Litigation Finance as Alternative Investment

By Larry Swedroe|August 11th, 2022|Event Driven Investing, Research Insights, Larry Swedroe, Academic Research Insight|

Litigation finance is a rapidly growing niche asset class focused on debt and equity investments in litigation claims and law firms. We find that in-sample returns in the space have been in excess of 20% annually with limited correlation to other investment areas. This apparent excess return may be due to information asymmetry and barriers to entry in the space. Our findings highlight the opportunities and risks for investors in this nascent asset classes and suggest such excess returns are due in part to limits to the speed with which efficient markets take hold.

Treasury Bonds: Buy and Hold or Trend Follow?

By Wesley Gray, PhD|August 10th, 2022|Research Insights, Trend Following, Introduction Course, Tactical Asset Allocation Research|

If one had to invest in buy and hold treasury bonds or trend-followed treasury bonds, it is likely that most investors would prefer the trend-followed bond investment. However, in a broader portfolio context, the analysis suggests that how one 'eats' their bond exposure is largely irrelevant and the portfolio's long-term outcome will be driven by equity market dynamics. Bonds systematically lower an equity-centric portfolio's returns, but they also lower the risk profile of the overall portfolio.

Global Factor Performance: August 2022

By Wesley Gray, PhD|August 9th, 2022|Index Updates, Research Insights, Factor Investing, Tool Updates, Tactical Asset Allocation Research|

Standardized Performance Factor Performance Factor Exposures Factor Premiums Factor Attribution Factor Data Downloads

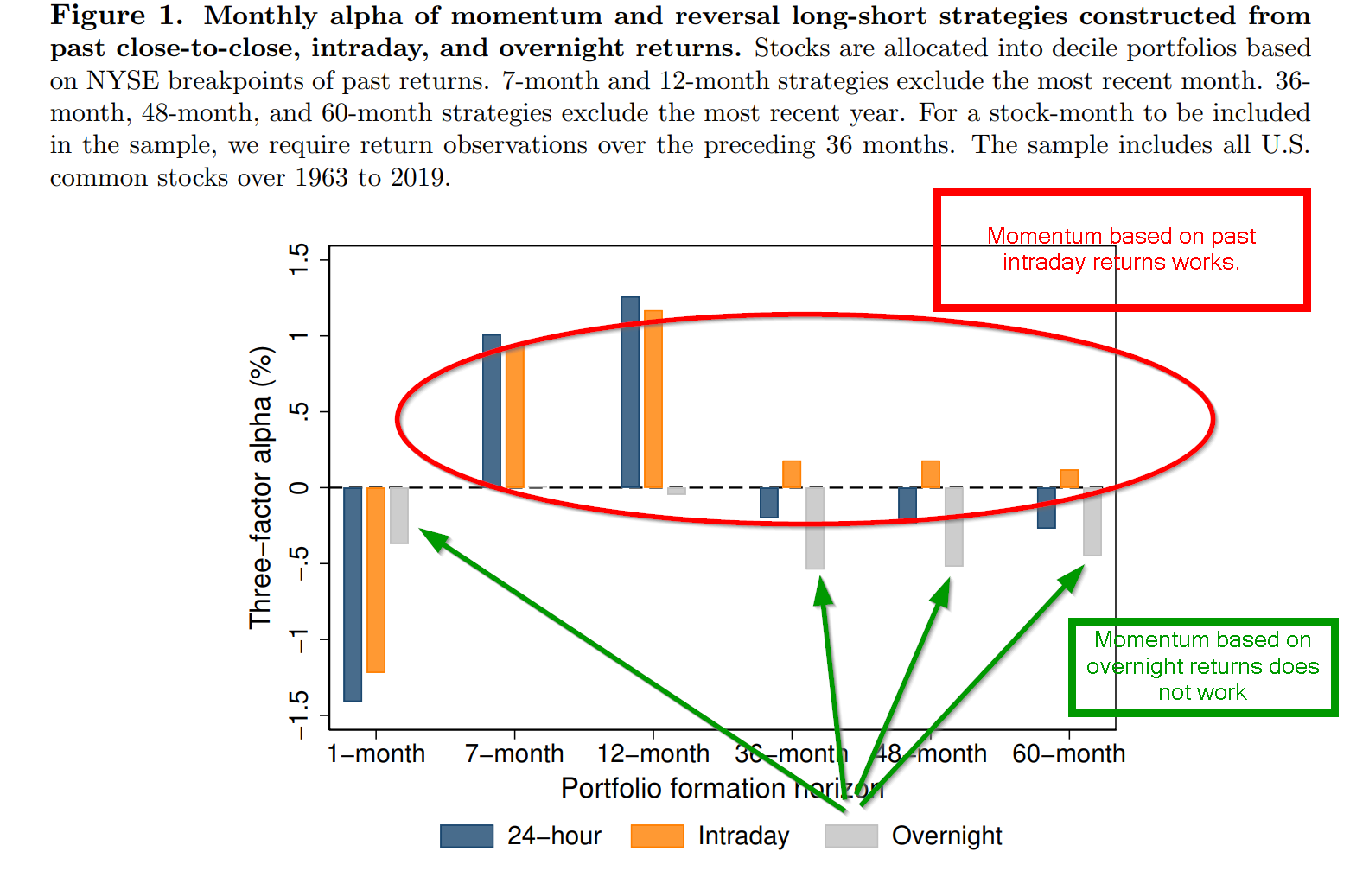

What Drives Momentum and Reversal?

By Tommi Johnsen, PhD|August 8th, 2022|Price Pressure Factor, Overnight Returns Research, Factor Investing, Research Insights, Basilico and Johnsen, Academic Research Insight, Momentum Investing Research|

How information affects asset prices is of fundamental importance. Public information flows through news, while private information flows through trading. We study how stock prices respond to these two information flows in the context of two major asset pricing anomalies— short-term reversal and momentum. Firms release news primarily during non-trading hours, which is reflected in overnight returns. While investors trade primarily intraday, which is reflected in intraday returns. Using a novel dataset that spans almost a century, we find that portfolios formed on past intraday returns display strong reversal and momentum. In contrast, portfolios formed on past overnight returns display no reversal or momentum. These results are consistent with underreaction theories of momentum, where investors underreact to the information conveyed by the trades of other investors.

Avoiding Momentum Crashes

By Larry Swedroe|August 4th, 2022|Larry Swedroe, Research Insights, Factor Investing, Academic Research Insight, Momentum Investing Research|

Across markets, momentum is one of the most prominent anomalies and leads to high risk-adjusted returns. On the downside, momentum exhibits huge tail risk as there are short but persistent periods of highly negative returns. Crashes occur in rebounding bear markets, when momentum displays negative betas and momentum volatility is high. Based on ex-ante calculations of these risk measures we construct a crash indicator that effectively isolates momentum crashes from momentum bull markets. An implementable trading strategy that combines both systematic and momentum-specific risk more than doubles the Sharpe ratio of original momentum and outperforms existing risk management strategies over the 1928–2020 period, in 5 and 10-year sub-samples, and an international momentum portfolio.

Trend Following Says Commodities…But Nothing Else!

By Wesley Gray, PhD|August 3rd, 2022|Research Insights, Trend Following, Introduction Course, Tactical Asset Allocation Research|

The analysis above highlights that we are in a rare regime when commodities are the only long asset with a positive trend. The last time this happened we entered a long period of high inflation and poor real returns. Will this happen again? Who knows. But we do know that post-1973 we entered a world where, for several decades (at least up to around 2007), both bonds and commodities were an important component of a diversified portfolio. The recent past has arguably made investors complacent in their reliance on a stock/bond portfolio as an end-all-be-all solution. When history tells us that incorporating commodities into a portfolio probably makes sense from a diversification standpoint.

DIY Asset Allocation Weights: August 2022

By Ryan Kirlin|August 1st, 2022|Index Updates, Research Insights, Tool Updates, Tactical Asset Allocation Research|

No exposure to domestic equities. No exposure to international equities. No exposure to REITs. Full exposure to commodities. No exposure to intermediate-term bonds.

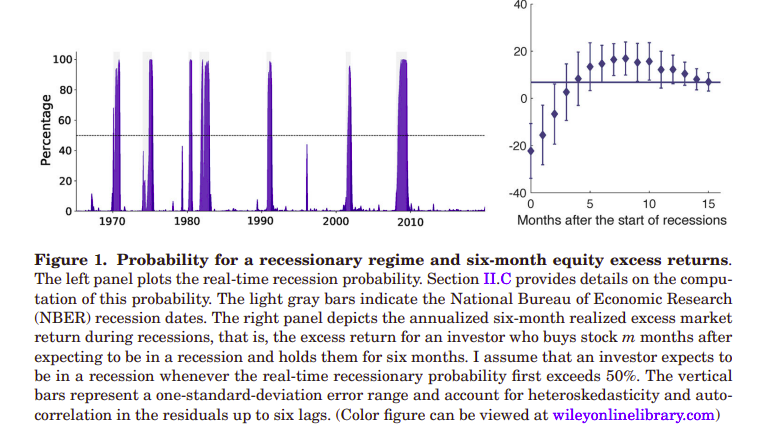

Do Stocks Efficiently Predict Recessions?

By Elisabetta Basilico, PhD, CFA|August 1st, 2022|Research Insights, Factor Investing, Basilico and Johnsen, Academic Research Insight, Tactical Asset Allocation Research, Macroeconomics Research|

I find that returns are predictably negative for several months after the onset of recessions, becoming high only thereafter. I identify business cycle turning points by estimating a state-space model using macroeconomic data. Conditioning on the business cycle further reveals that returns exhibit momentum in recessions, whereas in expansions they display the mild reversals expected from discount rate changes. A strategy exploiting this pattern produces positive alphas. Using analyst forecast data, I show that my findings are consistent with investors' slow reaction to recessions. When expected returns are negative, analysts are too optimistic and their downward expectation revisions are exceptionally high.

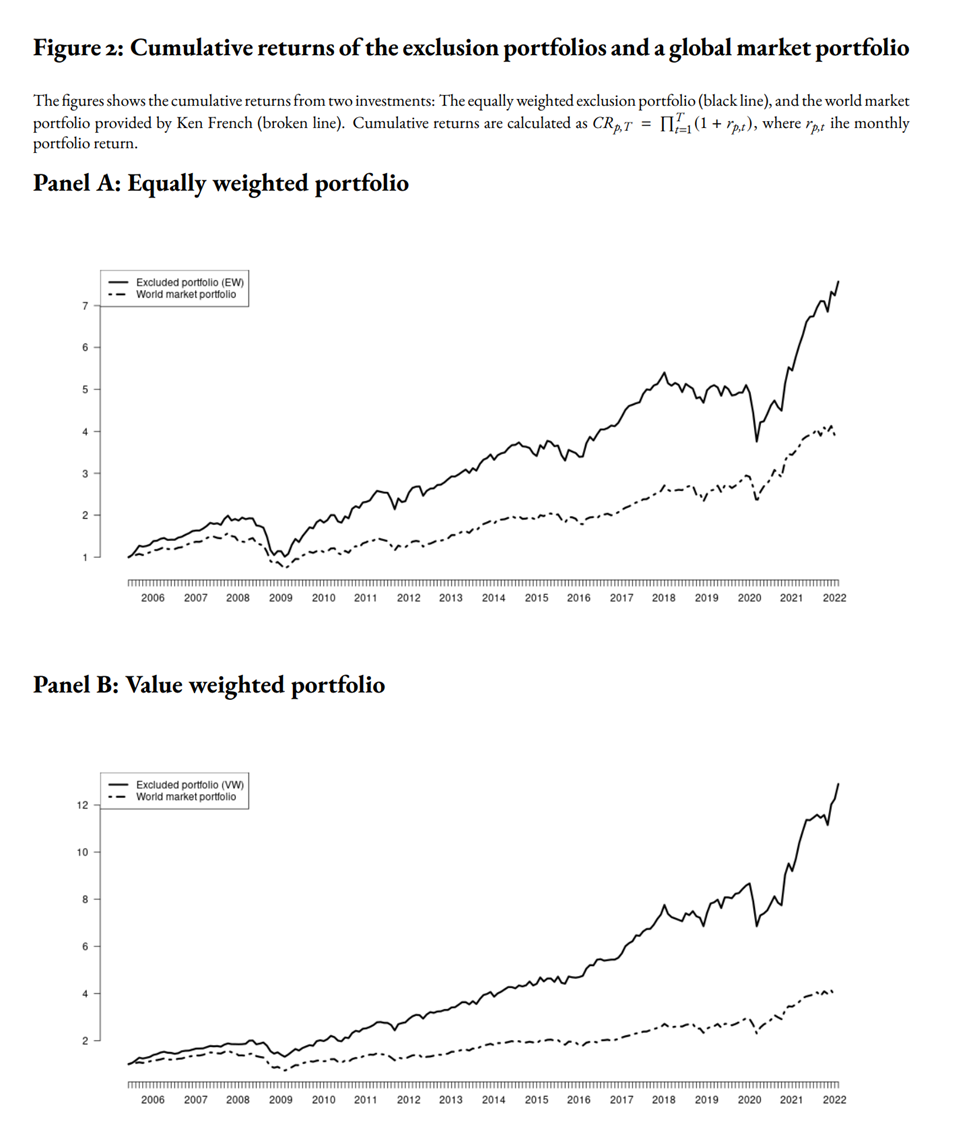

The Expected Returns to ESG-Excluded Stocks

By Larry Swedroe|July 28th, 2022|ESG, Larry Swedroe, Factor Investing, Research Insights, Academic Research Insight|

What are the consequences of widespread ESG-based portfolio exclusions on the expected returns of firms subject to exclusion? We consider two possible theoretical explanations. 1) Short-term price pressure around the exclusions leading to correction of mispricing going forward. 2) Long term changes in required returns. We use the exclusions of Norwegian Government Pension Fund Global (GPFG -`The Oil Fund') to investigate. GPFG is the world's largest SWF, and its ESG decisions are used as a model for many institutional investors. We construct various portfolios representing the GPFG exclusions. We find that these portfolios have significant superior performance (alpha) relative to a Fama-French five factor model. The sheer magnitude of these excess returns (5\% in annual terms) leads us to conclude that short-term price pressure can not be the only explanation for our results, the excluded firms expected returns must be higher in the longer term.

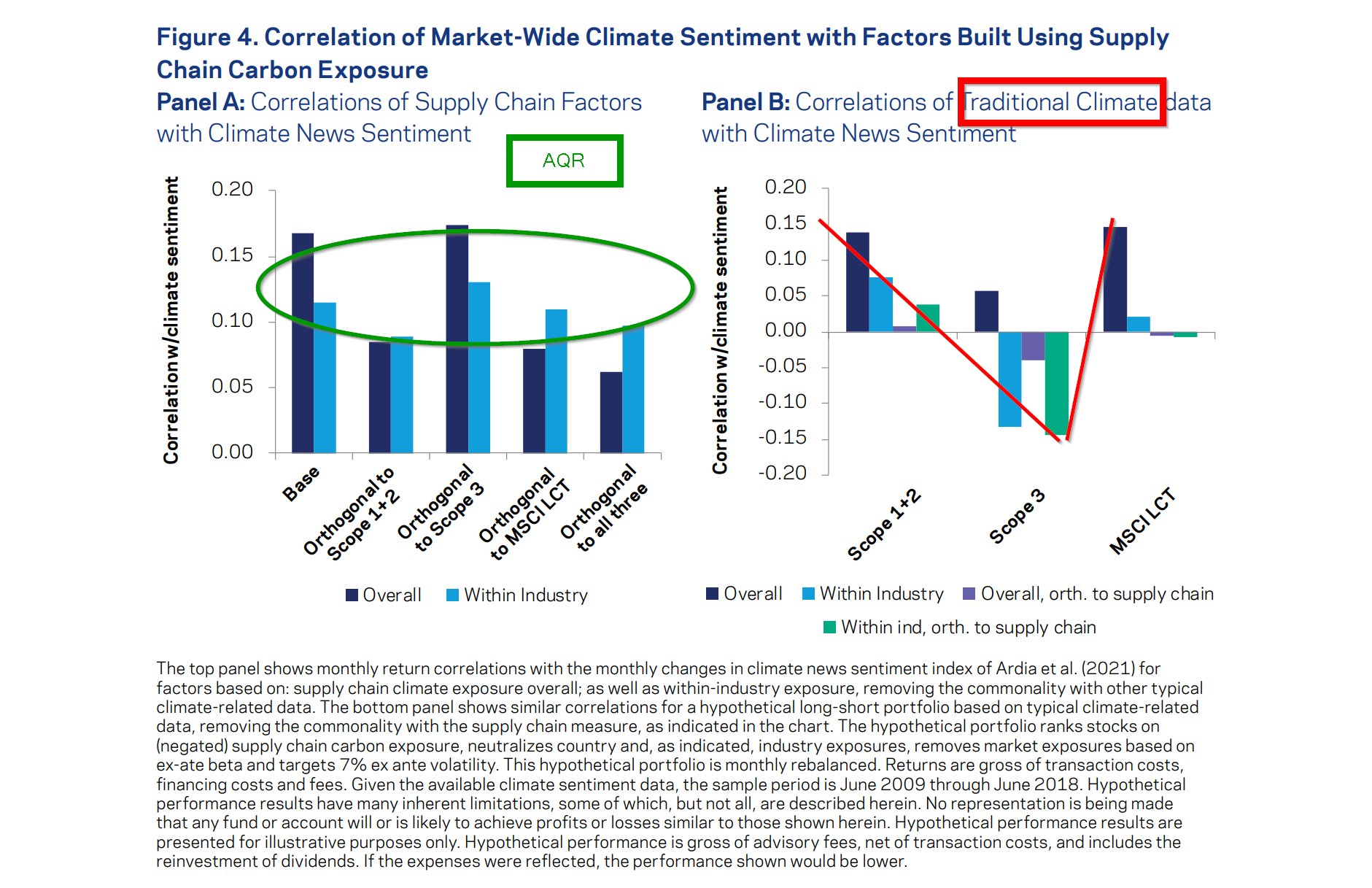

Measuring a Firms’ Environmental Impact

By Tommi Johnsen, PhD|July 25th, 2022|ESG, Research Insights, Basilico and Johnsen, Academic Research Insight|

To manage climate risks, investors need reliable climate exposure metrics. This need is particularly acute for climate risks along the supply chain, where such risks are recognized as important, but difficult to measure. We propose an intuitive metric that quantifies the exposure a company has to customers, or suppliers, who may in turn be exposed to climate risks. We show that such risks are not captured by traditional climate data. For example, a company may seem green on a standalone basis, but may still have meaningful, and potentially material, climate risk exposure if it has customers, or suppliers, whose activities could be impaired by transition or physical climate risks. Our metric is related to scope 3 emissions and may help capture economic activities such as emissions offshoring. However, while scope 3 focuses on products sold to customers and supplies sourced from suppliers, our metric captures the strength of economic linkages and the overall climate exposure of a firm’s customers and suppliers. Importantly, the data necessary to compute our measure is broadly accessible and is arguably of a higher quality than the currently available scope 3 data. As such, our metric’s intuitive definition and transparency may be particularly appealing for investors.