Traders, Guns, and Money

- Gopal and Greenwood

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category.

Abstract:

In this work, we investigate how mass shootings influence the stock price of firearms manufacturers. While significant anecdotal evidence suggests there is an immediate spike in firearms purchase after such events, the reaction of financial markets is unclear. On one hand, if the increased short-term demand represents an unanticipated financial windfall for firearms manufacturers, the stock prices of the firms may rise. On the other hand, mass shootings may result in perceptions of the social contract between the firm and society being systematically violated. In this case, the increasing potential for regulation may render the firm’s business model untenable in the long run, leading to stock prices decreasing….

Alpha Highlight:

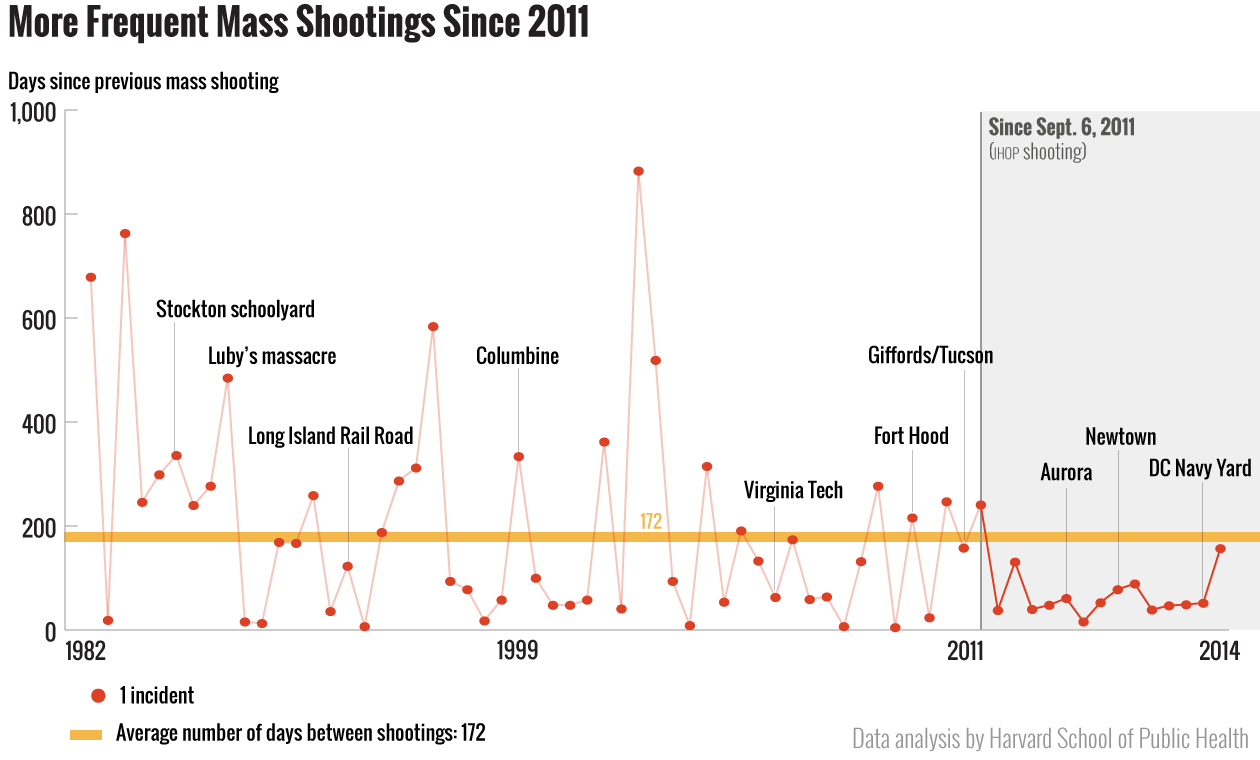

Obviously many devastating catastrophes are unpredictable. A typical example is a mass shooting. Harvard Researchers highlighted that since 2011, there was a mass shooting every 64 days on average.

People can still recall recent mass shooting events such as 2012 Elementary school shooting in Newtown (27 killed, 2 wounded), 2012 Movie theater shooting in Colorado (12 killed, 58 wounded) and 2007 Virginia Tech campus shooting in Virginia (32 killed, 25 wounded). According to Stanford University Libraries, about 40% of mass shootings over the past 40 years occurred at schools, where children and teenagers are targeted as victims.

After such events, the media inevitably stirs up the social debate on gun control, campus security, mental health treatment, etc. So how has the stock market responded to such random tragedies? This paper investigates this question.

The paper provides two hypotheses:

- On the one hand, anecdotal evidence suggests there is an immediate spike in firearms purchases after such events. For example, the local gun sales profits jumped by 52% in the year after the Elementary school shooting in Newtown.

- On the other hand, mass shootings may increase the perceived likelihood of future restrictions on gun sales, leading long-term financial effects on the firearm industry. Investors might reduce their valuations of these firearm manufacturers.

Empirical Analysis:

So which effect predominates? The paper addresses this question by testing the abnormal reactions in the stock market to such random and exogenous events.

- Data: The mass shooting data is drawn from Mayors Against Illegal Guns (2013) press release. The stock price data is from CRSP database.

- Sample: 93 mass shootings in US from January 2009 to September 2013.

- Variables: The dependent variable is the percent change in the stock price of the two publicly held firearm manufacturers: Smith & Wesson (SWHC) and Sturn, Ruger, & Co. (RGR); the independent variables are: the number of victims, location, whether or not children were involved and whether or not a handgun was involved.

- Method: study the abnormal returns of the two sample firearm manufacturers after a mass shooting, over 1, 2, 5, 10 and 30 days.

Punitive Effect on Stock Market:

- Main Results

There is clear punitive effect of mass shooting on firearm manufacturers.

Table 2 shows that there’s no significant effect in the 1st day post shooting, while a significant drop in the stock prices over a 2, 5, 10, and 30 day window. The daily drop is between 0.495 and 0.224 bps.

Then paper tests whether such punitive effect will influence the extended value chain (ex, the steel industry). The results show no contagion effects, so it seems the investors “penalize” the firearm manufacturers only.

- Robustness Tests Results

- As the number of victims increase, the punitive effect increases as well.

- In a striking result, the presence of children amongst the victims appear to have no significant effect;

- The results are not influenced by the location of the crime (whether the crime occurred in “red” or “blue” states)

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.