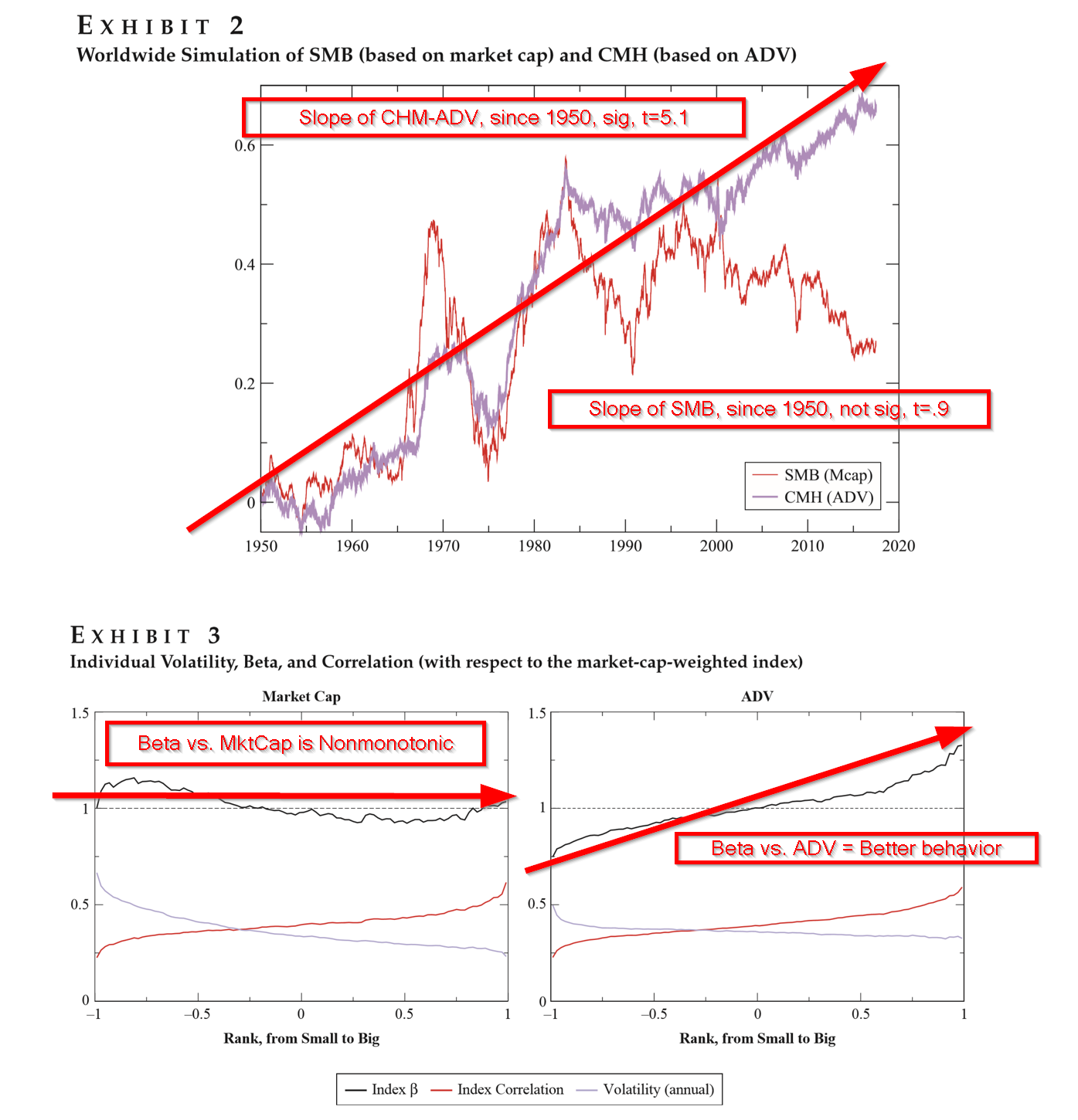

Liquidity might be a better proxy for Size in equity markets

By Tommi Johnsen, PhD|October 28th, 2019|Research Insights, Factor Investing, Basilico and Johnsen, Academic Research Insight, Size Investing Research|

The Size Premium in Equity Markets: Where Is the Risk? [...]

Core Earnings: New Data and Evidence

By Jack Vogel, PhD|October 24th, 2019|Research Insights, AI and Machine Learning|

Researchers love novel datasets--it gives them a new set of [...]

Superstar Investors

By Wesley Gray, PhD|October 23rd, 2019|Research Insights, Basilico and Johnsen, Academic Research Insight, Value Investing Research|

Superstar Investors Brooks, Tsuji and VillalonJournal of Investing, February 2019A version [...]

The Quality Factor—What Exactly Is It?

By Larry Swedroe|October 22nd, 2019|Quality Investing, Factor Investing, Research Insights, Low Volatility Investing|

While the quality factor has been identified in the literature [...]

Active Share: Predictor of Future Performance or Urban Legend?

By Larry Swedroe|October 17th, 2019|Financial Planning, Factor Investing, Research Insights, Academic Research Insight, Active and Passive Investing|

The crowning achievement for investors is the ability to identify [...]

Boutique ETF Issuers Finally Get a Break!

By Ryan Kirlin|October 15th, 2019|Tax Efficient Investing, ETF Investing|

Lingchi is the Chinese term for the form of torture [...]

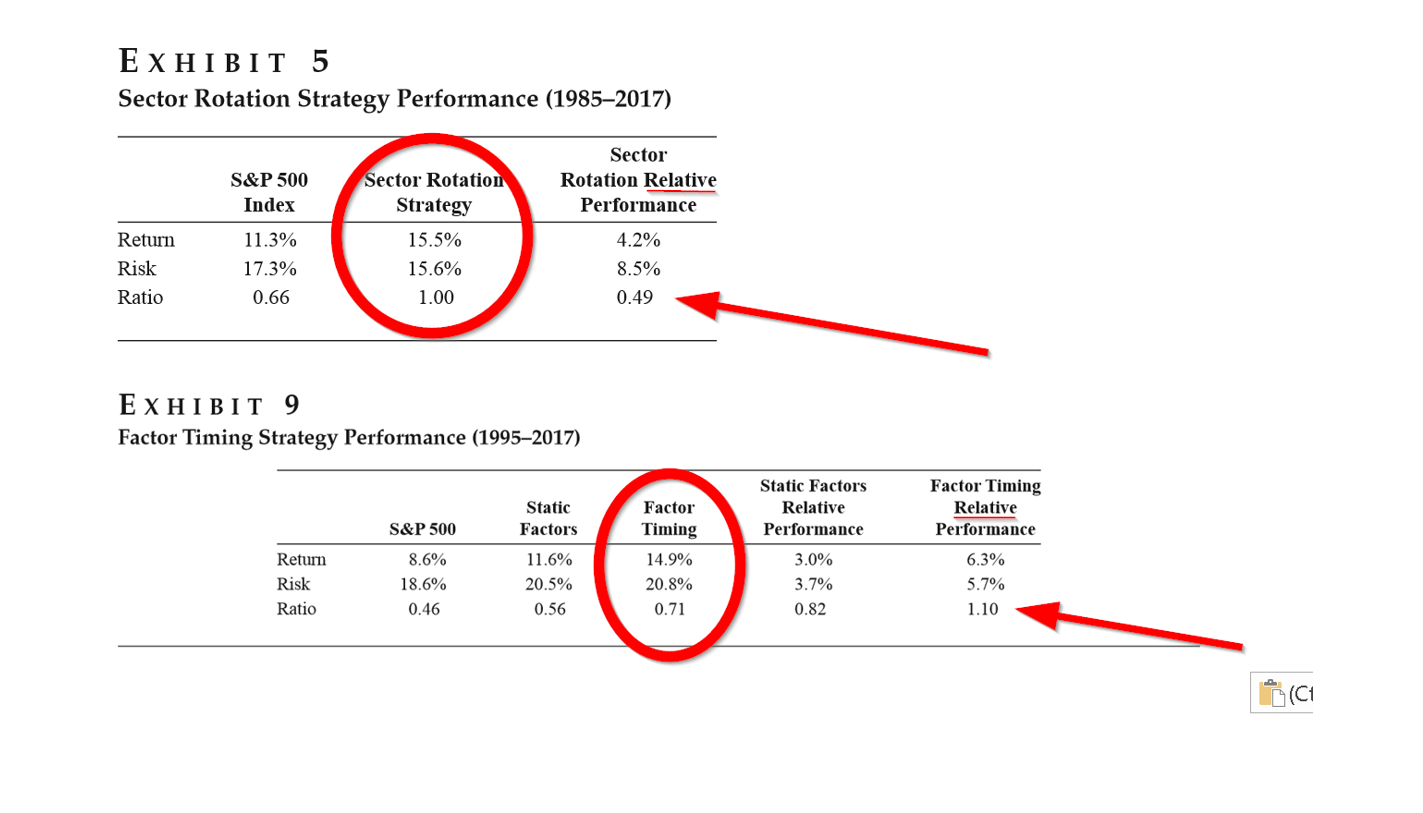

Crowded trades, asset centrality and predicting equity bubbles

By Tommi Johnsen, PhD|October 14th, 2019|Research Insights, Factor Investing, Basilico and Johnsen, Academic Research Insight|

Crowded Trades: Implications for Sector Rotation and Factor Timing William [...]

Using Firm Characteristics to Enhance Momentum Strategies

By Larry Swedroe|October 10th, 2019|Research Insights, Factor Investing, Momentum Investing Research|

Research into the momentum factor continues to demonstrate its persistence [...]

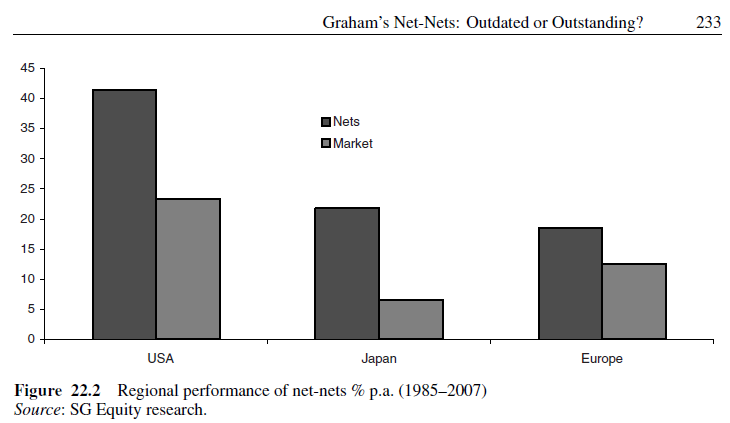

An Analysis of “Graham’s Net-Nets: Outdated or Outstanding?”

By Gaurang Merani, CPA|October 8th, 2019|Factor Investing, Research Insights, Value Investing Research|

James MontierA full version of this paper can be found [...]

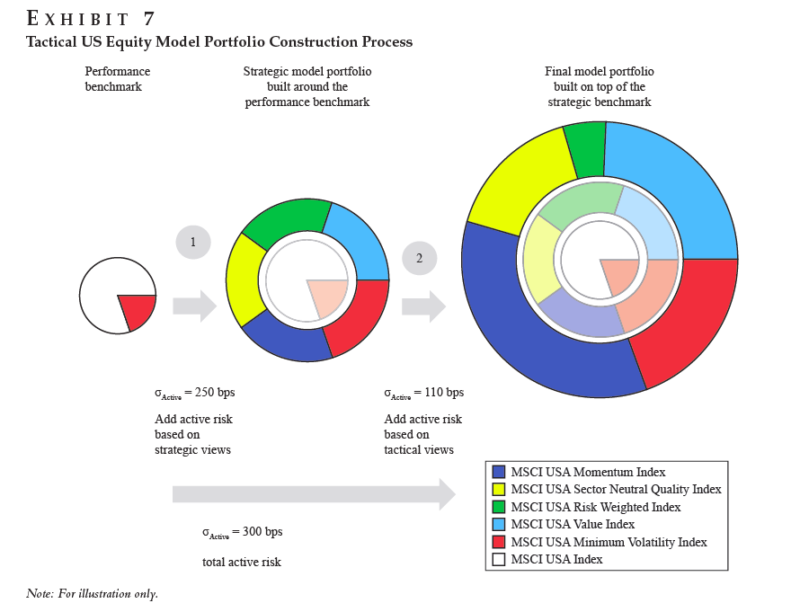

A Framework for Creating Model Portfolios

By Wesley Gray, PhD|October 7th, 2019|Factor Investing, Research Insights, Basilico and Johnsen, Academic Research Insight, Tactical Asset Allocation Research|

Model Portfolios Basu, Gates, Karir and AngJournal of Wealth Management, [...]