I Believe…Why Don’t You?

To believe your own thought, to believe that what is true for you in your private heart, is true for all men–this is genius. — Emerson, Self-reliance (1841)

False consensus — to see their own behavioral choices and judgments as relatively common and appropriate to existing circumstances while viewing alternative responses as uncommon, deviant, or inappropriate. –Ross, Greene, and House (1977)

People tend to evaluate their thoughts and behaviors based on other people, which is widely known as social comparison (Festinger, 1954). It is true that most of us feel good about ourselves when being conformed by our peers and thus we are motivated to seek such conformations (Suls and Wills, 1991).

However, we are not always able to accurately judge the opinions of others. Thus, what we believe is heavily influenced by what we think others believe, and by how we interpret the social environment. What does that mean? Ross, Greene, and House (1977) firstly raised the concept of “False-consensus bias.” From a psychological point of view, people tend to overestimate the level to which other people share their beliefs, attitudes, and behaviors.

Game: We think you agree

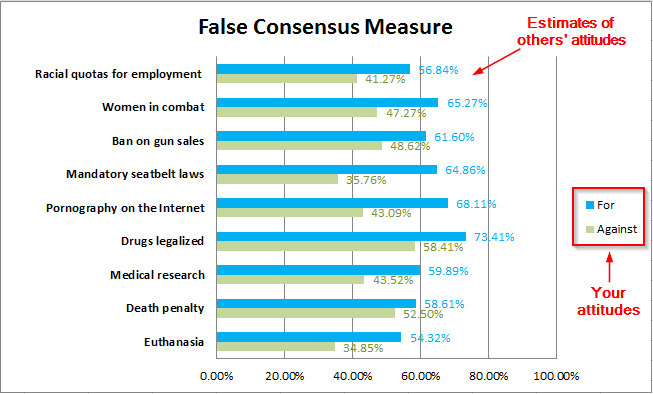

Before we go further, let’s first take a look about some statistics. Bauman and Geher (2003) conducted an experiments on 203 college students, asking about their own position on 20 different social issues (for or against) and an estimate of the percentage of peers who were in favor of each issue (on a scale from 0 to 100%).

Below chart describes parts of the results. People tend to think that others believe the same thing. For example, on the “Mandatory seat belt laws” issue, people who indicate that they support such laws assumes that 64.86% of others would feel the same. For people that don’t support seat belt laws, they believe that only 35.76% support such laws.

People make systematic errors interpreting social norms.

Data source: Bauman and Geher (2003), Table 1

One may argue that it’s not a big deal to have such bias, because false consensus increases self-esteem and confidence. However, such bias will lead people to overestimate the accuracy of their own judgments and believe that other alternative thoughts are uncommon, deviant, or biased.

Applications in Finance:

Choi and Williams (2013) finds that financial analysts suffer from false-consensus biases. He notices that “an analyst who overestimates the correlation of signal errors (within the firm’s earnings announcement) would underestimate the precision of collections of signals observed by groups of analysts. ” Simply put, analyst A and analyst B might underestimate the likelihood that they are focusing on different parts of the earnings announcement, and thus overestimate the correlation of their signal errors.

For naive investors, they regard themselves as rational in evaluating stock market, and believe others either to agree with them or to hold somewhat biased and defective evaluations. It’s a kind of overconfidence, which gives them a feeling of more assurance and security in their decisions, regardless of true or not.

References:

- Bauman and Geher, 2003, We think you agree: The detrimental impact of the false consensus effect on behavior, Current Psychology, Winter 2002, Volume 21, Issue 4, pp 293-318

- Choi and Williams ,2013, The False Consensus Effect and Trading Around Earnings Announcements, Wroking paper series

- Ross, Greene and House, 1977, The “False Consensus Effect”: An Egocentric Bias in Social Perception and Attribution Process, Journal of Experimental Social Psychology, 13, 219-301

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.