Manager Sentiment and Stock Returns

- Fuwei Jiang, Joshua Lee, Xiumin Martin, Guofu Zhou

- Journal of Financial Economics, forthcoming

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

- Does high corporate manager sentiment lead to speculative market overvaluation?

- Is the predictive power of such an indicator stronger compared to other macroeconomic predictors?

- Is the predictive power of such an indicator stronger compared to other investor sentiment measures?

What are the Academic Insights?

The authors construct a monthly manager sentiment index based on the aggregate textual tone* in 10Ks, 10Qs and corporate conference calls transcripts from 2003 to 2014.

They find the following:

- YES- The authors find both in sample and out of sample that increases in manager sentiment are associated with decreases in future month market excess returns. Corporate managers as a whole tend to be overly optimistic when the economy and the market peak. As such, the manager sentiment index can be seen as a contrarian indicator.

- YES- The authors compare their sentiment indicator with 14 other macroeconomic indicators. They find that the predictive power of the sentiment indicator is greater and remains largely unchanged after controlling for them.(1)

- YES- The authors compare their sentiment indicator with 5 other investor sentiment signals. They find that the manager sentiment is superior.

* To measure the tone they use the standard dictionary method (Loughran and McDOnald-2011 financial and accounting dictionaries). The tone is the difference between the number of positive and negative words in the disclosures scaled by the total word count of the disclosure.

Why does it matter?

The authors introduce a new measure of sentiment based on “corporate managers”. While investor sentiment has been widely used to examine a variety of financial issues, the manager sentiment index, which contains complementary information to the existing sentiment measures, may also yield a number of future applications in accounting and finance.

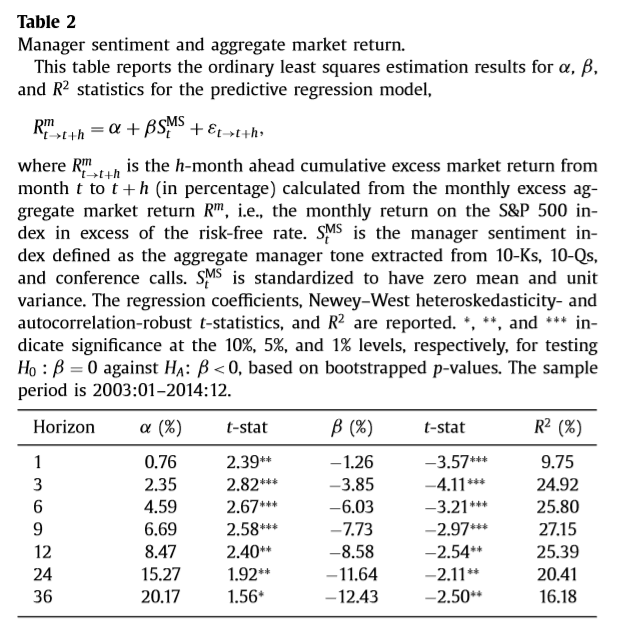

The Most Important Chart from the Paper:

Table 2 reports the in-sample OLS estimation results of the predictive regressions (2) for the manager sentiment index over each horizon. First, at the monthly horizon, the regression slope on the index, β, is−1.26, and is statistically significant at the 1% level based on the wild bootstrap pvalue, with a Newey-West t-statistic of −3.57. Therefore, the index is a significant negative market predictor: high manager sentiment is associated with low excess aggregate market return in the next month. This finding is consistent with our hypothesis that the sentiment index leads to market-wide over-valuation (under-valuation) when it is high (low), leading to subsequent low (high) stock returns in the future.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

This paper constructs a manager sentiment index based on the aggregated textual tone of corporate financial disclosures. We find that manager sentiment is a strong negative predictor of future aggregate stock market returns, with monthly in-sample and out-of-sample R2 of 9.75% and 8.38%, respectively, which is far greater than the predictive power of other previously-studied macroeconomic variables. Its predictive power is economically comparable and is informationally complementary to existing measures of investor sentiment. Higher manager sentiment precedes lower aggregate earnings surprises and greater aggregate investment growth. Moreover, manager sentiment negatively predicts cross-sectional stock returns, particularly for firms that are difficult to value and costly to arbitrage.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.