As many investors know, Eugene Fama developed the efficient-market hypothesis (EMH) at the University of Chicago in the 60s, and it subsequently flourished across academia. Under the strong-form interpretation of the EMH, asset prices reflect all available information (public and private) and there is no way for investors to consistently outperform a randomly selected basket of securities after controlling for risk. As noted EMH proponent Burton Malkiel so eloquently put it in his 1973 classic, A Random walk Down Wall Street: “A blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by experts.”

Indeed, the cult of efficient markets was pervasive in many of the nation’s business schools, and heretics have been frequently banished from the EMH temple. While some finance professors openly scoffed at the notion of being able to add value through fundamental analysis, they reserved the innermost concentric circle of hell for technical analysts, who were perceived as financial quacks and charlatans. Why? Because Wall Street is a random walk, and past price movements tell you nothing about the future.

Yet all was not well in paradise, as it emerged there was more to the story on technical analysis. Anomalies that were inconsistent with EMH began to emerge in the literature in the 70s, for example, a basket of low P/E stocks tends to outperform the market. At around the same time that the EMH was basking in glory, Daniel Kahneman was also working with Amos Tversky and others on exploring cognitive and behavioral psychology, which were found to significantly affect individual financial decisionmaking. It began to seem that there could be a connection between investors’ internal behavioral biases, and many of the observed anomalies that were being identified in the academic finance literature.

In the early 90s academics (e.g., Jagadeesh and Titman (1993)) began to focus on the concept of “momentum,” which refers to the fact that, contrary to the EMH, past returns can predict future returns, via a trend effect. That is, if a stock has performed well in the recent past, it will continue to perform well in the future. EMH proponents were perplexed, but argued that momentum returns were likely related to additional risks borne: riskier smaller and cheaper companies drove the effect. Many researchers have responded with studies that find the effect persists even when controlling for company size and value factors. And the effect appears to hold across multiple asset classes, such as commodities, currencies and even bonds. (e.g., Check out Chris Geczy’s “World’s Longest Backtest”)

In short, it appears the evidence for momentum is only growing stronger (Gary Antonacci has some great research on the subject: http://optimalmomentum.blogspot.com/). Today researchers are going even farther by applying behavioral finance concepts in order to understand psychological factors that drive the momentum effect.

In “Demystifying Managed Futures,” by Brian Hurst, Yao Hua Ooi, and Lasse Heje Pedersen, the authors argue that the returns for even the largest and most successful Managed Futures Funds and CTAs can be attributed to momentum strategies. They also discuss a model for the lifecycle of a trend, and then draw on behavioral psychology to hypothesize the cognitive mechanisms that drive the underlying momentum effect.

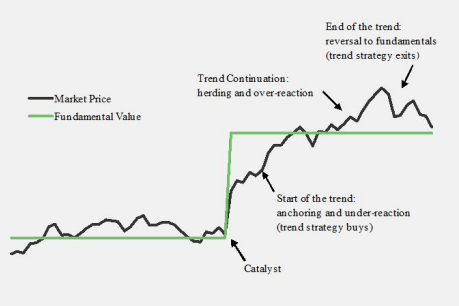

Below is a graph of a typical trend:

Note that there are several distinct components to the trend: 1) initial under-reaction, when market price is below fundamental value, 2) over-reaction, as the market price exceeds fundamental value, and 3) the end of the trend, when the price converges with fundamental value. There are several behavioral biases that may systematically contribute to these components.

Under-reaction phase:

Adjustment and Anchoring. This occurs when we consider a value for a quantity before estimating that quantity. Consider the following 2 questions posed by Kahneman: Was Gandhi more or less than 144 years old when he died? How old was Gandhi when he died? Your guess was affected by the suggestion of his advanced age, which led you to anchor on it and then insufficiently adjust from that starting point, similar to how people under-react to news about a security. (also, Gandhi died at 79)

The disposition effect. This is the tendency of investors to sell their winners too early and hold onto losers too long. Selling early creates selling pressure on a long in the under-reaction phase, and reduces selling pressure on a short in the under-reaction phase, thus delaying the price discovery process in both cases.

Over-reaction phase:

Feedback trading and the herd effect. Traders follow positive feedback strategies. For instance, George Soros has described his concept of “reflexivity,” which involves buying in anticipation of further buying by uninformed investors in a self-reinforcing process. Additionally, herding can be a defense mechanism occurring when an animal reduces its risk of being eaten by a predator by staying with the crowd. As Charles MacKay put it in 1841 in his book, Extraordinary Popular Delusions and Madness of Crowds, “Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one.”

Confirmation Bias and representativeness. In general, we suffer from a bias to confirm our beliefs and tend to search for information that supports those beliefs. Such a biased view might cause investors to move more money into investments, supporting a trend, when a dispassionate appraisal might suggest price already exceeds the fundamental value. Similarly, investors see recent price momentum and assume via representativeness that this reflects future conditions, likewise supporting the trend.

We found that the trend lifestyle framework and proposed underlying psychological factors made good intuitive sense and were consistent with both the momentum effect itself as well as many established behavioral finance concepts.

The growing academic body of work supporting the existence of the momentum effect, along with a sensible psychological framework that explains it, are a potent combination. Indeed, momentum may have come of age as an investment tool, as more and more investors incorporate it into their portfolios. If you would like to see the evidence for how momentum explains manager returns, we urge you read the paper, which can be found here:

http://pages.stern.nyu.edu/~lpederse/papers/DemystifyingManagedFutures.pdf

Given that ultimately there is not all that much mystery associated with many of the most successful Managed Futures strategies, it follows that we should pay attention to what we can get for free (or for very little). If something is widely available at both a high and a low cost, then why pay a lot for it?

If most strong CTA returns are due to basic momentum strategies, then it follows that there is nothing special about what many of the top funds are doing. For this reason, we should be extra vigilant with respect to fees. If a commodity fund manager charges high fees, try to understand exactly what you are getting for those extravagant fees. Is it momentum? Likely. Again, why pay 2/20 for something you can get for less?

About the Author: David Foulke

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.