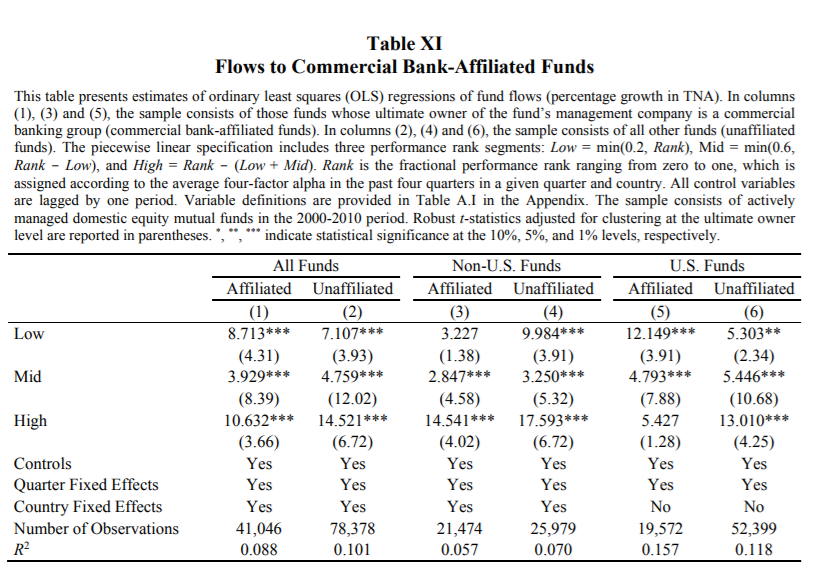

Do Bank Affiliated Funds Underperform Unaffiliated Funds?

By Wesley Gray, PhD|October 29th, 2018|Basilico and Johnsen, Academic Research Insight, Corporate Governance|

Asset Management within Commercial Banking Groups: International Evidence Miguel Ferreira, [...]

Alpha Architect Weekly Recap: Tracking Error and the “Mix Versus Integrate” Debate

By Wesley Gray, PhD|October 26th, 2018|Research Insights, Media, Weekly Research Recap Videos|

You can watch the video via the link below: This [...]

How large is the tracking error created by trend following?

By Jack Vogel, PhD|October 25th, 2018|Research Insights, Trend Following|

A question I've received in the past is the following: [...]

Constructing Long-Only Multifactor Strategies: Portfolio Blending vs. Signal Blending

By Tommi Johnsen, PhD|October 22nd, 2018|Factor Investing, Research Insights, Basilico and Johnsen, Academic Research Insight|

Constructing Long-Only Multifactor Strategies: Portfolio Blending vs. Signal Blending Khalid [...]

Alpha Architect Weekly Recap: ETF Tax Efficiency, Profitability Factor, Trend Following

By Jack Vogel, PhD|October 19th, 2018|Research Insights, Media, Weekly Research Recap Videos|

You can watch the video via the link below: This [...]

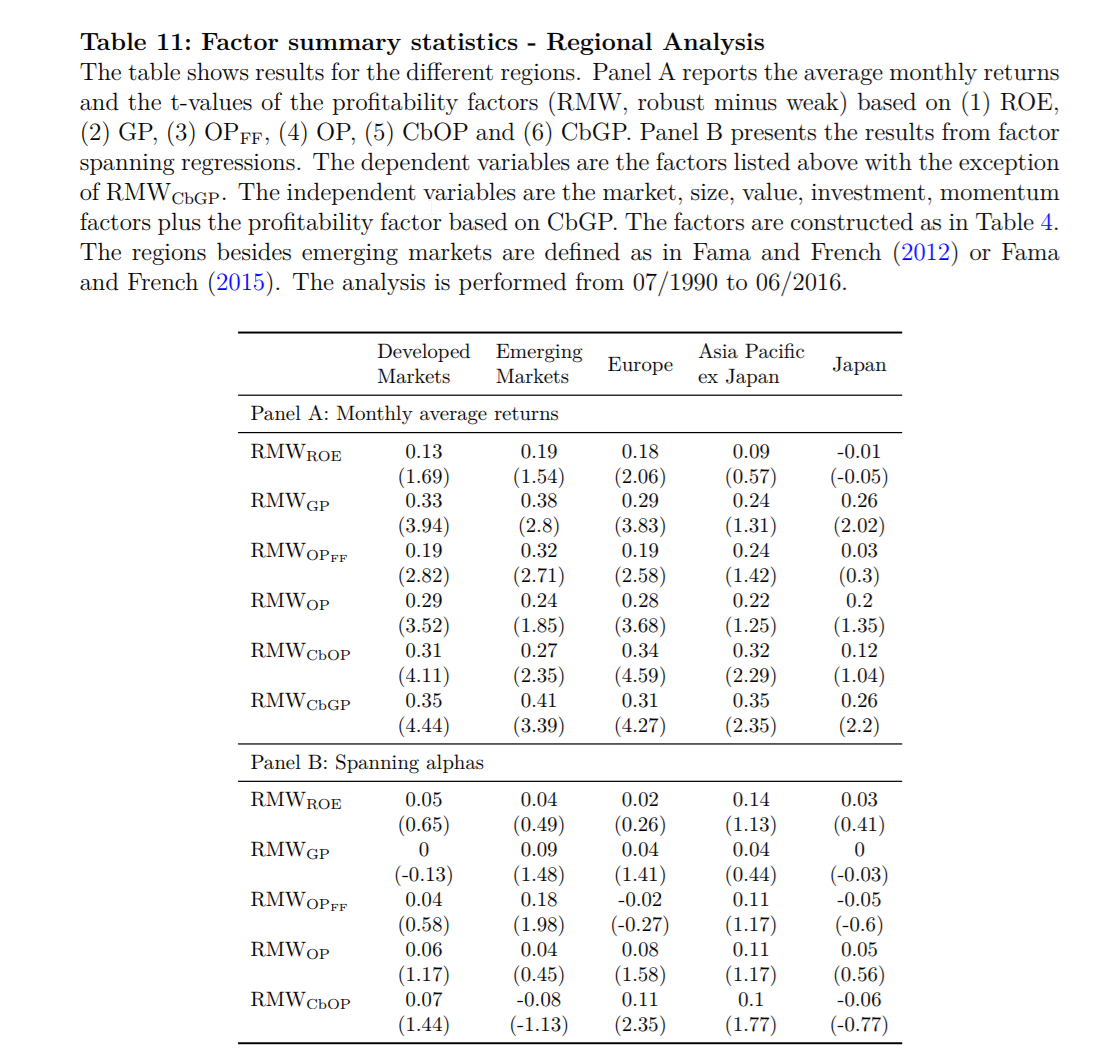

The Profitability Factor: International Evidence

By Larry Swedroe|October 18th, 2018|Quality Investing, Research Insights, Factor Investing|

Robert Novy-Marx’s 2013 paper “The Other Side of Value: The [...]

What is the correct benchmark for trend following?

By Jack Vogel, PhD|October 16th, 2018|Research Insights, Trend Following|

"What is the correct benchmark for trend following?" This is [...]

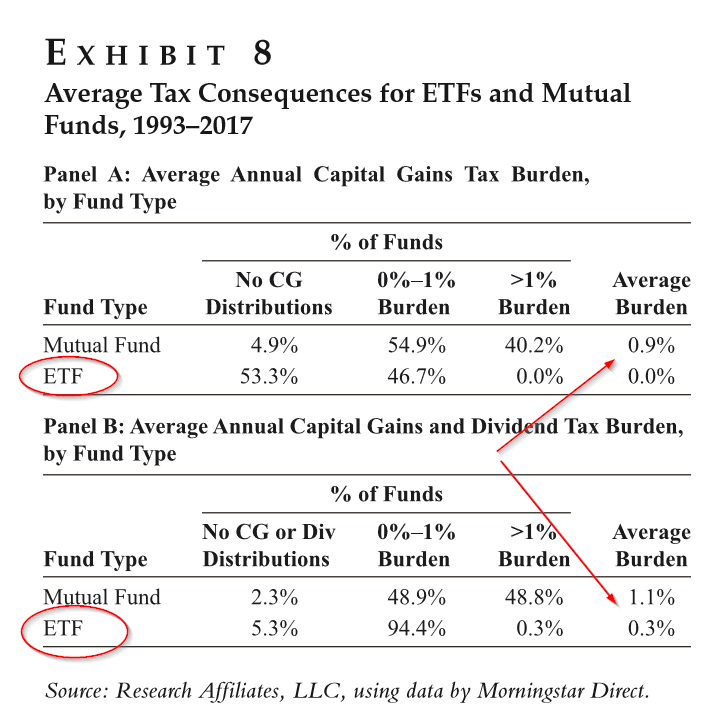

Can Your Alpha Cover the Tax Bill? Pro-Tip: The ETF Wrapper May Help.

By Tommi Johnsen, PhD|October 15th, 2018|Research Insights, Basilico and Johnsen, Academic Research Insight|

This blog discusses the academic research about after-tax alpha by [...]

Video: Alpha Architect Weekly Research Recap

By Jack Vogel, PhD|October 12th, 2018|Podcasts and Video, Media, Weekly Research Recap Videos|

You can watch the video via the link below: Video [...]

How a Multi-factor Portfolio is Constructed Matters

By Larry Swedroe|October 11th, 2018|Larry Swedroe, Factor Investing, Research Insights|

The CAPM was the first formal asset-pricing model. Market beta [...]