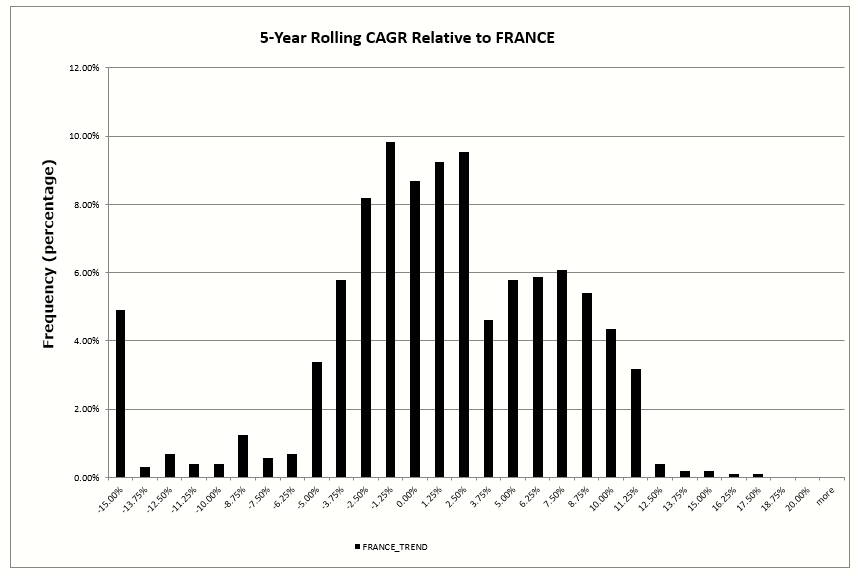

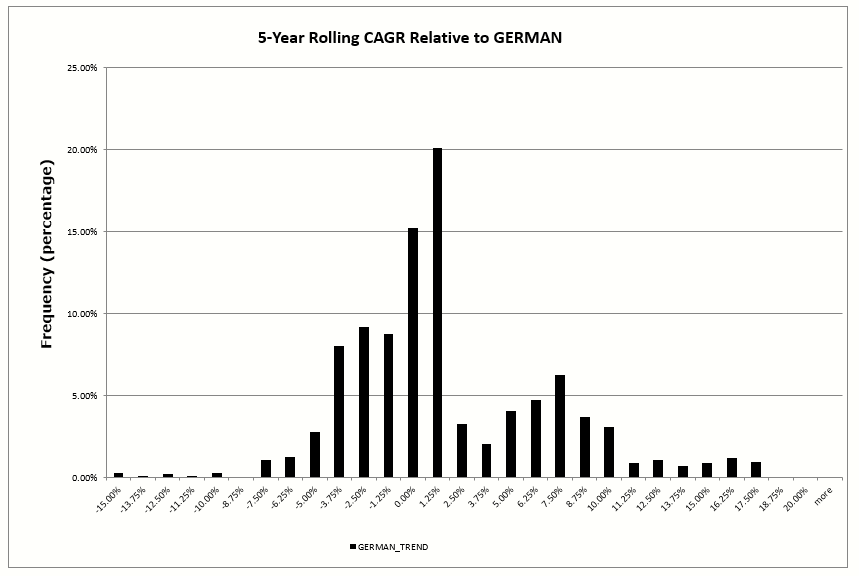

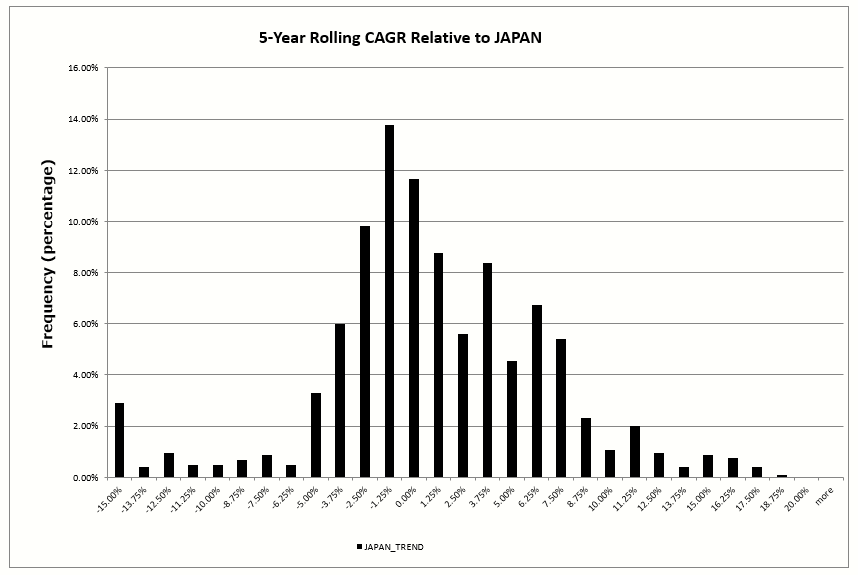

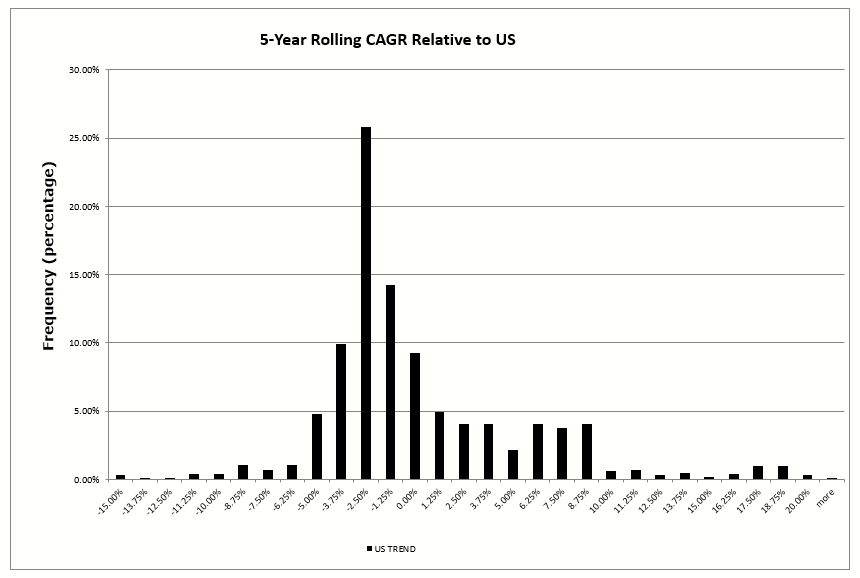

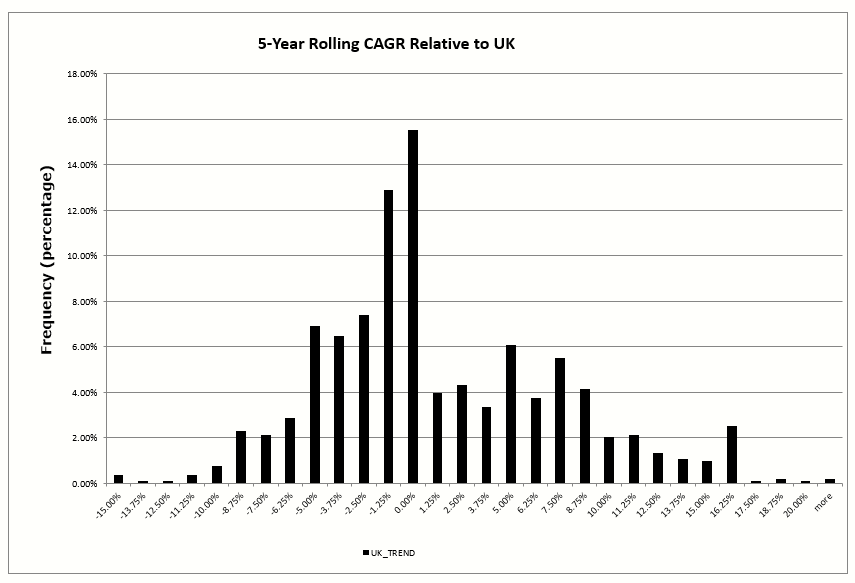

While sticking to a strategy seems easy after looking at the charts and evidence above, actually investing in a strategy in real-time can be behaviorally challenging. One way to assess the behavioral challenge of the basic long-term equity trend strategy outlined above is by examining the relative performance of the trend following strategy against the buy-and-hold strategy over 5 year rolling periods. 5 year is arguably a period of time where an underperforming strategy will test the will of most investors. We also recognize that buy-and-hold is probably not the appropriate benchmark for a strategy that holds equity less than 100% of the time. That said, while a buy-and-hold benchmark is theoretically not the correct benchmark for a trend-followed equity strategy, this benchmark is often the anchor in many investor’s minds and therefore captures the concept of “behavioral pain” in a more realistic fashion.(4) Please note that these are annualized figures in the histograms. So if you see a -15% observation that implies the strategy underperformed by 15% for 5 consecutive years, in other words, the spread in total returns is over 100%!

Australia

Brussels

Canada

France

Germany

Japan

US

UK

Summary

The relative performance of trend-followed equity strategies to buy and hold equity strategies on a rolling 5-year basis will test the will of any investor. Also, the bulk of the distribution is negative for most countries, which means that over most 5-year rolling periods one can expect to underperform the buy-and-hold counterpart.

The statistics above are a simple way of highlighting that the “behavioral edge” is critical for success as an equity trend-follower.(5)

Oh…but It Gets Worse…

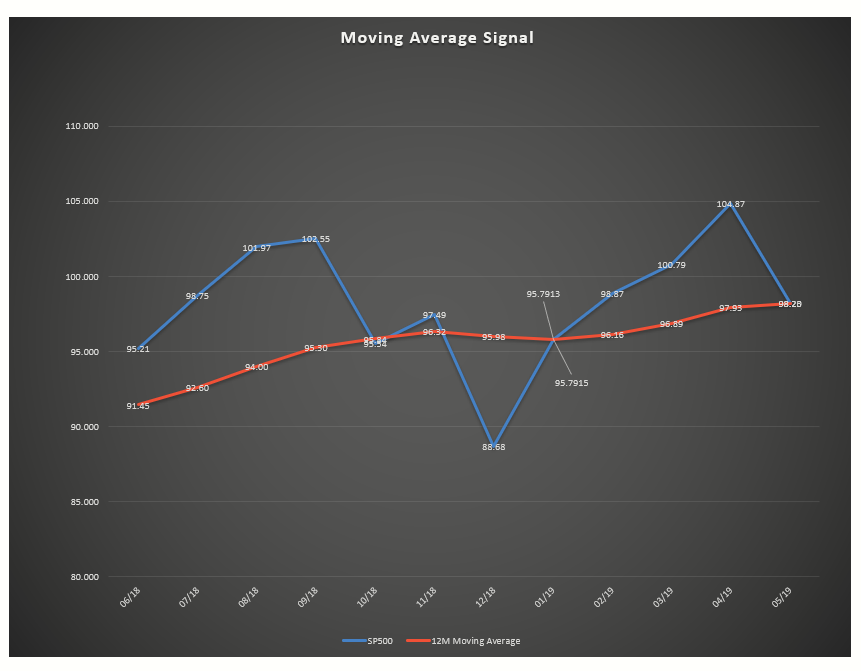

One of the most challenging aspects of trend-following strategies is the dreaded “whipsaw”. A whipsaw is a situation where a trend-following rule suggests you get out of the market, times passes, and then the trend-following rule has you get back in the market, but at a higher price than your exit price.

Here is a recent example of multiple “whipsaws” in the S&P 500 Index. Red represents exits and light blue represents entry points. Note that there have been 2 whipsaw events in the S&P 500 Index using the 12-month moving average.

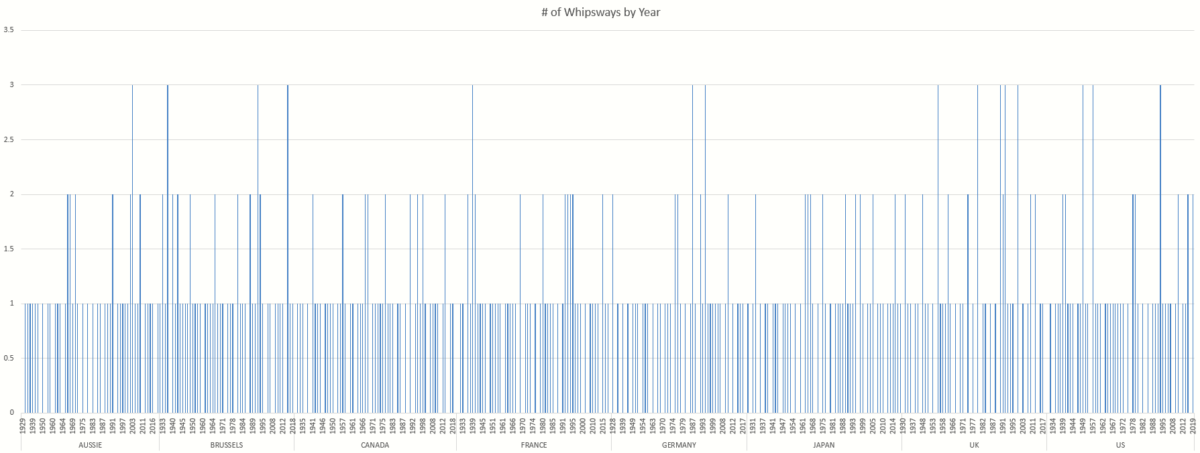

Whipsaws across countries and over time

To get a broader perspective on whipsaws we look across country and time. Here we map the number of trend triggers classified as a “whipsaw” by the year/country in which the whipsaws occur:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

The results highlight that having 2 or 3 whipsaws in a given year, while rare, are not uncommon (unfortunately!).

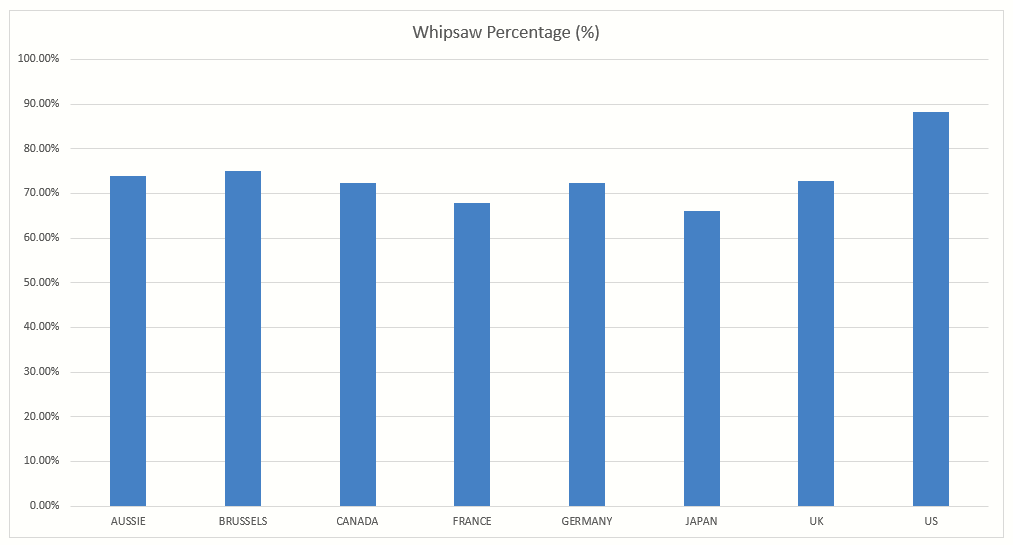

Probability of whipsaws by country

Next is a chart that maps out the probability of a whipsaw event, given you have had a trend-following trigger event:

The sad story from above is that you have around a 70% chance of having a whipsaw event when you are in a “hedged” position. For the US market the stats are even more sobering — almost 90% of the time you can expect to experience a whipsaw event while in a “hedged” status. In short, if you are a trend-follower, expect whipsaws most of the time.

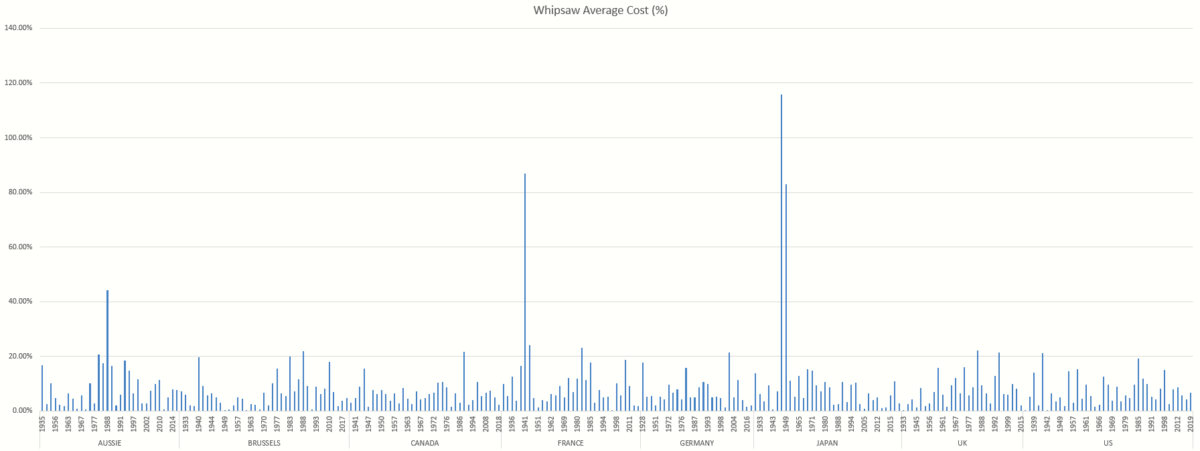

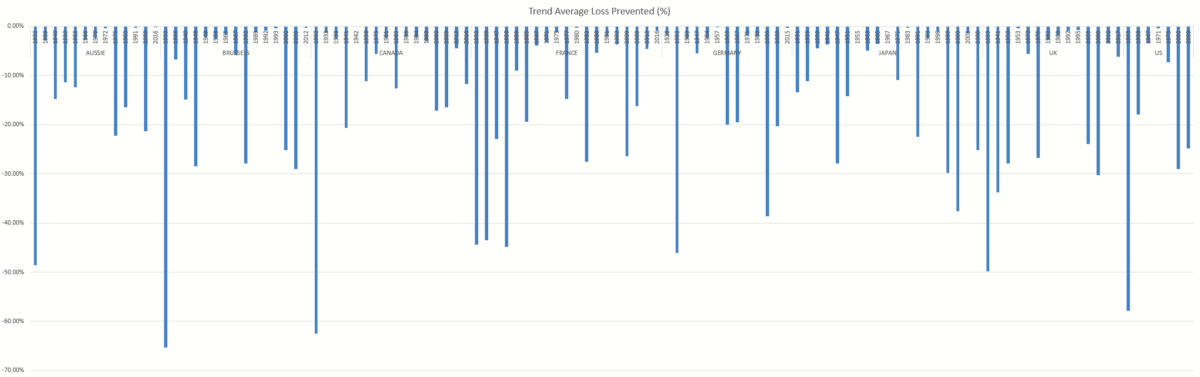

What is the average whipsaw “cost”?

Here we plot out the average whipsaw “cost” by country/year. This cost reflects an opportunity costs and is measured as the spread between your exit price and your entry price. For example, if you exit at $100, put your money in cash, and then re-buy at $110, this would represent a 10% “whipsaw cost.”(6)

The average whipsaw cost is pretty small, save a few huge outliers in markets with violent moves during WW2.

What is the average whipsaw benefit?

The analysis above highlights the frequency of whipsaw costs and maps out the costs of these whipsaws over time. Of course, not all is lost with trend-following. There is an upside if you can believe it! When trend works, it really works and saves one portfolio from potential major losses.

Here we have the average savings when a trend-following rule isn’t a whipsaw (i.e., it “worked”). For example, if we exit at $100 and enter at $50, we would save a -50% drawdown.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

The average loss saved by time/country is substantially larger than the whipsaw costs. This helps explain why trend-followed equity strategies look relatively good compared to buy-and-hold trend-followed equity strategies over long periods of time (where good = similar CAGR with better drawdown profiles). The reason we see this result is due to the fact that the benefits of trend-following (e.g., avoiding infrequent mega losses) make up for the cost of trend-following (e.g., frequently losing out on whipsaws).

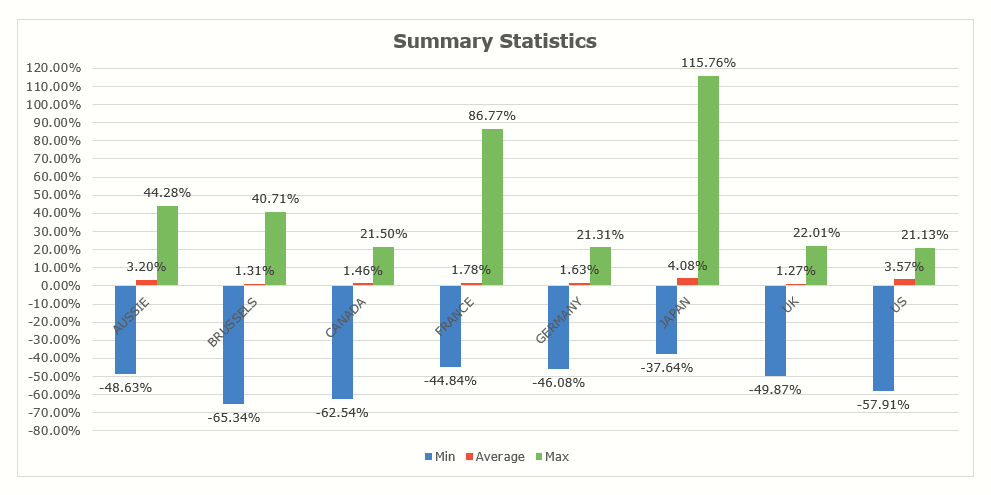

Trend Following Exit/Entry summary statistics

The observations below map out the minimum, maximum, and average exit/entry for each country.

The average exit/entry is positive, i.e., a “whipsaw” event, but the average is fairly small and as we pointed out above, fairly frequent. We also see that the maximum whipsaw costs (a positive observation) are generally lower than the maximum whipsaw benefit (a negative observation). But there are certainly opportunities to get absolutely destroyed in a whipsaw — see France/Japan as good examples.

Conclusion

Investing in stocks can be hazardous to one’s wealth. The long-term profile of stock market volatility is more violent than many probably realize, but the threat of intense volatility is real. To assume otherwise would be dangerous. So what is an investor to do? The easy answer is “diversification”. Clearly, one wants to allocate broadly across a lot of stock markets (and a lot of assets!). Another potential tool is trend-following, which has historically been a reasonably effective (albeit imperfect and sometimes destructive) way to manage extreme tail risks. The huge challenge of trend-following (and even diversification to a certain extent) is managing one’s behavior. One must endure numerous periods of “pain” in order to potentially benefit from the gain of trend-following.

What’s the bottom line? I’ll leave it Jack, who has a post entitled, “Trust the Process.” The key takeaway is that having conviction for an evidence-based process is critical for long-term success.

References[+]

| ↑1 | We could technically start in 1915 (limited by Japan and could go even further back if Japan is excluded), but our analysis system is built from 1927 forward. We are rebuilding our systems this summer and can report on “out of sample” as a follow-on post. | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| ↑2 |

Here are the formal index data used from GFD.

| ||||||||

| ↑3 | The one black eye for trend-following is WW2. Stock markets in Germany/France/Japan were essentially decimated in short order and trend-following was unable to save your bacon (score one for diversification!) | ||||||||

| ↑4 | See here for further analysis on the tracking error of trend following strategies. See here and here for a discussion on trend following benchmarks. | ||||||||

| ↑5 | same can be said for any active strategy, frankly). | ||||||||

| ↑6 | we assume 0% interest rate on proceeds for simplicity |

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.